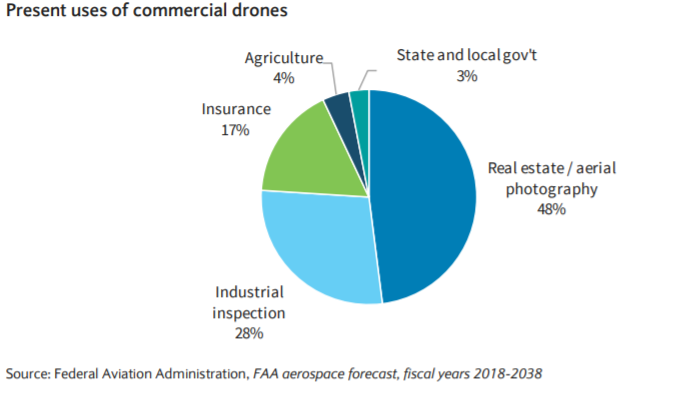

Commercial drones provide an avenue for cost reduction ($100bn) and safety improvement which will drive widespread adoption in the coming years, according to a report from Barclays. Of the sectors highlighted, insurance was presented as companies are in the early stages of adopting drones.

Early adopters are leveraging drones for a few broad use cases. Barclays categorizes the first use case as risk assessment. Risk assessment involves collecting data to more accurately determine risk-weighted premiums for a given area and capturing images that can be used for comparative purposes during future claim evaluations. Using drones for risk assessment will allow insurance companies to more accurately assess their liabilities and theoretically reduce unanticipated costs.

Barclays categorizes the second use case as damage evaluation. Drones can promote much more rapid damage evaluation following natural disasters – especially in areas that may be inaccessible for insurance agents to reach in person. To this point, Aviva used drones to assess flood damage in the UK in 2016, which allowed for more efficient resource allocation.

The insurance industry has been one of the early adopters of commercial drone technology, particularly following record-level insured catastrophe losses in 2017. Commercial P&C re/insurers including Allstate, AIG, Travelers, Hartford, State Farm, Chubb, and Everest Re continue to invest in drone technology, either through partnerships with drone-focused insurtech companies, or building the capabilities in-house.

As a point of reference, the use of drones is expected to result in annual cost savings of $6.8 billion for the insurance industry and drone sales to the insurance industry could reach $0.8 billion as a result of more efficient claims processing, better underwriting, improved employee safety, and reduction in fraud:

Claims processing – Insurers are primarily leveraging drones to more quickly estimate property damage and expedite claims processing, particularly following catastrophe events (including hurricanes and wildfires). Drones are especially helpful when catastrophes limit insurers’ physical access to the loss-impacted areas. For example, Travelers has said that it had ~500 commercial drones prepared to inspect damaged properties post-Hurricane Florence, which provided the company with a competitive advantage in claims handling.

Underwriting – The use of drone imagery could help insurers more accurately assess property values and conditions prior to issuing policies, which can lead to more precise pricing. Of note, adoption of drone technology on underwriting has been slower than on the claims processing side.

Employee safety – By using drones to assess damaged areas instead of employees, insurers can reduce workers’ compensation claims from potential injuries.

Fraud monitoring and prevention – Insurers can use drone images taken prior to a loss event to potentially disprove fraudulent claims. As a point of reference, fraudulent insurance claims amount to ~$32bn of loss costs annually, according to the Insurance Information Institute.