The year 2021 ended with a huge wave of activity both in volume and value across the enterprise softwaare M&A market, which is currently on a bull run. Strong sector trends continue to underpin the adoption of software across the board, driving demand.

877 enterprise software vendors changed owners in the second half of 2021. Valuations went up and larger deals drove the disclosed value to $114 billion, supported by 21 M&A transactions worth $1 billion or more.

A recent report from Hampleton Partners details analysis of specific acquisitions, deal count, M&A value, revenue- and EBITDA-based valuations, trends, largest deals and top acquirers.

Private equity firm Thomas Bravo was one of the top acquirers, with 17 acquisitions in 30 months, which included payment processing and EDI software firm Bottomline Technologies and customer experience management SaaS Medallia among them. The largest disclosed deal was Oracle’s acquisition of Cerner at $28.3 billion.

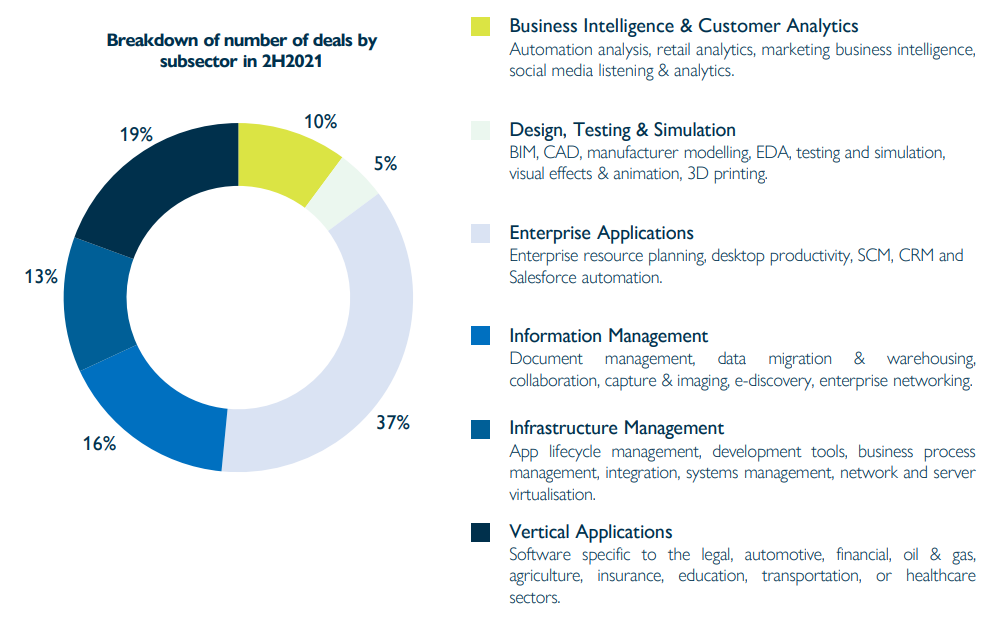

The Business Intelligence & Customer Analytics subsector has seen strong volume in the past two years. In the second half of 2021, the number of deals in the space remained stable with 89 deals closed. Valuation multiples in the space have also maintained a strong level: the trailing 30-month median revenue multiple. stood at 4.5x with 50% of transactions showing a sales multiple between 2.7x and 7.4x. Meanwhile, the trailing 30-month median EBITDA multiple came in at 10.8x, with 50% of all deals showing an EBITDA multiple between 9.6x and 16.4x.

“2022 has begun on a similarly bullish track. Financial buyers are armed with large amounts of dry powder and account for almost half of all Enterprise Software M&A,” wrote Hampleton Partners’ principal partner Miro Parizek in the report.