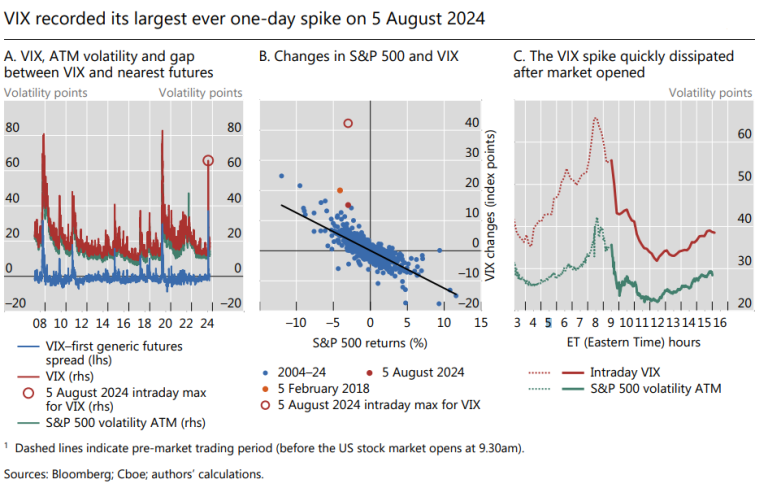

On 5 August 2024, the Cboe volatility index (VIX) derived from option prices on the S&P 500 recorded its biggest ever one-day spike, increasing by 180% to almost 66 pre-market (ie before the US market open). In a recent bulletin, researchers from the Bank for International Settlements (BIS) delve into this episode for clues to the possible reasons for the spike.

Their analysis indicates that the asymmetric widening of bid-ask spreads likely played a key role in exacerbating the spike, as it lifted mid-quotes of option prices used in the calculation of VIX. Market makers’ (MMs) adjustment of quotes was behind the widening, as MMs sought to avert an imbalanced book in uncertain conditions. These effects were particularly strong for less liquid put options, which have an outsize impact on the calculation of VIX and accounted for more than 85% of the spike.

As for alternative reasons, they appeared to have played a less important role. VIX ETFs, MMs’ option hedging, and so-called dispersion trades – which typically bet on lower correlation among S&P 500 stocks – do not seem to have contributed meaningfully to the spike. The increase in correlations and a commonly used dispersion index were not unusual compared with the outsize jump in VIX.

Another often discussed amplification channel due to MMs’ option hedging is unlikely to explain the observed patterns either. Our findings highlight the possibility that the calculation of VIX makes it vulnerable to a widening of bid-ask spread quotes regardless of a fundamental rise in underlying volatility. The outsize role of less liquid put options in the calculation of VIX exacerbates these problems. Given the subdued liquidity in overnight option markets and reliance on quotes instead of trades in the VIX methodology, pre-market readings of VIX may be less informative than those during regular trading hours.