CCPs for the buy-side in securities finance, long thought of as an elusive unicorn, are now coming to fruition in what may be the most important change to the industry in the modern era. The balance sheet benefits to the sell-side of lower RWA are well-known, but equally important is how the buy-side may come to define itself in securities finance once CCPs are more widely used. A guest post from Pirum.

CCPs in securities lending has been a topic of serious discussion for the last decade, often in fits and starts. The benefits of CCPs in capital usage and netting down exposures has attracted the sell-side, which has every reason to be interested. A 2% risk-weight compared to up to 100% RWA in a bilateral transaction can bring immediate benefits, especially in a market where balance sheet constraints have been one cause of reduced volumes and muted revenues. If a CCP can unlock utilization due to lower costs, that would be a positive outcome for all parties.

The buy-side has not yet been as excited however, largely because historically there hasn’t been enough in the model for them and their agent lenders to truly benefit. That said, buy-side firms recognize that balance sheet constraints have led to lower revenues, and that change may be necessary for sustaining a robust market, especially in the face of new entrants looking for their share of revenues. Lending participants are increasingly concerned about how borrowers view their attractiveness and are looking for ways to increase their market share of a decreasing revenue pool: whether that’s in flexibility of acceptable collateral, term or participation in central clearing. A new push by agent lenders to engage in both Europe and the US means that their clients may soon take another look at the CCP model.

For buy-side firms lending with their own desks, CCP participation could fundamentally change how their businesses work. A central and accepted point of credit intermediation in the form of the CCP, coupled with an electronic market that provides access to automated pricing delivery in an RFQ or limit order book format, would make securities lending look a lot more like equity execution than it does today. That could encourage self-lending, including diverse types of partnerships with agent lenders, and potentially generate more industry participation overall.

Buy-side benefits on a CCP start with the sell-side

Given the positive experience of CCPs in other capital markets businesses, global regulators have continued to apply pressure through a carrot and stick approach to encourage the use of CCPs in securities finance. The market has agreed that the model is effective, with some theorized benefits now playing out in practice. As far back as 2013, Eurex Clearing found a potential cost saving of up to 80% for users on their Lending CCP compared to a bilateral transaction, all due to RWA and CVA impacts. This was the intention of regulators when applying a 2% risk weighting for qualified CCPs. It should of course be noted, that clearing can also result in some increased costs, with wider margin requirements and default fund contribution.

Netting benefits have proven more elusive but may grow over time, especially as CCPs are able to combine their margin pools across products. Eurex Clearing’s Prisma model and the OCC’s stock loan hedge program support parts of cross-margining already, and regulatory influence suggests that cross-netting opportunities will continue to expand. As a related matter, the transparency of the CCP counterparty obviates an immediate problem with Agent Lender Disclosure: knowing the counterparty for RWA purposes at the time of trade.

Looking forward, CCPs will bring a large new benefit by not being captive to Single Counterparty Credit Limits, (SCCL) which mandate a 15% maximum of Tier 1 capital in credit exposure between GSIBs. The US version of these rules will go live in January 2020 but CCPs are exempt. This is expected to drive business to US CCPs for a wide range of products, including securities finance. While critics may argue that this only increases the worry of CCPs as Too Big to Fail, SCCL also means that CCPs may be critically required to continue some business activities.

Functional and projected CCP models

Europe has been at the forefront in the introduction of CCPs in securities finance, after a few non-starting enterprises. Eurex’s Lending CCP has over the past few years gained traction and acceptability as well as addressed the need to accept bilateral and cross border transactions; this had been the downfall of prior attempts by other firms. Eurex offers a “Specific Lender License” for Lending CCP participation that enables buy-side firms to lend without the typical requirements of paying into the default fund, paying margin or needing to clear through a General Clearing Member. Agent lenders can oversee the activity and collateral is managed in a pledge model with a tri-party agent.

PGGM, the Dutch pension fund investment manager, became the first beneficial owner to join Eurex’s Lending CCP in June 2018, and BNY Mellon became the first agent lender to facilitate a trade on the Lending CCP in June 2019. PGGM’s Roelof van der Struik cited “cost and operational efficiencies” in its decision to join. BNY Mellon’s James Slater said that while the CCP offered immediate benefits for regulatory reporting and counterparty capital usage, the future points to other buy-side benefits: “Over time, the benefits of central clearing from a capital perspective should manifest as a combination of some uplift in price, increased distribution, or both for lending clients.” These firms see the CCP as a natural way forward for the markets.

The advance of major CCPs into sponsored repo clearing for the buy-side has seen substantial interest. DTCC reported $230 billion in average daily balance at the end of 2018 and $376 billion at the end of Q2 2019. Their model, incorporating both cash providers and collateral providers trading on a principal basis with sponsoring banks, has drawn in money market funds and hedge funds alike. DTCC has proven the business case that a CCP serving the buy-side while lowering balance sheet costs for their respective dealers will draw volumes.

