‘No one length fits all’ – haircuts in the repo market

by Miruna-Daniela Ivan, Joshua Lillis, Eduardo Maqui and Carlos Cañon Salazar

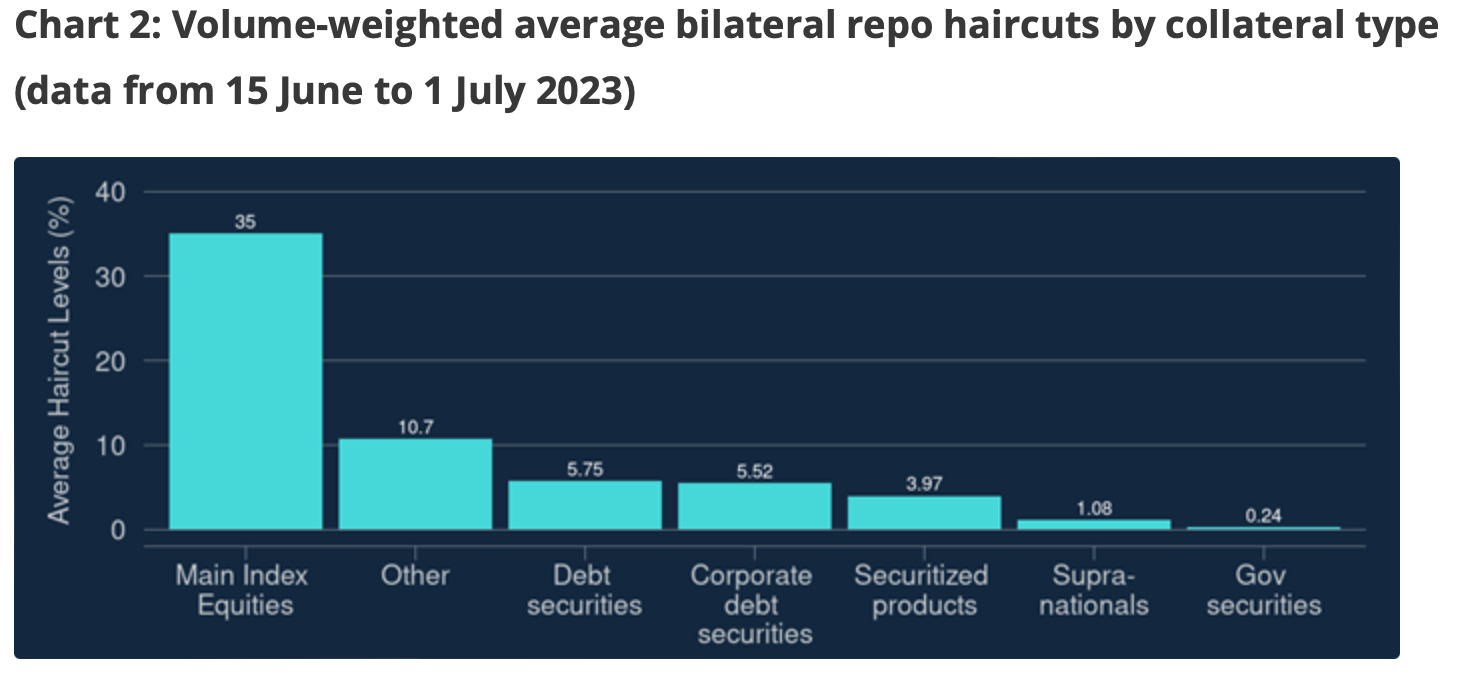

Looking through different collateral types in the bilateral repo market, haircuts typically increase with the market risk (interest rate and liquidity) of the underlying collateral (Chart 2). Government debt securities – widely recognised as the ‘safest’ non-cash assets – have an average haircut of close to zero in bilateral transactions between dealer banks and NBFIs. Consistent with Julliard et al (2022), we find that within the government bond repo market, haircuts reflect, in part, the risk of fluctuations in the collateral price (interest-rate risk). Longer-dated collateralised bonds generally involve higher haircuts largely due to being more sensitive to interest rate changes. Meanwhile, repo backed by riskier debt securities – such as debt issued by banks and NBFIs – attracts average haircuts of over 5%, but this remains far smaller than the 35% average haircuts on main index equity repos.

Examining the government bond repo market in more detail, SFTR data show that gilt repo haircuts are generally near-zero (between 0%–2%). Meanwhile, haircuts on repo transactions backed by US Treasury securities are at or below 0.5% for most of our sample, with a notable increase (to nearly 1.5%) around the time of the Spring 2023 banking sector turmoil (Chart 3). This slight variation in haircut levels across government bond repo provides some further evidence that the level of haircuts also reflects the degree of market liquidity in the underlying collateral securities.

Editor’s note: we think it takes some bravery to work with SFTR data in this way. While the transactions volumes have generally been correct, previous analysis has shown that the collateral data have been historically faulty – not even close for analysis. The authors are working with non-public data that may result in more accurate conclusions. However, casual readers should compared to the results with their own experience.

The full article is available at https://bankunderground.co.uk/2024/07/10/no-one-length-fits-all-haircuts-in-the-repo-market/