The European Central Bank (ECB) is launching a public consultation on its report on “Sound practices in counterparty credit risk governance and management”. The report summarizes the results of the targeted review performed in the second half of 2022 on how banks govern and manage counterparty credit risk (CCR). It highlights the good practices observed in the market and points to areas where improvement is needed.

CCR was identified as a supervisory priority for 2022-24, as banks had been increasingly offering capital market services to riskier, leveraged and less transparent counterparties, particularly non-bank financial institutions, incentivized by the search for yields in the then low-interest rate environment. Energy and commodity price volatility induced by the conflict in Ukraine prompted enhanced focus on banks’ exposures towards energy utilities and commodity traders.

In 2023, ECB Banking Supervision conducted off-site follow-up activities at 23 banks active in derivatives and securities financing transactions with non-banking counterparties. In some cases, the ECB also carried out on-site inspections.

The review found that, despite some progress in how banks measure and manage CCR, there is still room for improvement in areas such as customer due diligence, the definition of risk appetite, default management processes and stress testing frameworks. Supervisors’ expectations cover, among other dimensions, banks’ capacity to obtain information from non-bank counterparties, regularly stress test their counterparty credit risk exposures and assess their counterparties’ vulnerabilities under tail risk scenarios.

The good practices described in the report go beyond mere compliance with regulatory requirements and should be considered when banks design their approach to CCR. Approaches to CCR taken by banks should be proportionate to the scale and complexity of the business and products offered, as well as the nature of the counterparties.

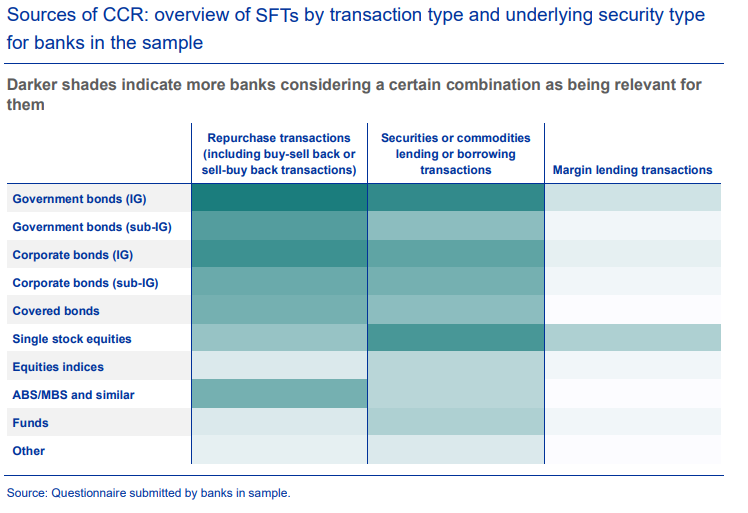

SFT watch

- In September 2000 the Basel Committee for Banking Supervision (BCBS) issued its “Principles for the Management of Credit Risk”, which highlighted the need for a clear and detailed definition of a bank’s strategy and risk tolerance for CCR arising from derivatives and securities financing transactions (SFTs) in the banking and trading books. The BCBS clarified that banks must receive sufficient information for a comprehensive assessment to be made of the true risk profile of a counterparty, including the counterparty’s capacity to repay based on historical trends and future projections under various scenarios.

- As of the date of the targeted review (31 March 2022), the banks selected held on aggregate approximately €1.245 trillion ($1.3tn) of CCR exposure value (of which, 59% was derivatives and 41% SFTs) and €278 billion of CCR risk-weighted exposure amount (RWEA) (of which, 82% was derivatives and 18% SFTs).

- Institutions subject to the targeted review and related on-site inspections also showed a mix of regulatory methodologies for computing CCR exposure values, with 17 banks using the internal models method (IMM) for derivatives and nine banks using this method for SFTs.

- The contractual possibility of collateral re-use (on both sides of a trade) in the context of SFTs is very high, underscoring the importance of sound collateral management and monitoring frameworks.

- There is still room for improvement in how, on a firm-wide basis, CCR is mitigated, monitored and managed when a counterparty is in trouble or defaults. In many cases, static margins have not yet been replaced with more risk-sensitive arrangements. Early warning indicators specific to derivatives and SFTs, such as discipline in margin payments, are not always considered when compiling watchlists.

Among the good practices for SFTs are:

- Presence of a three lines of defence model for CCR Institutions have dedicated, comprehensive governance and risk management frameworks in place to deal with increased CCR exposures from market activities in derivatives, SFTs or long settlement transactions. These frameworks include a welldefined three lines of defence model with proper allocation of responsibilities and clear reporting lines.

- Institutions implement risk policies explicitly reflecting their willingness to accept CCR resulting from derivatives and SFTs or other market activities with a long settlement.

- Market-makers in derivatives and SFTs regularly assess their own capabilities to close out positions, both under business-as-usual and in stressed markets, to ensure their ongoing ability to close out large hedging and collateral instruments. Safeguards and monitoring are set up for illiquid positions in the portfolio or in the collateral pool.