DTCC is now building on the success of its sponsored repo platform to migrate this framework to equities. The equities model, expected to launch in 2020, will contain some new features specific to the securities finance business, including allowing agent lenders that are not broker-dealers to sign up directly, and allowing business to be introduced instead of conducted as principal then novated. For both agents and prime brokers, this means an introduced transaction in which the only exposure is to the CCP, not both the client and the CCP. The more that the value chain remains undisturbed, especially for agent lenders, the more comfortable they will be asking their clients to participate.

These CCP models are still works in progress and may see changes depending on user needs. However, they are live and represent years of working with the industry to align requirements onto the CCP model.

Buy-side business model change

Not since the Global Financial Crisis has the buy-side shown so much interest in securities lending. In the US, large lenders are returning to the market and some firms that have never lent are signing up. Securities lending is seen as a lower risk product than ever, even though the fundamentals remain the same, and new lenders are happy to gain a slice of the revenue stream at the expense of their peers. In Europe, regulatory and revenue challenges have meant that some firms are looking at starting securities lending while others are shutting down; it is a time of complex market evolution.

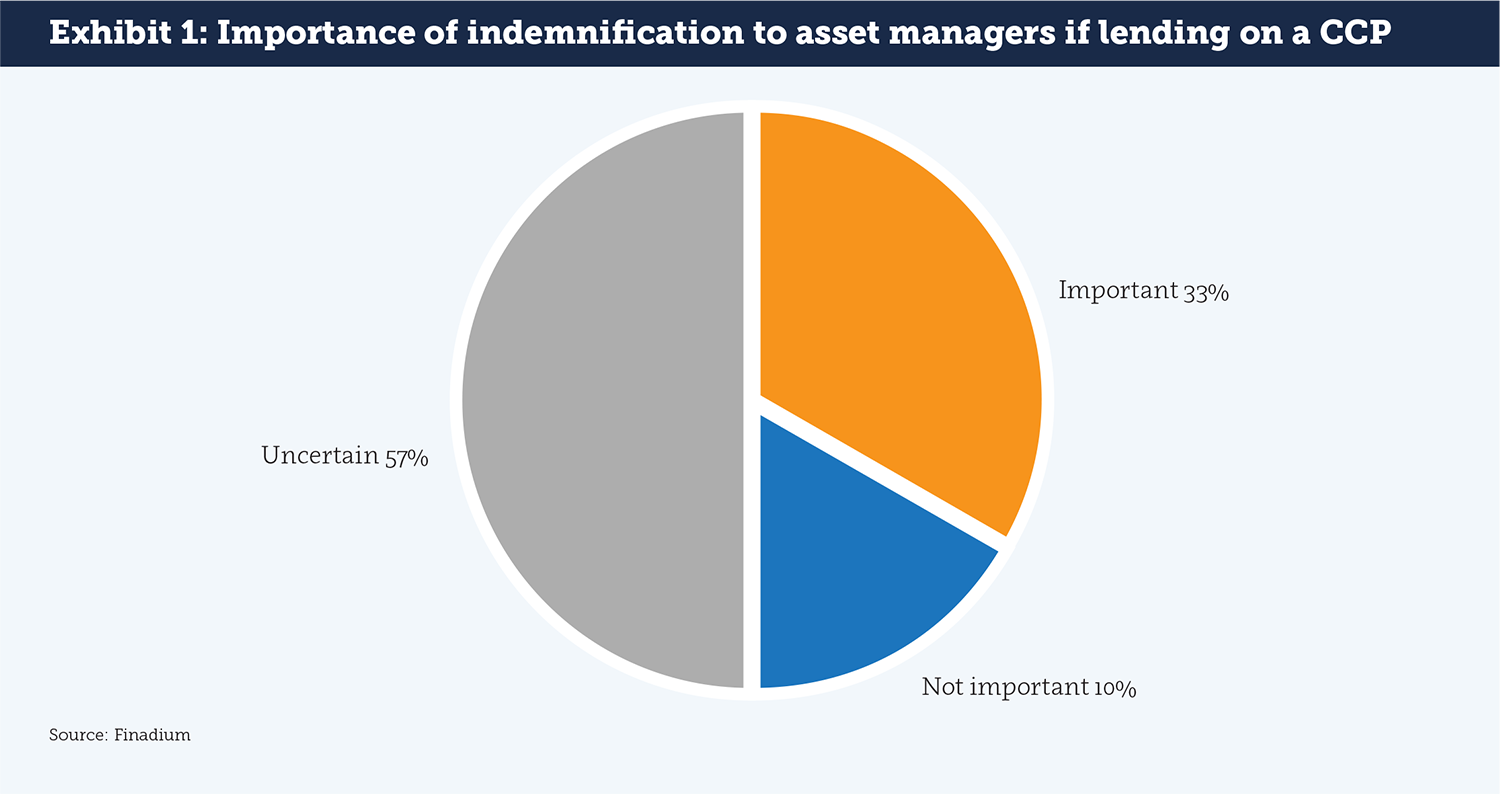

A securities lending CCP is still a new idea for most beneficial owners, but some dynamics are already coming into focus. A critical benefit to the CCP model for the buy-side is maintaining the existing relationship with an agent lender. This may matter even if a firm is lending internally, as an external agent may still provide important counterparty default indemnification and operational settlement services. Indeed, a demand for indemnification may be the most important reason to stay with an agent even if transacting on a CCP: a forthcoming Finadium survey of large asset managers in securities lending found that 33% of firms will still want indemnification even when lending on a CCP (see Exhibit 1). Nearly twice as many, or 57% of respondents, said that they did not know enough about CCPs in this space to comment on its impact. Only 10% said that they were ready to use a CCP without indemnification.

