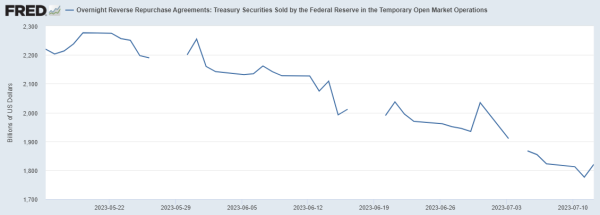

Following the debt ceiling resolution in June, bank economists had forecasted a glut of Treasury issuance in the range of ~$1 trillion T-Bills. With all that net issuance, there were fears that the repo market would not be able to absorb the excess supply of collateral and funding rates would spike higher, writes Victor Masotti, director of Repo Trading at independent prime broker Clear Street, in an emailed commentary.

“What we’ve seen over the past month is the reallocation of cash out of the RRP [Fed’s Reverse Repo Facility]. The RRP, where investors earn 5.05% interest on their cash, has declined by over $300bn to $1.7tn since the debt ceiling suspension. Cash investors have been quick to pull their cash from the Federal Reserve’s RRP and re-invest in overnight General Collateral, T-Bills, and Agency Discount Notes, which has alleviated any forecasted funding stress on repo rates due to increased Treasury issuance.”

“Lastly, repo term markets seem to be fully pricing in a 100% probability for an FOMC hike on July 26, while Futures markets are reflecting odds of a July hike closer to 90% likelihood,” he wrote.

Victor Masotti joined Clear Street as director of Repo Trading in October 2021. Prior to joining Clear Street, Victor held the title of US STIR Trading and vice president at TD Securities. He also previously held analyst positions at Société Générale, Merrill, and Meredith Whitney Advisory Group.