The European Banking Authority (EBA) published its Report on the impact and calibration of the Standardised Approach to Counterparty Credit Risk (SA-CCR), simplified SA-CCR and Original Exposure Method (OEM). The impact of setting alpha equal to 1 under SA-CCR for the purposes of the output floor (OF) on a permanent basis is also analyzed.

Estimated aggregate impact from the introduction of new counterparty credit risk (CCR) standard methods in the EU in terms of exposure value (EV) stands at -7.2% (+31% for the median bank). Larger banks mainly experienced negative impacts while banks with smaller derivative business displayed large positive impacts on CCR, but limited impact on total credit risk.

Derivative business mainly moved from the Mark-to-Market Method (MtM) to the SA-CCR. Compared to the old methods, margined business is better recognized under SA-CCR.

In terms of calibration, compared to the internal model method (IMM), SA-CCR produces EV figures 60% higher on average (+40% for the median bank). These results are in line with the Basel Committee on Banking Supervision (BCBS) objectives for the calibration of the SA-CCR framework.

Simplified SA-CCR EV figures are on average 60% higher than the SA-CCR ones (+40% for the median bank). The OEM is the most conservative approach: compared to simplified SA-CCR, average EV figures are 110% higher (+30% for the median bank). Setting alpha equal to 1 on a permanent basis under SA-CCR for the purposes of the OF reduces the impact of the OF only marginally (-0.2%).

In its proposal for a regulation amending the Capital Requirements Regulation (CRR3), the European Commission introduced an output floor (OF) to the risk-based capital requirements. Transitional arrangements are envisaged: for CCR, until 31 December 2029, institutions with Internal Model Method (IMM) permission, shall replace alpha by 1 in the SA-CCR calculation of the exposure value for their derivative contracts. This also includes the option for the Commission, after taking into account this EBA report, to permanently modify the value of alpha under SA-CCR used in the calculation of the exposure values of derivatives under the IMM for the OF. Therefore, the present report includes an analysis of the impact of setting alpha equal to 1 under SA-CCR for the purposes of the OF on a permanent basis.

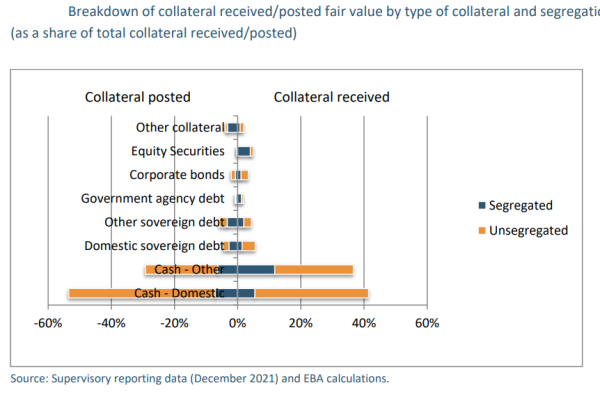

Collateral analysis

The EBA also provides an overview of the composition of collateral used in derivative transactions, breaking down the fair values of collateral received or posted by: a) the types of collateral exchanged; b) the amount of collateral that is exchanged as variation (VM) or initial margin (IM); and c) whether the collateral is segregated or unsegregated.

The largest part (70.4% posted and 57.8% received) of the collateral considered in the analysis is exchanged as variation margin (VM). VM is mainly unsegregated (88.6% of VM posted and 96.3% of VM received). On the contrary, initial margin (IM) is mainly segregated (54.9% posted and 60.6% received).

Regarding the type of collateral, cash in domestic currency is the main type of collateral used (53.5% collateral posted and 41.6% received), followed by cash in other currencies (29.2% collateral posted and 36.6% received). For IM, other types of collateral are also commonly exchanged, in particular sovereign debt and equity securities.