Global Digital Finance (GDF) and Ownera released a report on the “Case for collateral mobility in Europe and UK using money market funds (MMFs). The report examines the legal certainty of collateral eligibility and the mobility of tokenized MMFs in Luxembourg, Ireland, and the UK. Ireland and Luxembourg host more than 80% of the MMFs and cross-border funds in Europe and English law governs the Credit Support Annex (CSA).

The report concludes:

- There is relative legal certainty of tokenized MMFs located in Luxembourg in a digitally native or registered form due to the availability of statutory frameworks to govern such transactions

- Longstanding historical legal interaction between Luxembourg and the UK in respect of financial and investment contractual arrangements, including CSAs, also makes this an attractive place to establish a TMMF where the tokens will be posted as collateral under a CSA governed by English law

- There is not yet express statutory or judicial authority in Ireland specifically addressing tokenized shares or TMMFs. Legal certainty in respect of ownership and treatment of tokenized shares under Irish law therefore requires an analogy to traditional shares and electronic contracts, rather than being directly established

- It is reasonable to conclude that Irish courts would treat digitally native TMMF shares in a manner consistent with traditional shares. This alignment reinforces the view that TMMF shares can be accommodated within existing property law principles in Ireland, supporting their recognition and enforceability under Irish legal standards

- Where an MMF is tokenized using a digitally native TMMF and is located in the UK, there is a low degree of legal uncertainty concerning the legal treatment of ownership and a similarly low level of uncertainty concerning the replication of rights for market participants between the traditional MMF and a digitally native TMMF

- It is anticipated that further certainty will be available in the UK if the Property (Digital Assets etc.) Bill is enacted and common law precedent is developed as to the implications of the “third category” of property.

Over 70 firms participated in the working group including S&P, Federated Hermes, R3, JP Morgan, Ownera, Finastra, Lloyds Banking Group, Hogan Lovells, LSEG, Archax, Blackrock, State Street, ISDA, EY, Commerzbank, Fireblocks, Northern Trust, Apex Group, Franklin Templeton, and Goldman Sachs.

“The combination of research and assessment findings and the practical sandbox execution of production use cases made this working group a very special and successful achievement,” said Armin Peter, GDF executive in Residence who is also a former global head of Debt Syndicate EMEA at UBS and a former Global Financial Markets Association (GFMA) Board member, in a statement.

Sharon Lewis, lead partner for Future of Finance and co-chair of Digital Asset & Blockchain Practice at Hogan Lovells, said in a statement: “There is relative legal certainty of TMMFs located in Luxembourg in a digitally native or registered form, where both Ireland and the UK have a low degree of uncertainty as the courts are likely to treat digitally native TMMF shares in a manner consistent with traditional shares.”

Collateral mobility sandbox

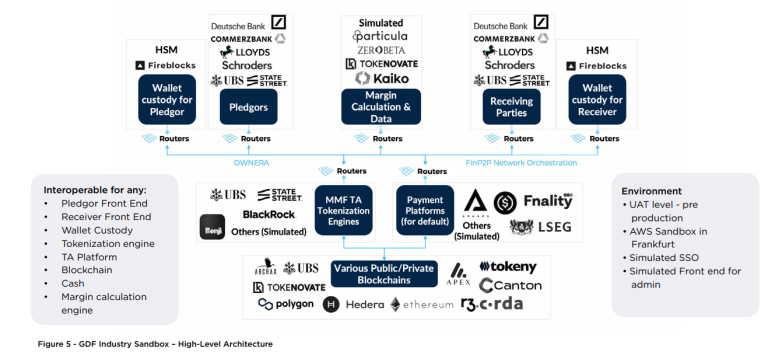

As part of a working group, 30 of the firms participated in the GDF Industry Sandbox, powered by Ownera, the firm which operates the FinP2P routers that implement the open FinP2P standard to “prove” the production use case for collateral mobility in TMMFs.

