Several years after the adoption of central bank digital currencies (CBDCs), the evidence shows that the CBDCs in both Jamaica and The Bahamas have failed to gain traction with either consumers or businesses. Instead, the CBDCs have become little more than vehicles for government handouts — distributed through limited-time giveaways and incentive programs, with little lasting use. These early experiments provide a cautionary tale for other governments weighing whether to launch a CBDC, writes the Cato Institute.

Almost every increase in the Jamaican CBDC is tied to government incentives. Consider the first the initial increase to J$1 million ($6,330) in September 2021. As reported by the central bank in the Jamaica Information Service, this early jump was due to the Bank of Jamaica giving J$1 million ($6,330) in CBDC to its staff. Similarly, the next increase — in November 2021 — occurred because the Bank of Jamaica issued J$5 million ($31,650) to National Commercial Bank.16 However, in this instance, National Commercial Bank paid for the CBDC transfer through Jamaica’s real-time gross settlement system in a manner similar to requesting physical cash.

The only increase that cannot be accounted for with publicly available information was in May 2024. However, the Bank of Jamaica confirmed via email that the J$200,000 ($1,273) increase occurred because of a request by a wallet provider.

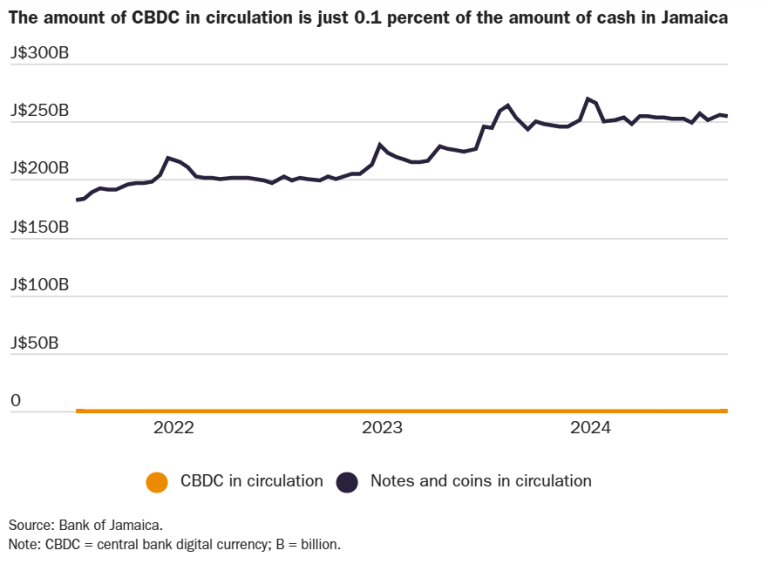

When viewed in a vacuum, some people may consider it impressive that the amount of CBDC in circulation went from zero to more than J$257 million ($1.64 million) in three years. When viewed in context, however, the reason for this increase is not because the CBDC had solved the issues that had been weighing on Jamaican citizens. Rather, the reason was that the Jamaican government had given the money away.

In the Bahamas, the changes over time resemble the experience in Jamaica, although changes in the amount of CBDC in circulation in The Bahamas have been more frequent. Reflecting on the lack of consumer adoption in 2024, Central Bank of The Bahamas governor John Rolle said commercial banks would soon be forced to distribute the CBDC—suggesting a shift from incentives to mandates.

When asked why central banks have struggled to get people to adopt CBDCs, government officials have provided several possibilities. In Jamaica, the central bank said people were not interested in adopting a new system when they can already make digital payments.54 In The Bahamas, the central bank said the COVID-19 pandemic made it difficult to promote CBDC use. Reflecting on these statements, it seems that the common thread is that a CBDC is not an effective policy tool. Governments may build CBDCs, but that does not mean people will use them. People are served well by cash, prepaid cards, debit cards, credit cards, payment apps, and cryptocurrencies. They don’t need the government to reinvent the wheel.