Collateral optimisation, balance sheet constraints and inventory management are all buzzwords we’ve heard repeated over the past few years, but are banks and asset managers actually practicing what they preach? In this article, we explore how J.P. Morgan Triparty is supporting financial institutions as they begin to measure and become increasingly accountable to Return on Investment metrics. Being open to a wide range of optimisation possibilities — from clients’ ordering lists, to running internal models, to adopting fully outsourced collateral activity — is no longer a nice to have, it is a necessity to be competitive.

The success measure of collateral optimisation has evolved in response to the changing regulatory framework over the last 20 years, starting with ranking cheapest to deliver securities. The most advanced market participants are now running what-if planning scenarios and keeping detailed security-level pricing across products and importantly allocating that collateral accordingly at a granular level. Firms have focused on optimisation in line with how big an impact it could have on the entity: banks benefit the most across revenues and balance sheet while a growing number of portfolio finance desks on the buy-side take a bespoke approach to self-funding. Whether giving or receiving collateral across OTC and listed derivatives, repo, securities lending, FX and structured products, and regardless of the leverage that a firm employs; collateral optimisation has become a critical component in achieving core business objectives.

The ability for service providers to meet clients at every stage in the optimisation process presents its own unique challenges. Some clients want customised optimisation models, others want insight into all their holdings, whilst many would rather layer their own optimisation models on top of their existing triparty optimisers. Across the industry, there is no one-size-fits all solution, and depending on the client need and investment, there are many options available to tailor solutions that best align with operational preferences and strategic objectives.

Defining optimisation across the industry today

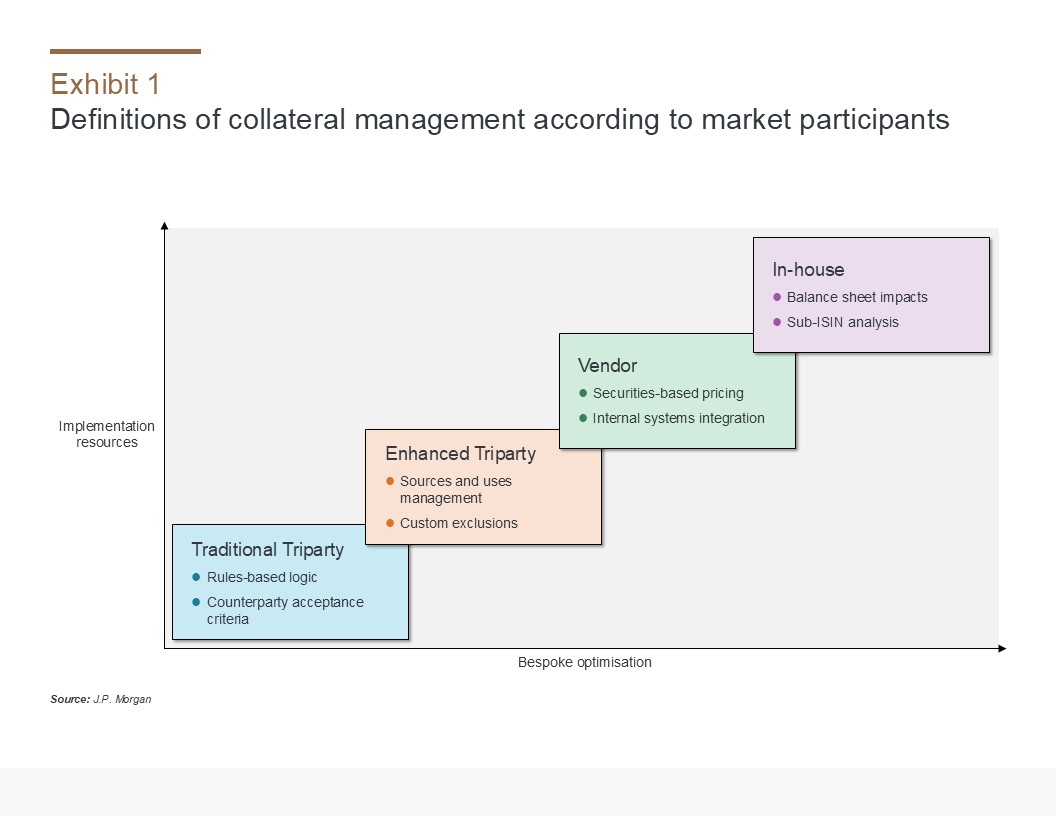

The end-goal of collateral optimisation as a mechanism to generate profitability is consistent across firms. There is less alignment however on how models operate including whether enhancing balance sheet capacity is a primary objective or not. In recent conversations with market participants on defining their optimisation models, we found as many different responses as the number of firms interviewed even when using the same technology vendor and triparty agents (see Exhibit 1). This shows the diversity of thinking about how to approach the problem and what questions are trying to be answered.

