The Financial Stability Board (FSB) published a report about FinTech and Market Structure in the COVID-19 Pandemic. The main finding of the report is that the pandemic has accelerated the trend toward digitalization of retail financial services.

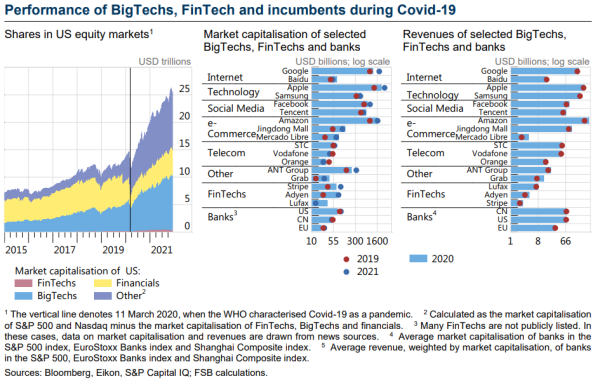

While comprehensive data on the market shares of fintechs, bigtechs and incumbent financial institutions in retail digital financial services are scarce, proxies suggest that bigtechs and larger fintechs have further expanded their footprint in financial services.

The report notes that bigtech and fintech firms’ expansion into financial services can bring benefits such as improved cost efficiencies and wider financial inclusion for previously underserved groups. However, it also cautions over the potential for market dominance. In some markets, concentration measures are high, but there is no evidence yet of a generalized increase.

There could be negative financial stability implications from dependence on a limited number of bigtech and fintech providers in some markets, the complexity and opacity of their partnership activities, and potential incentives for risk taking by incumbent financial institutions to preserve profitability. There could also be consumer protection risks from greater dependency on technology and data protection issues. In addition, the limited number of cloud service providers could magnify the impact of any operational vulnerability.

The growth of bigtechs in particular underscores the need to address data gaps that currently hamper the assessment of those firms’ financial risks and systemic importance. Such data gaps make it difficult for authorities to decide whether and how to regulate bigtechs.

The report outlines the types of actions authorities have taken during the pandemic that may impact market structure and the role of different firms in providing digital financial services. These actions relate to financial stability, competition, data privacy and governance issues. The report also stresses the importance of cooperation between financial authorities and, where relevant, with competition and data protection authorities.