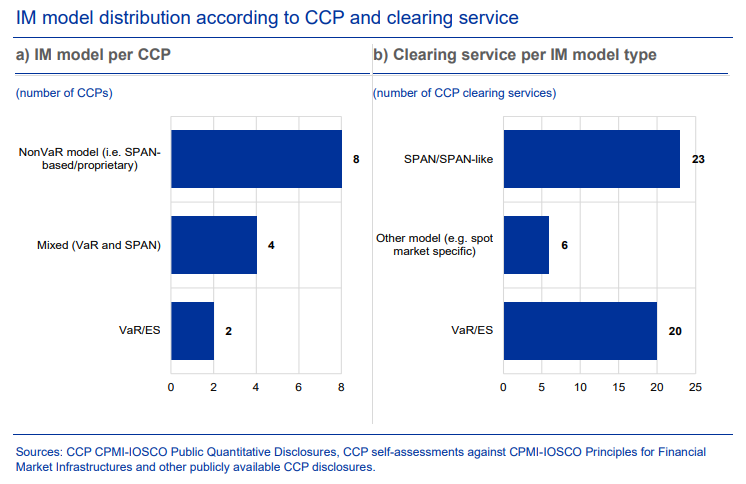

In a recent paper, researchers for the European Central Bank (ECB) aim to provide a holistic understanding of the Initial Margin (IM) models used by central counterparties (CCPs) in Europe. In addition to discussing their relevance in terms of CCP risk management and their importance for the functioning of financial markets, they provide an overview of the main modelling frameworks used, including Standard Portfolio Analysis of Risk (SPAN) and Value at Risk (VaR) models.

By leveraging on publicly available data, they provide an up-to-date picture of current modelling practices for specific cleared product classes, as well as various trends in IM modelling practices in Europe. Researchers show how IM model frameworks vary materially, depending on the CCP’s past choices and the products it clears. Despite a propensity to switch to VaR models, idiosyncrasies and differences across CCPs are likely to persist.

Researchers conclude by highlighting current and upcoming challenges and risks to CCP IM model frameworks and linking the current status quo with ongoing and upcoming regulatory work at European and international level.

Some of the observations relate to liquidity strains and difficulties in sourcing sufficient collateral to address increased margin calls, as experienced in practice by counterparties when confronted with large exogenous events (such as COVID-19 or turmoil related to the energy supply and related derivatives). These strains underscore the importance for financial stability of achieving additional transparency and an understanding of CCPs’ IM models by clearing members and their clients.