The growth in assets allocated to stablecoins will have an impact on the Treasury market — particularly on shorter-dated securities. If the inflows into digital assets continue at the current breakneck pace, the amount of money that those vehicles have to invest will soon be material even in the context of the Treasury market, wrote Jan Nevruzi, US rates strategist and Gennadiy Goldberg, head of US Rates Strategy at TD Securities in a recent article.

This may influence Treasury’s debt management decisions, leading to a shorter weighted average maturity of issuance. US Treasury is already paying close attention to this and has been asking primary dealers to comment on the topic.

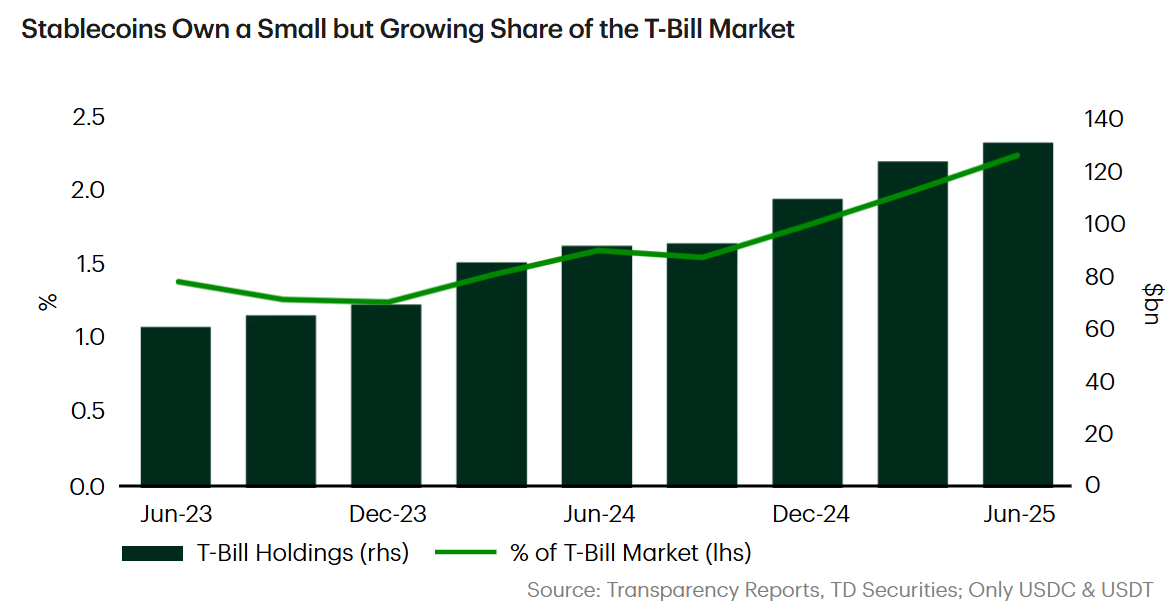

Dollar-denominated stablecoins, which at this stage make up nearly the entire fiat-backed stablecoin universe, are forced to back their tokens 1:1 with assets. The GENIUS Act imposed stricter guidelines on what those reserves can look like, but the main allocations will likely be to Treasury bills and coupons with less than 3 months of maturity and overnight repo (a close substitute to bills).

If stablecoins keep growing, they will be material investors in Treasury bill and repo markets. On the issuance side, the US Treasury is likely to take more comfort that there is a new source of demand for bills and increase its reliance on bills at the margin. On the repo side, market participants are likely to adjust their behavior to rely on this source of cash when intermediating financing needs.

This behavior resembles inflows into regular 2a-7 money market funds. However, in addition to regulatory differences, the flows in and out of stablecoins are inherently much more volatile than into money market funds. For example, the total market capitalization of stablecoins contracted by about 30% after reaching a local peak in 2021 after underperformance in crypto markets, de-pegging of algorithmic stablecoins, and the collapse of the digital currency exchange, FTX.

The market capitalization of stablecoins isn’t significant in the macro sense, a drawdown of a similar magnitude in future years could lead to large price shocks and funding issues as stablecoin issuers have to fire-sell inventories. Additionally, US Treasury is unlikely to rely on stablecoins when estimating the long-term demand for bills due to the risk of asset volatility. However, Nevruzi and Goldberg noted that the industry is much closer to maturity now and use cases have increased, allocators become more institutionalized, and regulations significantly increase transparency.

“Risks persist but are likely to continue diminishing in our view,” they wrote.