Can hedge funds get a break? It looks like they are not getting much love from LCR or NSFR.

Earlier this month in a SFM post “The Net Stable Funding Ratio (NSFR) and repo market liquidity: A Basel accident or an effort at extreme risk mitigation?” we noted:

“…The January consultative document proposes RSF weightings for securities financing trades (SFTs). Among these is a 50% factor for all loans with a maturity of less than 12 months to non-bank counterparties; including reverse repos. This would imply that all reverse repos with non-banks regardless of their maturity would require stable funding against 50% of their value…”

So if a hedge fund financing pretty much anything for less than a year, 50% of the deal would need to be term funded…and that long term funding cost would be folded back into the pricing. That is going to be very expensive. It also creates its own risk issues. A repo desk could now be overfunded relative to their short-dated client trades, creating a kind of negative convexity that comes when asset prices and interest rates fall at the same time repo books in general shrink (gee, where have we seen that before?). We touched upon this last November is a post “We have some more thoughts on Fed Governor Tarullo’s speech.”

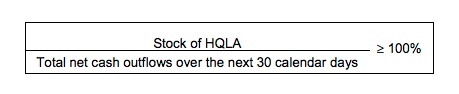

But there is more. We have heard from hedge fund managers that banks don’t want to take their short dated cash deposits. One fund COO we spoke to had trouble finding a bank that would take a couple hundred million dollars in a deposit. LCR rules say it is, in effect, hot money and hurts LCR by inclusion into the denominator of the calculation (“Total net cash outflow over the next 30 calendar days”).

From the BCBS publication “Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring tools” (January, 2013), Paragraph 109 (Unsecured wholesale funding provided by other legal entity customers: 100%):

“…109. This category consists of all deposits and other funding from other institutions (including banks, securities firms, insurance companies, etc.), fiduciaries, beneficiaries, conduits and special purpose vehicles, affiliated entities of the bank and other entities that are not specifically held for operational purposes (as defined above) and not included in the prior three categories. The run-off factor for these funds is 100%…”

There is a small loophole accorded to deposits held in connection to operational services for prime brokerage and custody related services. But this relief does not apply to “non-regulated funds” including hedge or private equity funds. It should not be surprising that hedge funds will typically want to retain as much liquidity as they can and not lock up cash in term deposits. That’s a good thing.

This issue is part of the many regulatory developments that will impact hedge funds and their relationships with their prime brokers. A good piece to read for an overview is “Leveraging the Leverage Ratio, Basel III, Leverage and the Hedge Fund-Prime Broker Relationship through 2014 and Beyond” from J.P. Morgan.