IOSCO released their third hedge fund survey last week with some expected results and some new information. Most importantly, we have to get used to their definitions of leverage and how the data are measured. There were some changes from last year.

In their second hedge fund survey from 2013 (“IOSCO builds new measurements for hedge fund leverage; this is a work in progress but shows good forward momentum“) IOSCO promoted an idea called the Gross Notional Leverage, which tried to capture all the economic impacts of leverage in the hedge fund industry including derivatives exposure. GNE makes an appearance again in the third hedge fund survey but not the data. According to IOSCO:

“Despite some limitations of this metric, such as the fact that it is heavily skewed by positions in interest rate derivatives, it provides a complete appreciation of the leverage employed by a fund to gain market exposure, incorporating both financial leverage and synthetic leverage. GNE does not directly represent an amount of money (or value) that is at risk in a fund. Instead, it is a conservative measure of the economic or market exposure of the fund positions by looking through to the underlying assets.”

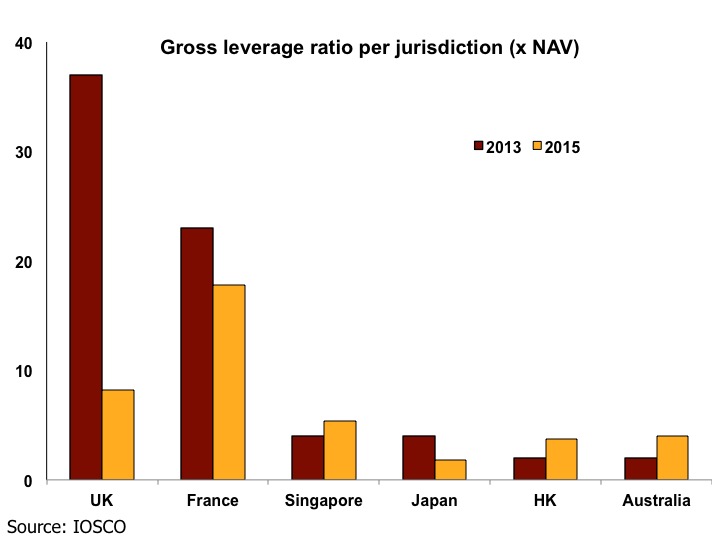

Instead of the GNE from 2013, IOSCO goes straight to gross leverage: “The gross leverage ratio is presented here as the proportion of GNE to NAV.” Its a slightly roundabout way of looking at leverage but now that we have two years of data with the same methodology, it becomes easier to get a read on.

The data this year (collected in 2014) show a sharp decrease in gross leverage from the second survey (data collected in 2012) in Europe and an increase in Asian countries.

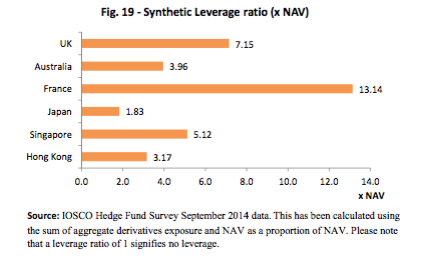

Meanwhile, synthetic leverage represents most of the overall leverage. This was a data point missing in the second hedge fund survey and we are glad to see it incorporated here. This was one of the most valuable parts of the old UK FSA hedge fund surveys that we were sorry to lose. Although the IOSCO data are less transparent to read, at least this is something.

Should we believe these leverage data points? Yes and no. They might be the only game in town right now but even IOSCO cautions against using the data indiscriminately. “In relation to the data reported by France, the average of the small sample was significantly impacted by the amount of synthetic leverage reported by one fund reflecting its substantial use of interest rate derivatives. With respect to the UK sample, the synthetic leverage was similarly skewed by two particular funds in relation to their use of interest rate derivatives. This advises caution when comparing aggregate leverage statistics across jurisdictions since these may be skewed by a few single funds.”

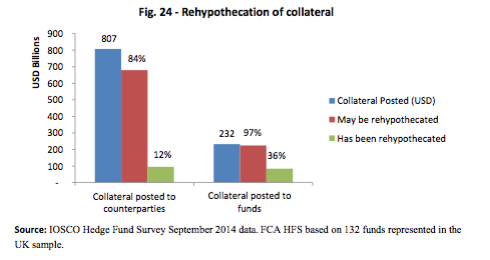

Another good new addition to the IOSCO survey is information on hedge fund collateral rehypothecation. This may be the first time that this type of data has been published, which helps to set out new parameters in understanding the broad collateral rehypothecation patterns of hedge funds. In particular, note the low actual rehypothecation of collateral compared to allowable rehypothecation.

A link to IOSCO’s third hedge fund survey is here.