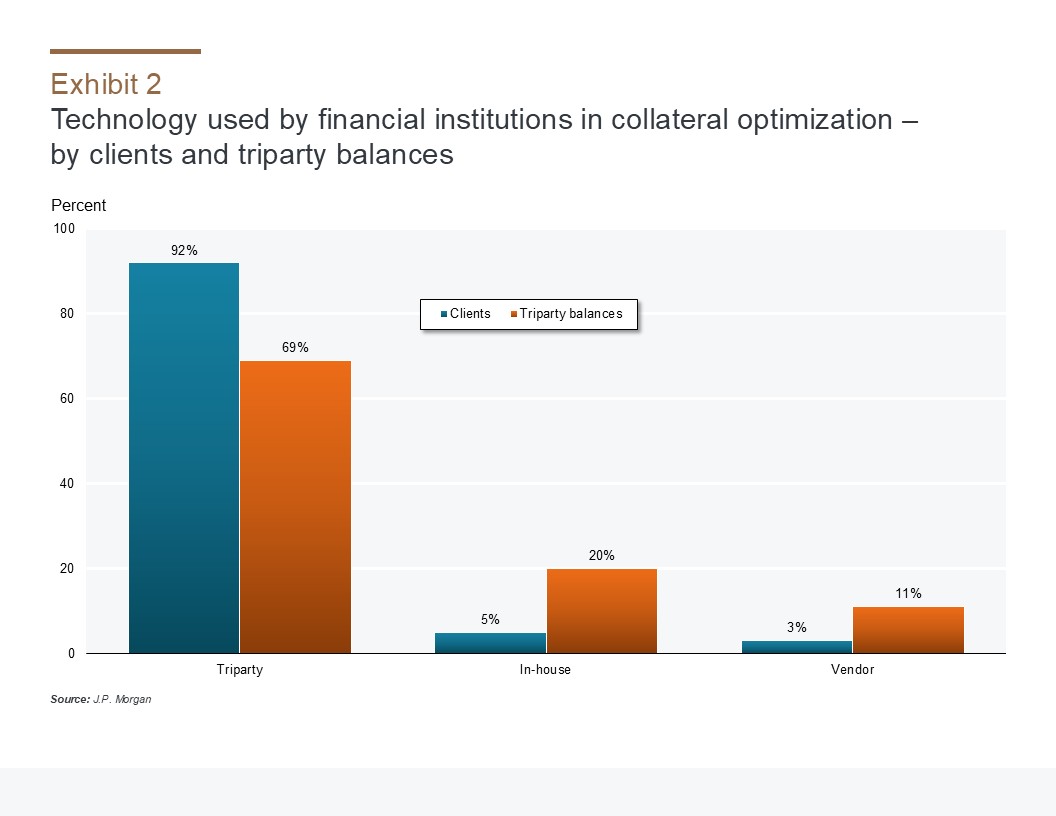

A large number of small to medium sized firms are at the earlier stages of optimisation while a smaller percentage of mostly larger, more sophisticated firms lead the market in adopting advanced technologies and practices. J.P. Morgan data shows that 92% of firms rely solely on their triparty agent’s collateral optimisation technology and represent 69% of triparty balances (see Exhibit 2). This is acceptable if there is a perceived moderate return to developing a more agile approach. Another 3% use a vendor optimisation package and are 11% of triparty balances, while the remaining 5% have built in-house optimisation technology and make up 20% of triparty balances. Some firms rely on their triparty agent only while others exchange data with a technology platform or their own models, then with their triparty agent, to find optimal results.

Firms’ adoption strategies suggests that the larger the book, the greater the benefit to optimisation and the justification of the investment spend. The more recent trend towards vendor solutions indicates that the cost to entry (both in terms of technology and time to market) is falling with more off-the-shelf but configurable functionality, which is already tried and tested, and fully integrated with triparty agents. The standardisation of data delivery methods required for optimisation algorithms further reduces barriers to using vendor solutions.

