To increase market transparency, the BoE intends to use new data to publish summary statistics of activity in the broader sterling money markets on a regular basis. The BoE now collects granular data on sterling money market transactions, providing new insights into these markets. A subset of these Sterling Money Market (SMM) data will, from April, be used as the inputs to the sterling overnight index average (SONIA) benchmark, as planned reforms take effect.

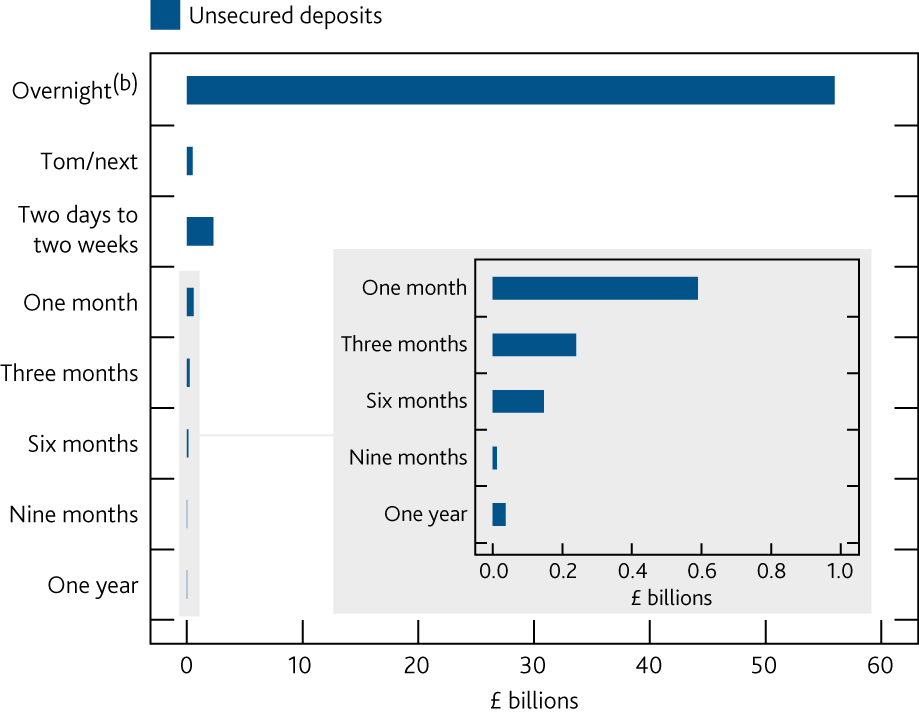

In an article, Rob Harris and Tim Taylor of the Bank’s Markets Directorate, write how the BoE also use this new, comprehensive data set to shed light on the market for term unsecured deposits. Transactions are overwhelmingly completed overnight. Beyond that maturity, the average daily value of term deposit transactions is generally low, rarely exceeding £1 billion at maturities of one month or longer. Average rates at these terms are also highly volatile, albeit around a clear trend.

By comparison, the average value of transactions soon to underpin SONIA – capturing overnight unsecured deposits which are £25 million or larger – has been on average close to £50 billion per day, and the headline rate is very stable. Underlying this stability, analysis suggests that there is an active core of depositors in the overnight unsecured market measured by SONIA. Researchers find evidence of a dynamic pattern of bank-depositor relationships, consistent with a competitive market environment where depositors can, and do, move their business around.

Sources: SMM data collection and Bank calculations.

(a) Daily average from 1 September to 30 November 2017, by original maturity.

(b) With a minimum transaction size of £1 million. Transactions underpinning reformed SONIA are £25 million or greater.

The SMM data also show strong levels of activity in the overnight gilt repo market. Harris and Taylor show that rates vary according to the collateral used in these transactions and that the distribution of rates varies considerably over time.

Observations support the direction of ongoing market-led reforms to how interest rate benchmarks are used in sterling financial markets. A desire for benchmarks to be based on transactions implies a shift away from LIBOR towards overnight benchmarks. In sterling the market’s preferred alternative, SONIA, provides a robust alternative to Libor without the additional complexities that can affect gilt repo rates.