With no fundamental barriers identified across legal, operational and regulatory dimensions, the sandbox demonstrated that TMMFs can transition from theoretical use cases to a production-ready collateral instrument across six simulations:

- Simple Bilateral Transfer – Manual Margining of TMMFs

- Integrated Margin Calls – Automated Posting via Third-Party Systems

- Depeg Event and Substitution – Dynamic Portfolio Management

- Default Scenario – Enforcement and Recovery in Insolvency

- Funding of TMMF in Triparty

- From SWIFT to Collateral Settlement in Seconds.

“Hosting the GDF Industry Sandbox was a monumental collaborative effort, bringing together some of the best-in-class market participants, custodians, and technology providers from across the industry. The results highlight what’s truly possible when we apply FinP2P and its DLT interoperability layer to collateral mobility and optimization,” said Natasha Benson, COO and CFO of Ownera, in a statement.

Amarjit Singh, UK Digital Assets Leader, EY said: “The over 30 TradFi and Fintech firms participating in the sandbox have demonstrated that collateral mobility for TMMFs has arrived. This is an exciting next step in the continued uplift to the future market’s infrastructure, leveraging digital assets to bring real-world benefit to investors and financial institutions around the globe.”

Lawrence Wintermeyer, GDF Member Board Chair added: “Testing the legal certainty of digital assets and demonstrating real production use cases is a time that has arrived for the global securities industry. This outstanding working group demonstrated it could engage the world’s best TradFi and digital Financial Market Infrastructure (dMFI) firms to collaborate and demonstrate to the whole of the industry and its regulators that digital finance has truly arrived. I look forward to the US working group kicking off in January 2026.”

Participant quotes cited in report:

“Tokenization removes key operational constraints … It offers a real-time, on-chain representation of assets, making the funds verifiable, trackable, and easier to mobilize,” said Anna Matson, head of Digital Assets & Innovation for EMEA at Northern Trust.

“Rather than selling shares of a money market fund and then sending the cash as collateral to meet a margin call, a financial institution can transfer ownership of tokens representing shares of the money market fund. That reduces the time for settlement and increases the speed,” said Sandeep Sasikumar, director for Derivative Operations, Clearing & Collateral Management at Blackrock.

“This groundbreaking initiative proves that digital assets can be used in regulated financial markets under existing legal frameworks here in the UK. It’s a major step forward in demonstrating how tokenization can enhance collateral efficiency, reduce friction, and unlock new trading opportunities,” said Peter Left, head of Digital Finance at Lloyds Banking Group.

“The GDF project proves out the benefits of DLT in enabling use of MMFs in collateral markets. We hope this will be a catalyst for the emergence of more tokenized MMFs, as well as the review of regulation and market participants’ collateral management frameworks to allow for greater use of MMFs,” said Reyer Kooy global head of Digital Operations at Apex Group and former chair of the Institutional Money Market Funds Association.

“We face many challenges in Europe with our fragmented settlement infrastructure to make T+1 happen. Solutions like this demonstrate that we could solve the need for cash on-ledger and help overcome some of these barriers across 22 CSDs and our currently prohibitively high intra-day liquidity demands. These experiments show that TMMFs deliver a highly liquid alternative that can be used as collateral for margin payments. Thus combining the interest payable benefits from MMFs with the ability to be used in lieu of cash,” said Andreas Biewald managing director and senior advisor for Cash and Collateral in the Treasury Department at Commerzbank.

Kim Hochfeld, global head of Cash and Digital at State Street Investment Management, said: “The global financial crisis reforms established margin and collateral requirements to reduce counterparty risk. Yet, in turn, these gave rise to surges in liquidity demands during periods of heightened market stress, as seen, for example, during the 2022 LDI crisis.

“As pension funds scrambled to meet margin requirements against their gilt exposures at that time, they were forced to redeem holdings in MMFs in order to source cash, causing money fund managers to be forced sellers into a stressed market, depressing gilt prices even further and contributing to a negative spiral. TMMFs allow for more efficient collateral management allowing capital to be freed up, reserve requirements reduced and existing inventories used more effectively. This is an all round win-win for collateral managers, money managers, investors and regulators.

“By enabling programmable ownership transfer on distributed ledgers, TMMFs would have allowed the money fund units to be posted to the collateral receiver quickly and efficiently and most importantly, would have avoided the need for redemption into cash and the associated frictions and stress that would thus be introduced into the market.”