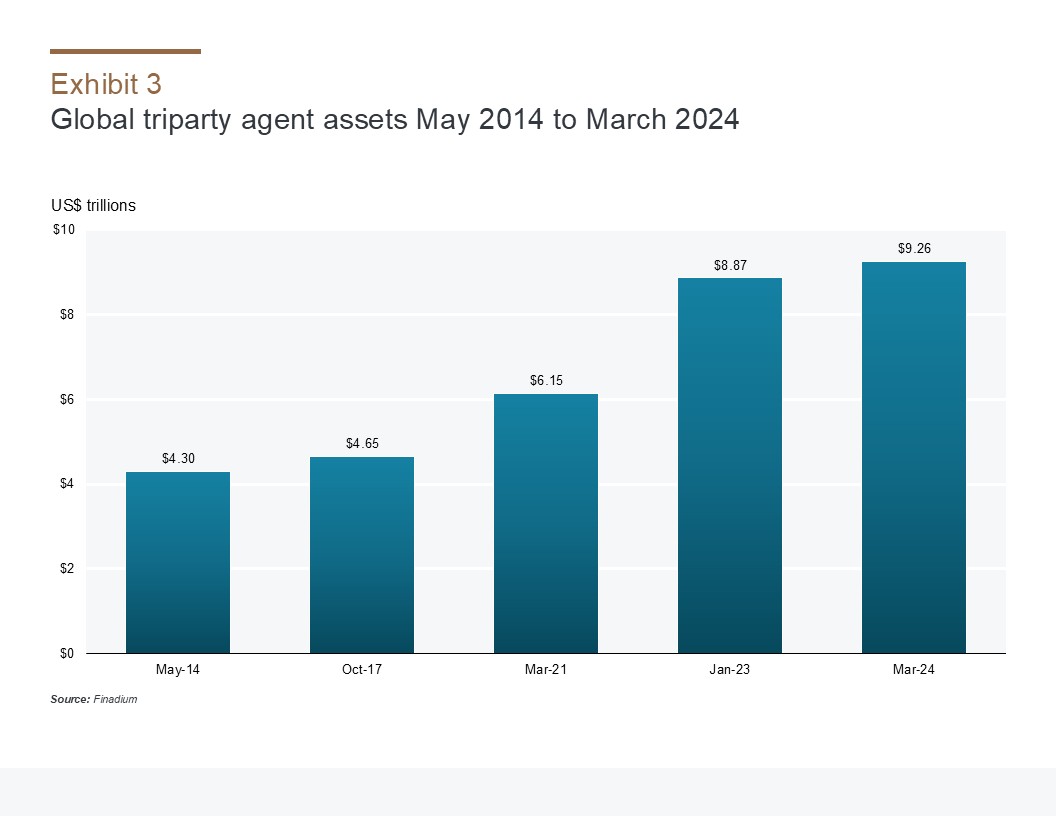

Triparty agents across the market are central to the conversation about collateral optimisation and every dealer of size uses at least one triparty agent. Triparty is now much more than repo: securities loans, centrally cleared products, OTC derivatives margin, central bank liquidity and structured products all form part of the product mix. The rapid growth in triparty balances in recent years shows the industry’s reliance on outsourcing at least some elements of the process: assets held by triparty agents have doubled from 2014-2024, according to regular surveys by Finadium (see Exhibit 3).

Sources and uses of collateral

Leading firms have invested in understanding the sources and uses of their inventory, or, where an asset comes from, what it is worth and how it can best be deployed (see Exhibit 4). A single view of global inventory increases the opportunities for collateral to be found that meets specific use cases on the other side; conversely, not including pools of assets means a natural loss of revenue and expanded capacity. Aggregating all available inventory pools across entities and jurisdictions can be the hardest part of any collateral project; modern entities have grown up through siloes, acquisitions and regionalised technology purchasing decisions. Inventory management requires breaking through these legal, organisational, operational and technology obstacles.

Firms talk about the value of metadata, or descriptive data that inform what can be done with individual pieces of collateral depending on each repo or securities lending agreement (Global Master Repurchase Agreement /Global Master Securities Lending Agreement) and other client agreements. For example, a client agreement stating that Security A cannot be rehypothecated takes it out of the running for pledge to a counterparty. That same agreement may also influence the cost of the trade to the client, comparable to if a client will accept equities compared to government bonds, or if pledge back might reduce the bank’s exposure (and regulatory capital impact) and capture better pricing. On the other hand, many assets have no restrictions. Categorising each asset in a consistent way delivers the supporting data that firms need to deploy collateral for the best results.

