Citi Investor Services released findings from a new report that tracks views of the structural shifts reshaping the global asset management industry. Primary findings include:

- Ongoing industry challenges are coinciding with new opportunities: More than half of respondents cited new inflows going to mega players, the rise of passive funds, accelerating fee compression, and rising costs as key challenges.

- At the same time, new inter-linked growth drivers are emerging. 67% of respondents believe that the democratization of private markets will drive organic growth in their businesses over the next three years; 61% cited the advancement of artificial intelligence (AI) and generative AI (genAI), and 59% said intergenerational wealth transfer from Baby Boomers will contribute to their growth.

- Small step, not big leaps, mark the rise of AI and genAI: While AI and genAI are expected to reshape operating models, the adoption rate is moderate, with 41% of respondents at the implementation phase of AI, and 26% at the same phase for genAI. That said, a majority of respondents believe that AI and genAI will significantly impact investment processes, although legacy systems and concerns around data quality, security and transparency remain key barriers.

Outsourcing seclending

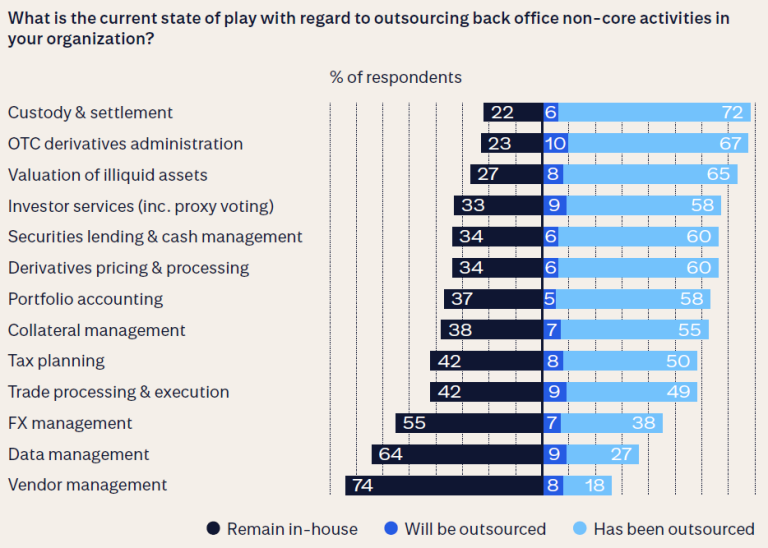

Outsourcing is linked with organic growth at lower costs: What started as a cost-cutting tactic is morphing into a strategic imperative with outsourcing creating tangible benefits on both the bottom line and organic growth. 59% of respondents noted the reduction of unit costs from outsourcing, and 57% acknowledged that it allows top executives to focus on core competencies.

The report further suggests industry service providers will need to advance and develop state-of-the art capabilities and innovate across front, middle, and back-office functions as asset managers continue to outsource in these areas and prioritize core competencies in-house.

Of the 13 main back office activities, ten have been outsourced by one in every two asset managers. The top five are: custody and settlement; OTC derivatives administration; valuation of illiquid assets; investors services (incl. proxy voting); and securities lending and cash management.

Chris Cox, global head of Investor Services at Citi, said in a statement: “The findings of this report underscore that asset managers are already future proofing their businesses, albeit at varying degrees. As a long-standing service provider to the industry, Citi’s priority is to enable our clients to effectively capture new and emerging opportunities for growth as outlined in the report. We continue to invest across capabilities, especially in our data and digital solutions, so we fully support our clients as their needs and operational models evolve and adapt to shifting industry dynamics.”