Fidelity Investments and Allianz Global Investors are the two best known firms that have started to lend their own securities in-house over the last two years, joining Vanguard, Aviva and a few other large asset managers and insurance companies. These firms are seeking to take advantage of not just revenues but also the market data and intelligence that securities finance can deliver. A move to self-lending also means that these organizations are independent thinkers; if a CCP is going to work, they will be involved early and will be hoped-for lead participants.

Not all firms can grow with a CCP however. In January 2018, Robeco, one of the more trail-blazing European institutional securities lenders, decided to outsource its securities lending and asset servicing products to J.P. Morgan. This stand-alone business had been in operation since the 1980s and established a global presence through desks in North America and APAC. Once viewed as a model of institutional self-lending, Robeco made the decision that regulatory complexity and changing demand no longer justified an independent desk. At the time, Robeco noted that “given industry developments and Robeco’s global ambitions, new and ongoing investments would have to be made to keep its operations activities cutting edge.” This suggests that while CCPs can help on the margins, they cannot solve fundamental market problems.

What will drive mass adoption?

Institutional lenders can be slow to embrace change; their internal systems, approval processes and budgets can limit the speed at which they can forge ahead, despite theoretical buy in. As a result, any uptake of new ways of doing business will be based upon ease of access and lack of expense. Buy-side firms will also need a certain amount of reshaping of the strict guidelines that have been in place in the classical view, and to be sold on the solidity of the CCP credit and risk process.

Apart from the well-documented alleviating capital impact for the sell-side, which should produce higher lending volumes, there are other reasons why all buy-side firms benefit from an expanded use of CCPs, including:

- Access to new supply and demand

- Real time reporting and settlement

- Greater choice of settlement methodologies to provide redundancy

- Opportunity to adopt an alternative risk analysis of counterparties

- Better corporate governance by conforming to global regulatory influence

- Better positioning for future regulatory changes

- Continued use of existing infrastructure

- Growing homogeneity of operational settlement across all transactional types leading to cost savings

- Cross margining capabilities

Connectivity and straight-through processing

One of the biggest changes that has been made in the last year has been the introduction of clear ways and means of accessing a functioning CCP solution. It is now nearly universally agreed that CCPs are a good conceptual idea. The next issue has been accessibility.