Part of the sources and uses analysis is looking at the layers of complexity: Graham Gooden, Head of EMEA Triparty, Trading Services at J.P. Morgan, notes that “utilising collateral at the right place, right time and right structure is a key element to a successful optimisation programme.” This structure may include a repo shell, a cleared derivative, pledged or title transferred, or something else. The same collateral holding can take on different balance sheet treatment depending on the right allocation; this is a subtle but important part of the optimisation analysis for firms that are ready for this step. Collateral uses are also on the minds of service providers that are looking to deliver optimised solutions for clients on a wider basis.

Some firms engage in extensive pricing of collateral while others do not, and some firms have developed their own cross-product pricing databases or use vendor data. S&P Global has reported on wide spreads between repo and securities lending rates for the same ISIN; knowing the opportunity to deploy collateral in one market vs. the other can make a difference of up to 18% in unique cases. For those that price, the ability to look across markets and have the legal agreements in place to execute on optimal pricing decisions is the next part of the process. There is little value in pricing corporate bond collateral for a repo trade if there are no Global Master Repo Agreements in place that accept corporate bonds in a shell.

The deployment of collateral to specific counterparties is often revisited daily as part of what-if exercises to find the best mix of uses. More sophisticated firms talk about conducting this analysis on a sub-CUSIP, ISIN or SEDOL level, where they will break up their holdings of a security into smaller quantities for discrete uses. This may solve limitations with counterparties, for example where no more than 5% of collateral may be from a single issuer. This approach is a departure from previous models when only groups of securities were considered as possible collateral pools.

To look at a single transaction, a hedge fund client could buy equity securities on margin that can be rehypothecated. The dealer is paid interest on the margin loan to the hedge fund but also has a balance sheet impact that could be mitigated if the securities were exchanged for cash or High Quality Liquid Assets like government bonds. The dealer could repo out the equities in a shell and pay a rate that would result in less earnings on the trade but a much reduced balance sheet cost; this would enable capacity and reduce funding charges. Or, the dealer could post the equities as collateral to a counterparty in an OTC derivatives transaction with government bonds as the reference security, if the Credit Support Annex accepts equities, and avoid paying the fee on the repo transaction. While the multivariate nature of risk and capital calculations rarely, if ever, results in a one-for-one exposure trade, there are multiple opportunities to mitigate costs when collateral can be appropriately moved to the right counterparties for the right purpose.

Can optimisation benefits be quantified?

Firms have begun to put a hard number on the financial benefits of optimising individual pieces of collateral, which can then be aggregated to a total number to state that “we have saved/earned US$X this year through collateral optimisation efforts.” This could be a function of relative P&L opportunities; where one scarce resource was used (Liquidity Coverage Ratio) but another was gained back (Leverage Ratio); or balancing tenor vs. duration vs. cost. Some firms say they can produce a specific Return on Assets (ROA) figure but do not want to reveal the specifics of their models.

Another way to look at the benefits is in capacity constraints: can optimisation allow the firm to do more business when leverage, capital and liquidity are all taken into consideration. A capital constrained market could be a primary reason to invest in optimisation. In practice however, firms said that this was a factor but not the biggest one. Most of their analysis focused on revenue gains and cost savings using what-if scenario tools and collateral pricing.

Multiple firms talked about the work they have done to organise and clean their data sets to be ready for optimisation. Banks in particular stated that getting to robust optimisation takes a consistent, firm-wide effort to ensure clean data. This is the real work of the effort and requires both an upfront investment and ongoing maintenance.

To support this effort, some of the recent innovation by triparty agents in the optimisation space is less around the algorithms themselves and more in automating and facilitating data inputs. These may include real time positions, eligibility, reference data, pricing and concentration limits. A more efficient data exchange makes the end process easier for clients and adds operational scale. It also enables clients to more comfortably choose between using internal optimisation algorithms or the triparty agent’s models without sacrificing the data integrity that is critical to execution.

J.P. Morgan is supporting the road ahead

No firm says that they have reached the end-stage of collateral optimisation: there are always new requirements, new assets and new clients to consider. That said, some ranked themselves a four out of five in terms of how complete their systems and processes were today. None said that they planned to do anything different in an era of regulatory change; even if risk or capital rules are modified, the building blocks of collateral optimisation represent best business practices. The types of optimisation may need evaluation however, not only focused on the collateral asset, product or counterparty but increasingly on the structuring of the various arrangements, whether pledge verses title transfer or the relative benefits of central counterparties such as CBOE Clear’s securities lending CCP.

