In this note, the Federal Reserve shows that nonbank lenders’ behavior as cash lenders can help discern early informative signals about the scarcity of reserves. Reserves, which are deposits that banks and other financial institutions hold at the Federal Reserve, are the most liquid asset on banks’ balance sheets and hence play a central role in banks’ liquidity management. The aggregate supply of reserves tends to decline when the Federal Reserve’s balance sheet shrinks, for instance, through quantitative tightening.

As reserves decline, banks may conserve liquidity by limiting their lending in overnight money markets, including secured (repo) and unsecured (federal funds) markets. With banks less eager to lend, nonbanks’ role as cash providers in these markets tends to increase, and their supply of liquidity can provide useful early signals for reserve scarcity. These early signals are valuable because reserve scarcity can lead to disruptions in funding markets, such as the sudden spikes in overnight rates seen in September 2019.

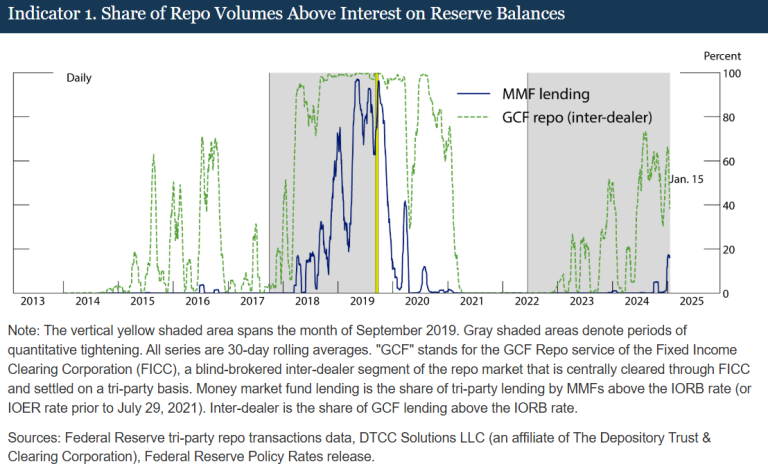

The authors focus on two critical nonbank suppliers of liquidity to money markets: money market funds (MMFs), the largest providers of cash in repo markets, and the Federal Home Loan Banks (FHLBs), the largest providers of cash in the federal funds market. The institution-based approach complements approaches that use aggregate market-based indicators for monitoring scarcity.

The Fed shows that four new indicators based on these institutions’ cash supply can help discern early informative signals about reserve scarcity:

- The proportion of MMF repo lending above the interest rate on reserve balances (IORB);

- The elasticity of MMF repo spreads to the balance in Treasury General Account (TGA);

- Volume and rates in the “true” domestic interbank fed funds market (i.e., transactions that do not involve FHLBs as lenders);

- FHLBs’ lending in the fed funds market at rates below their repo rates.