The results of the Federal Reserve Board’s annual bank stress test showed that while large banks would endure greater losses than last year’s test, they are well positioned to weather a severe recession and stay above minimum capital requirements. Additionally, the Fed published aggregate results from its first exploratory analysis, which will not affect bank capital requirements.

“This year’s stress test shows that large banks have sufficient capital to withstand a highly stressful scenario and meet their minimum capital ratios,” vice chair for Supervision Michael Barr said in a statement. “While the severity of this year’s stress test is similar to last year’s, the test resulted in higher losses because bank balance sheets are somewhat riskier and expenses are higher. The goal of our test is to help to ensure that banks have enough capital to absorb losses in a highly stressful scenario. This test shows that they do.”

The stress test is one tool to help ensure that large banks can support the economy during downturns. The test evaluates the resilience of large banks by estimating their capital levels, losses, revenue and expenses under a single hypothetical recession and financial market shock, using banks’ data as of the end of last year. The individual results from the stress test inform a bank’s capital requirements to help ensure a bank could survive a severe recession and financial market shock.

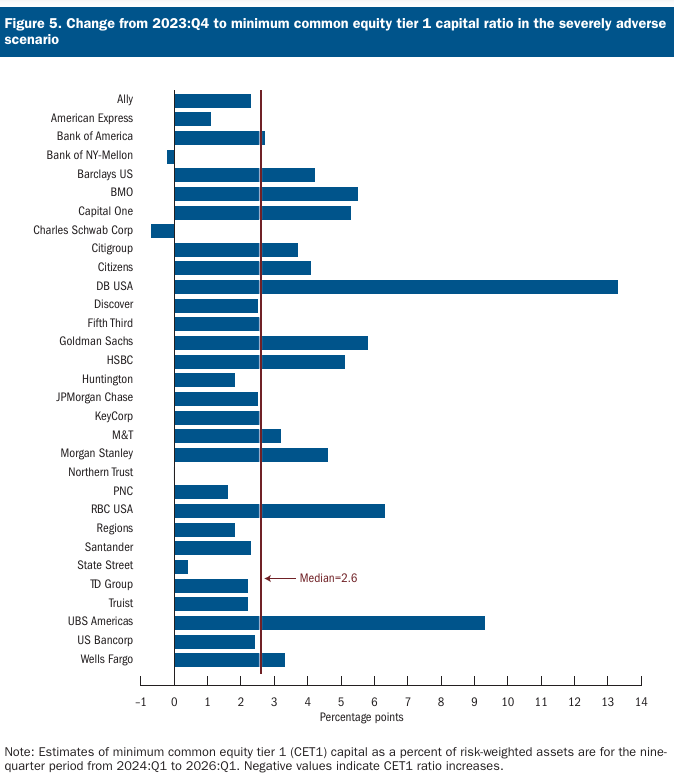

All 31 banks tested remained above their minimum common equity tier 1 (CET1) capital requirements during the hypothetical recession, after absorbing total projected hypothetical losses of nearly $685 billion. Under stress, the aggregate CET1 capital ratio—which provides a cushion against losses—is projected to decline by 2.8 percentage points, from 12.7 percent to 9.9 percent. While this is a greater decline than last year’s, it is within the range of recent stress tests.

This year’s hypothetical scenario is broadly comparable to last year’s scenario. It includes a severe global recession with a 40 percent decline in commercial real estate prices, a substantial increase in office vacancies, and a 36 percent decline in house prices. The unemployment rate rises nearly 6-1/2 percentage points to a peak of 10 percent, and economic output declines commensurately.

With the scenario relatively unchanged from last year, there are three main factors that explain the larger capital decline in this year’s test:

- Substantial increases in banks’ credit card balances combined with higher delinquency rates have resulted in greater projected credit card losses;

- Banks’ corporate credit portfolios have become riskier, partly reflected in banks’ downgrading of their own loans, resulting in higher projected corporate losses; and

- Higher expenses and lower fee income in recent years, resulting in less projected income to offset losses.

The nearly $685 billion in total projected losses includes $175 billion in credit card losses, $142 billion in losses from commercial and industrial loans, and nearly $80 billion in losses from commercial real estate. The disclosure document includes additional information about losses, including firm-specific results and figures.

In a statement, J.P. Morgan noted that the investment bank had reviewed the Federal Reserve’s 2024 stress test results and specifically the Federal Reserve’s projections for Other Comprehensive Income (OCI). “Based on the Firm’s own assessment, the benefit in OCI appears to be too large. Should the Firm’s analysis be correct, the resulting stress losses would be modestly higher than those disclosed by the Federal Reserve.”

The Fed also conducted an exploratory analysis, including two funding stresses to all banks tested and two trading book stresses to only the largest and most complex banks. The exploratory analysis is distinct from the stress test, exploring additional hypothetical risks to the broader banking system.

The two funding stresses include a rapid repricing of deposits, combined with a more severe and less severe recession. Under each element, large banks would remain above minimum capital requirements in aggregate, with capital ratio declines of 2.7 percentage points and 1.1 percentage points, respectively.

Under the two trading book stresses, which included the failure of five large hedge funds under different market conditions, the largest and most complex banks are projected to lose between $70 billion and $85 billion. The results demonstrated that these banks have material exposure to hedge funds but that they can withstand different types of trading book shocks.

Fintech comment

In emailed commentary, Joseph Cordahi, strategy director at NeoXam, said: “These results do not mean banks can afford to rest on their laurels by any stretch of the imagination. Any assertion that the Fed’s stress tests negate the need for the Basel III endgame capital requirements misses the mark.

“Central bank stress tests, ultimately, only provide a snapshot under specific conditions. They cannot account for the increasingly unpredictable nature of financial crises, which as we have seen with SVB, often unfold in ways that differ markedly from pre-defined scenarios.

“In today’s interconnected markets, there is no telling where the next pocket of unforeseen risk lies. As the stress testing bar gets higher and higher as each year passes, banks need to have an even greater handle on their portfolio transactions, trading positions, as well as pricing.

“Last year’s failures of three big banks has clearly been a big wake-up call for this year’s institutions to rethink their approach to safeguarding against future economic turmoil. Given the success rate, banks are clearly putting more of an emphasis on getting hold of precise and timely information – the lifeline in any financial meltdown.”