The off-the-shelf, in-built triparty optimisation functionality often described as rules-based allocations has evolved a long way from a single monolithic algorithm. The ability to configure different rule sets to subsets of assets or counterparties and the ability for borrowers to apply overlays can go a long way to achieving an individual firm’s optimisation objectives. While all firms opt for this approach to start, J.P. Morgan has the expectation that clients will take an increasingly bespoke approach to collateral optimisation over time. James Forman, Senior Vice President at Jefferies, recently noted that “J.P. Morgan Triparty started as a regular triparty platform for us but now they are in our strategic trading models going forward.” Another senior market participant cited the importance of J.P. Morgan Triparty as part of their overall collateral ecosystem.

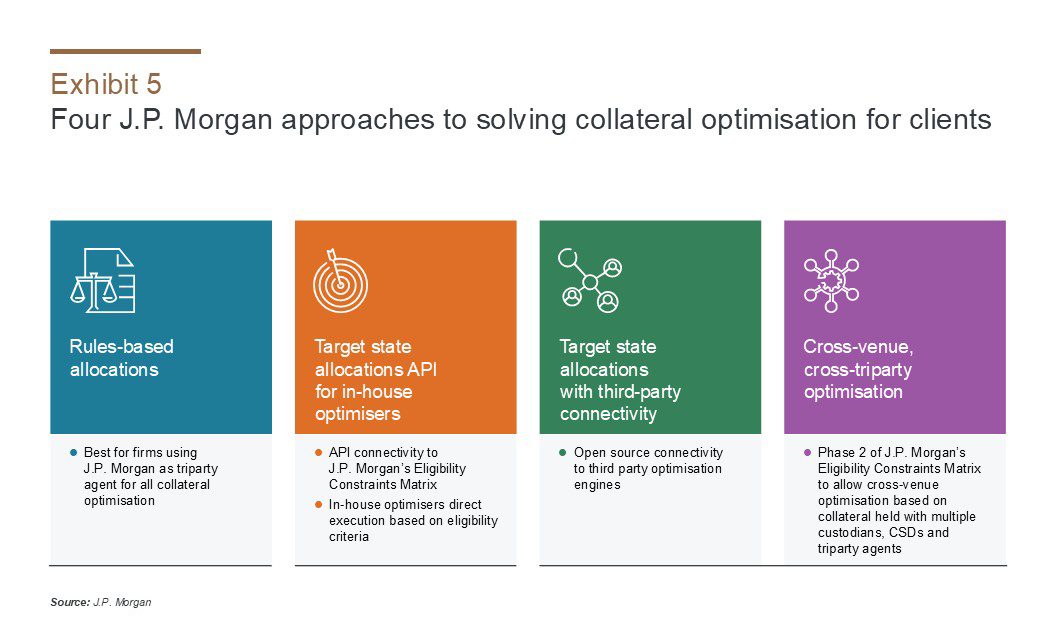

J.P. Morgan now offers three optimisation models for clients with a fourth to launch shortly, including rules-based ‘Target State’ allocations (ordered lists) and connecting with both in-house and third party vendor optimisation engines (see Exhibit 5). The next imminent stage is enabling a broad, customisable view of what-if optimisation scenarios incorporating data from any custodian, central securities depository (CSD) or other triparty agents.

The use of J.P. Morgan Triparty Services has improved outcomes for a wide range of market participants on the buy-side and sell-side; even firms with no technology or focused staff can meet their counterparty requirements in an automated and flexible way. An important part of this outsourcing is the ability to send and receive accurate data on holdings and exposures that can be captured by other systems; even if firms have not cleaned their global inventory holdings, the assets held in triparty benefit from the agent’s efforts. This part of industry standardisation helps everyone across Straight-through Processing, reporting and quantifiable data used for counterparty discussions.

Alongside technology, triparty and collateral optimisation remain in part a relationship business; collateral can only be deployed when there are counterparties ready to receive it. As a leading triparty agent, J.P. Morgan knows borrower and lender interest and works to connect potential new partners.

There is never likely to be a standardised market for collateral optimisation services and that is to the advantage of each market participant. With this in mind, the role of J.P. Morgan Triparty Services is to deliver a multi-asset class, follow-the-sun model covering all products and increasingly unlocking new markets with previously trapped assets. This is the future of collateral optimisation: while some clients say that standardisation would be a benefit, in practice every participant is at their own stage of the optimisation journey, which helps create competitive advantages and differentiation. In collateral optimisation, being independent and partnering with service providers that understand individual goals will put firms on the pathway to success.