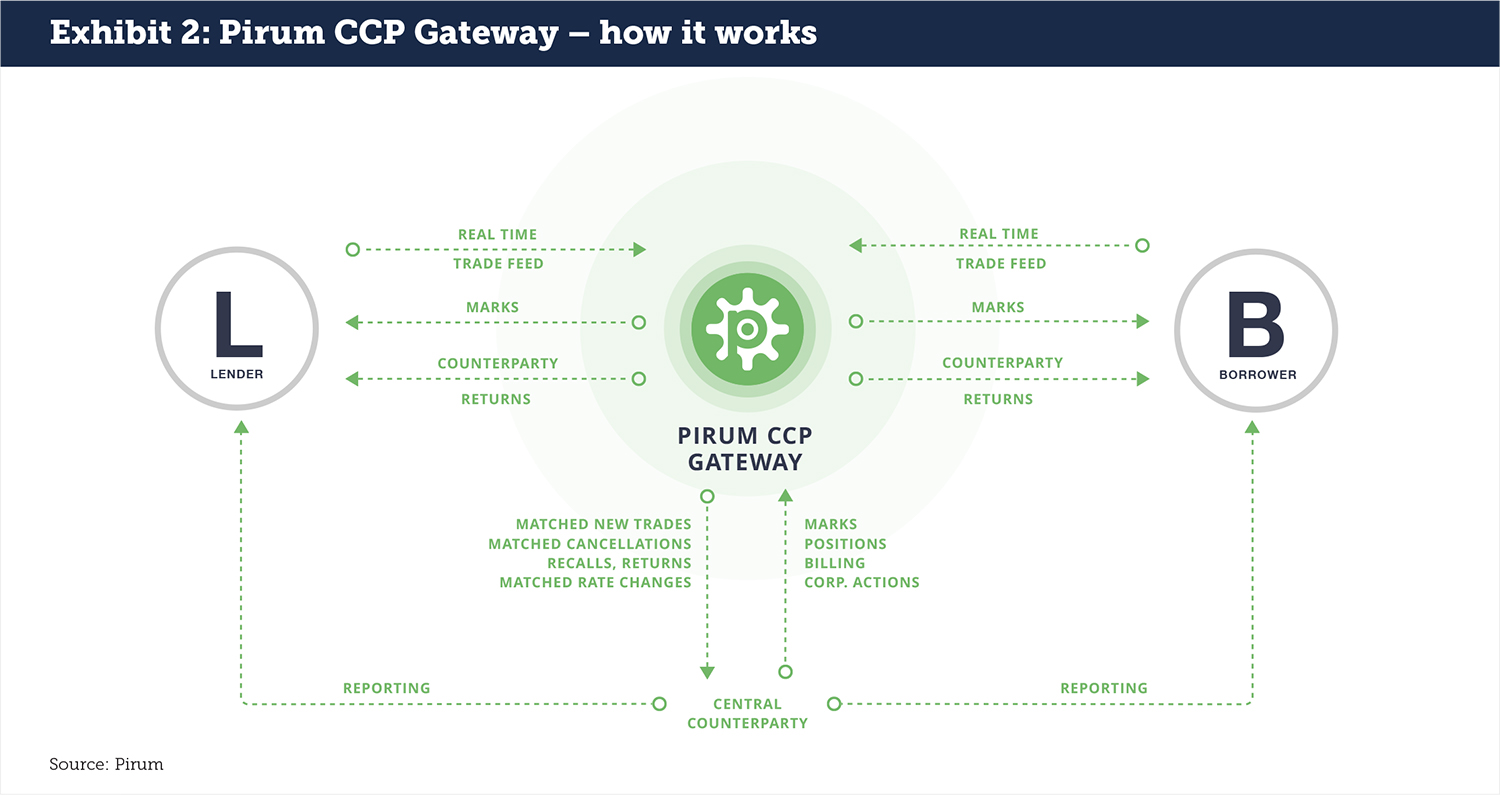

Pirum’s CCP Gateway service creates the ability to morph a bilaterally agreed loan and borrow into a CCP cleared transaction as well as catering for post-trade, billing, reconciliation and settlement operational requirements (see Exhibit 2). It allows the buy-side, across lending and borrowing firms, to utilize a CCP as well as bilateral transactions in the same technology. The Gateway is not limited to securities finance alone; it can also be used for repo and collateral management, which allows for a holistic overview of secured financing activity.

A priority of the Pirum CCP Gateway is facilitating existing relationships, whether using an agent lender, prime broker or self-lending. Transactions are matched real time and then “handed-off” to Pirum reconciliation, marks, returns, corporate actions, billing and cancellation services. This continues Pirum’s strategy of steady augmentation to the product suite and functionality.

Building towards a new future state

CCPs are both a reaction to and catalyst for change. The projected increase in their use is a result of advances in technology, desire for revenue, and greater transparency. They may also drive more change in risk control and analysis (alternative credit scoring), more efficient use of margins and collateral (one pot margining), and greater cross-border capabilities and product convergence (repo and stock loan). The more that CCPs are accessible for every value chain stakeholder, the more liquid the market becomes.

While the market has already been experimenting with alternatives to dealer credit intermediation in securities finance, including peer to peer and direct lending, CCPs represent the biggest opportunity yet for a re-alignment of balance sheet and utilization. Lenders, borrowers and intermediaries are benefitted in this task by technology and automation that revolve around a set of standard protocols and established vendors.

Rajen Sheth is CEO of Pirum System. Raj joined Pirum in 2003 and has been in the role of CEO since 2014. He started his career in technology as a software programmer and progressed to running IT teams within investment banks. Prior to working at Pirum, Raj held IT program management positions at UBS supporting both Equities and OTC products; his last role was head of cash equity post-trade strategic IT. Before this, Raj was head of Prime Broker IT at Lehman Brothers delivering front office and client technology solutions.

Rajen Sheth is CEO of Pirum System. Raj joined Pirum in 2003 and has been in the role of CEO since 2014. He started his career in technology as a software programmer and progressed to running IT teams within investment banks. Prior to working at Pirum, Raj held IT program management positions at UBS supporting both Equities and OTC products; his last role was head of cash equity post-trade strategic IT. Before this, Raj was head of Prime Broker IT at Lehman Brothers delivering front office and client technology solutions.