The Bank of Canada (BoC) released its mandatory review, known as the sunset review, of the CORRA methodology, which happens every 5 years to ensure CORRA remains representative of the market it measures, and the data source and the data providers remain optimal for the calculation of the benchmark. This is the first sunset review of CORRA.

Since the BoC became the administrator of CORRA in June 2020, there have been several changes to Government of Canada (GoC) debt and repo markets:

- The government of Canada (GoC) securities market has grown rapidly since the COVID pandemic.

- BoC became a larger holder of GoC securities following exceptional asset purchases undertaken during COVID and is now more active and at times a large participant in the repo market.

- The GoC through its morning Receiver General (AM RG) auctions, has also become a large participant in the repo market.

- The industry move from T+2 to T+1 settlement in the cash bond market on May 27, 2024 has shifted volumes from the tomorrow/next repo market into the overnight repo market, increasing the amount of CORRA-eligible transactions and changing the shape of CORRA’s distribution.

The analysis of potential methodological changes is limited by a lack of a true counterfactual. Simulating new methods (e.g., trim rate, BoC/GoC repo trade inclusion) using historical data implicitly (and potentially falsely) assumes no change in market participant behaviors, even as CORRA and other reported statistics would have been different. Moreover, the introduction of the Canadian Collateral Management Service (CCMS), a tri-party collateral management service offered by the TMX Group and Clearstream, will structurally change the Canadian repo market.

Through the trading of general collateral (GC) baskets, the service will enable the clear identification of GC trades. Therefore, these trades will not require trimming, which will require changes to CORRA’s methodology. However, it would be premature to recommend methodological changes to account for CCMS in this sunset review due to the risk of having to make subsequent revisions as market participants broaden their adoption of CCMS.

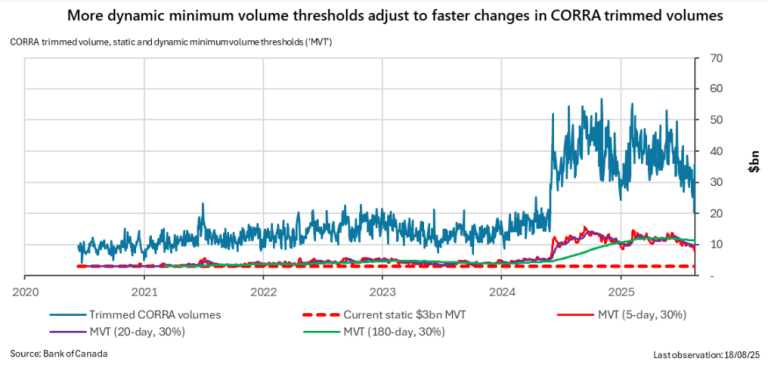

One recommendation from the BoC is to change the minimum volume threshold (MVT) to be dynamic and calculated as 30% of the 5-day moving average of CORRA trimmed volumes. The dynamic MVT retains $3 billion as a minimum value to ensure representativeness in the possible, but unlikely event CORRA volumes were to decline significantly.

The BoC called to continue to exclude BoC and GoC overnight repo transactions from the CORRA calculation. Although the BoC and GoC are now at times large participants in the repo market, the initial rationale for excluding these transactions from CORRA remains relevant. Specifically, the BoC and GoC transactions do not necessarily reflect broader market conditions and only a subset of market participants are eligible counterparties to these trades.

The BoC called to continue to exclude BoC and GoC overnight repo transactions from the CORRA calculation. Although the BoC and GoC are now at times large participants in the repo market, the initial rationale for excluding these transactions from CORRA remains relevant. Specifically, the BoC and GoC transactions do not necessarily reflect broader market conditions and only a subset of market participants are eligible counterparties to these trades.

Moreover, the BoC’s overnight repos generally clear at or near its policy rate, below the rates prevailing in the market. Including the BoC’s overnight repos could therefore be perceived as influencing the benchmark, which would not be aligned with the International Organization of Securities Commission’s (IOSCO) Principles for Financial Benchmarks. Such perceptions could reduce confidence in CORRA as a financial benchmark.

“Although the size of repo trades with the BoC and GoC has increased, the initial justification for the exclusion of these trades has not changed. Despite recent periods of increased activity, the Bank’s operations continue to be ad-hoc, as warranted by market conditions,” the BoC wrote.

Finally, the expected increased adoption of CCMS triparty will likely trigger an ad hoc review to account for features like GC baskets, which do not need to be trimmed. Thus, any potential improvements from using a different trim method are not material enough to warrant a change now and may need to be reversed once the methodology is updated to account for CCMS basket trades. Instead, BoC staff recommended the industry to leave the current 25th percentile trim method unchanged and to consider an ad-hoc sunset review once greater CCMS adoption is realized.

Fallback rate

Benchmark interest rates should exhibit robust underlying volumes. CORRA’s minimum value threshold (MVT) is meant to ensure that the benchmark rate represents broad conditions in the market for overnight GC repo funding in GoC securities. If CORRA’s trimmed volume for the day is below the MVT (currently $3 billion), CORRA will be set at the ‘fallback rate’ using the approved fallback methodology. At current volumes, the $3billion MVT is likely no longer representative of the market.

When CORRA’s new methodology was developed, the $3 billion static MVT represented around 30% of average daily volume of about $10 billion. However, following the industry move to T+1 settlement in May 2024, CORRA trimmed volumes increased to around $40bn on average. Thus, a $3 billion MVT now represents less than 10% of the daily average CORRA trimmed volumes.

Changing to a dynamic MVT would be an improvement Two options for a revised MVT were considered — a higher static MVT, and a more dynamic MVT. The static MVT could be revised higher to $10-15 billion, which would be similar to the 30% volume share prior to T+1 settlement. However, the primary drawback of this continued static approach is that the MVT may need to be updated again if volumes change materially, either up or down. Among the catalysts that could change CORRA volumes in the medium-term are:

- A change in participation in the GoC markets from participants like hedge funds

- Increased issuance by the government

- An increase in collateral efficiency as CCMS is broadly adopted

- If volumes were to increase, the MVT may again become too small to be representative.

- If volumes were to decline materially, there is a risk that CORRA could be set using the fallback rate for an extended period. A dynamic MVT would likely eliminate the need for future revisions.