Prime funds can sometimes be overlooked by investors in favor of government and treasury funds. A new piece of analysis based on data from BNY Mellon’s Liquidity DIRECT reveals that not only are prime funds delivering investors superior yields over other money funds, the funds are doing so with remarkable stability and consistency.

October 2016 witnessed the enactment of major reforms to US money market funds, as the Securities and Exchange Commission (SEC) introduced sweeping changes in the rules governing treasury, government and prime funds. Like treasury and government structures, prime funds invest in US Treasuries and US government debt, but prime funds are distinguished by the fact that these vehicles also invest in corporate credit instruments. These corporate instruments can provide investors higher yields relative to other money market fund structures.

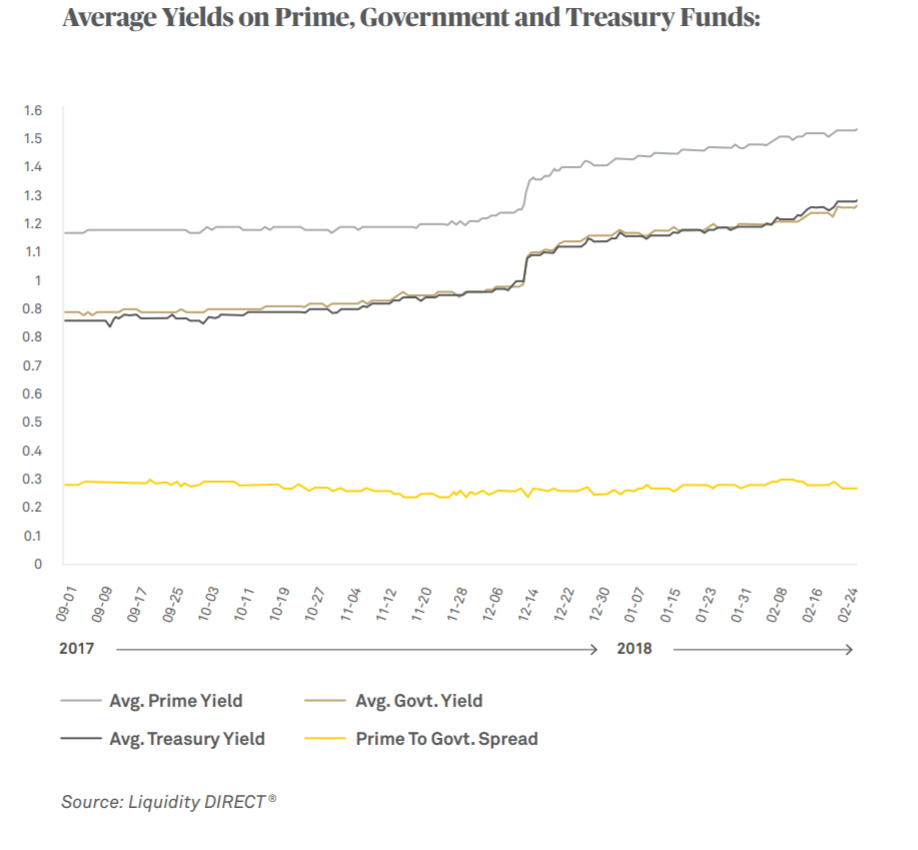

The intent of the 2016 reforms was to strengthen the resiliency of money market funds and, in any future market turbulence, to limit the kind of large-scale redemptions witnessed in 2008 after the Reserve Primary Fund “broke the buck”. In order to gauge the impact of these reforms, BNY Mellon has analyzed data going back to October 2016 but has focused in particular on the six-month period between September 2017 and February 2018. In this paper, BNY Mellon presents some of the findings from its analysis and outlines observations supporting its primary conclusion: investors should reexamine the allocation of prime funds in their portfolio, given the superior returns achievable relative to other money market vehicles and the comparable high degree of NAV stability.

BNY Mellon’s analysis definitively found that in the months since the 2016 reforms, prime funds have presented investors with enhanced yield relative to other money market instruments while also maintaining stable NAVs, very similar to those achieved by government and treasury funds. Barring a huge loss to the fund that dramatically drags down its NAV, a prime fund will in most circumstances outperform the yield available in either government or treasury funds by a very wide margin.