The Basel Committee on Banking Supervision (BCBS) has released a consultation document that looks to operationalize what we’ve seen previously from the Financial Stability Board on haircuts for Securities Finance Transactions (SFTs). We provide a read-through of the document and highlight some areas we see as possible concerns.

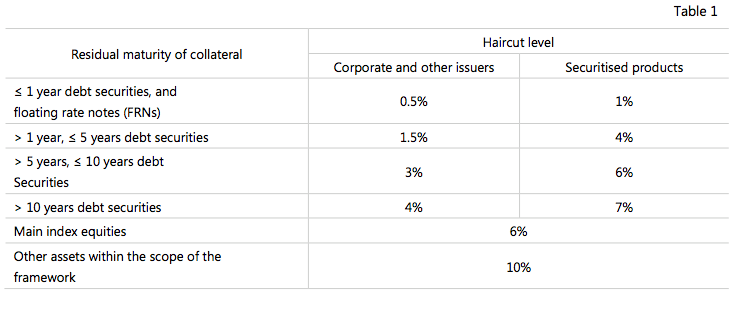

This Basel document picks up where the FSB left off in “Strengthening Oversight and Regulation of Shadow Banking – Regulatory framework for haircuts on non-centrally cleared securities financing transactions,” October 2014. That doc presented the haircut floors that the BCBS is formally proposing to adopt now. They are pretty straight-forward (see Table 1) and in some cases are less than what the market charges now, for example equity haircuts in US tri-party repo (the median is 8% compared to the table’s 6%). Some of the haircuts are lower than what borrowers post to lenders for securities loans with equities as collateral (8% to 15% vs. 6%).

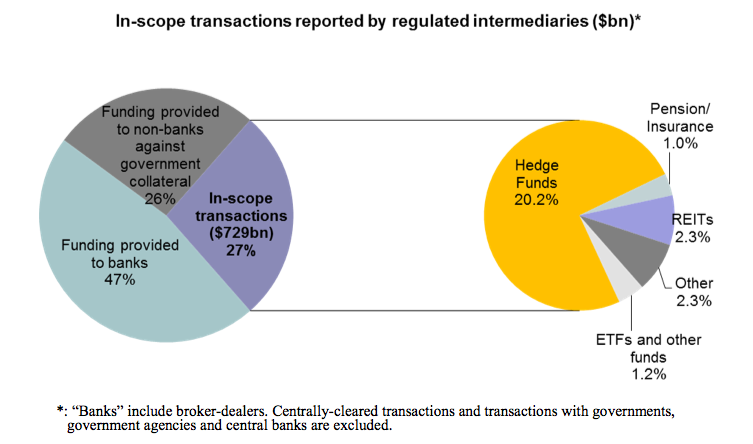

The setup of the FSB and BCBS docs is that banks can charge any haircut they want, but that haircuts underneath the minimum levels will have “significantly higher capital requirements,” mentioned throughout the document as being calculated like an unsecured loan instead of a secured loan. The haircuts apply to a pretty limited set of transactions though, about 27% of the universe of SFTs. From the FSB Oct 2014 document, the majority of this is prime broker loans to hedge funds not associated with government securities.

There are a mess of exemptions for these haircuts, which is how the FSB got to the limited set of transactions above. From the BCBS doc, the haircuts will apply to SFT transactions are that are:

(i) Non-centrally cleared

(ii) Cash-lent-for-collateral with non-banks or collateral-lent-for-collateral with non-banks

(iii) Not referencing government securities

(iv) Not SFTs traded with central banks

(v) Not SFTs where the primary motive is to borrow securities rather than lend cash

(vi) Not collateral-lent-for-collateral where collateral is not re-hypothecable

Interestingly, transactions where banks support direct securities lender to hedge fund arrangements could be seen as applicable to the haircut rule even though the bank takes no principal transaction. We expect this will be a question that comes up later for clarification.

The FSB and BCBS are both wise to two arbitrage opportunities that the rules create and specifically disallow them:

(i) Arbitrage between long and short SFT positions using the same security

(ii) Arbitrage using upgrade of collateral with a security not subject to the FSB proposal

“The higher capital requirements apply at the transaction level and only to the transactions in scope whether or not the transaction is contained in a netting set.” Basically banks have to calculate haircuts based on individual and then portfolio-level transactions and take the more expensive result.

There are some rules on cash collateral that we could see causing a pretty immediate problem for beneficial owners taking any level of risk in their securities lending cash portfolios. We see the push towards conservatism in cash collateral reinvestments as going with the majority of the industry’s current practices but also substantially reducing opportunity, and hence the rationale for lending at all, for a portion of the market. According to the proposal:

“Assets which the securities lender and/or its agent hold to meet cash collateral calls should be highly liquid with transparent pricing so that they can be valued at least on a daily basis and sold, if needed, at a price close to their pre-sale valuation.” Does that mean no more two-year floaters, or long-dated ABS repo? These assets could be at direct risk for securities lending cash collateral pools.

This is the consultation paper only so these rules are subject to change. Its a pretty good idea of where regulators are heading though.

Here are links to they key documents:

Haircut floors for non-centrally cleared securities financing transactions – consultative document