A fascinating article appeared in the NY Fed’s March 2014 (Volume 20, Number 2) Economic Policy Review. “Matching Collateral Supply and Financing Demands in Dealer Banks” by Adam Kirk, James McAndrews, Parinitha Sastry, and Phillip Weed. It touched on many interesting topics. We will look at their take on collateral efficiency and focus on what they say about repo netting. A summary of the article also appeared in the April 1st Liberty Street Economics blog.

The authors addressed collateral by dividing it up into three categories:

- matched book repo

- internalizing of trading activities

- derivatives collateral.

Matched book repo is certainly familiar to the readers of this blog – it is the traditional repo book activity. The authors did note that the term “matched” is something of a misnomer and we’d have to agree.

“…However, a matched book does not always involve executing offsetting repurchase and reverse repurchase agreements that are “perfectly matched” in terms of the final maturity date or the credit quality of the involved counterparties. That is, dealer banks engage in maturity and credit transformation… In an extreme event, the dealer is exposed to “rollover risk,” in which it could prove difficult for the dealer to roll over its borrowings, while still being required to fund the lending on longer-term reverse repos…”

Internalizing of trading activities is primarily taking place in prime brokers, where one client may be short and another long the same security – allowing the PB to cross the trades internally.

“…Internalization allows the dealer to generate potential income from finding and matching, among its own customers, natural buyers and sellers of the same security. Importantly, internalization also presents regulatory advantages from a capital and leverage perspective; eliminating the need to engage in external repo and securities borrowing transactions minimizes the size of the balance sheet and enables the dealer bank to increase other client activity…”

Derivatives collateral is what it sounds like – managing the collateral flows associated with initial and variation margin on derivatives trading. The authors wrote:

“…Cash tends to be favored in this context because it is operationally easier to exchange and attains a greater degree of balance-sheet efficiency though the cash collateral netting provisions granted under U.S. GAAP and IFRS…”

Each of these collateral-driven activities has their (now familiar) risks.

“…The interdependence of the financing for the borrowing of one customer and the collateral posted by another customer makes the sources of funding for dealer banks vulnerable in ways that are different from those of standard banks. Consider that in a standard bank, when a borrower repays a loan, the bank can often redeploy the repaid funds as a loan to another borrower or as payment to a deposit holder. In contrast, when a borrower repays the dealer bank, the borrower also reclaims the collateral it posted to the bank. The interdependence of the financing for the borrowing of one customer and the collateral posted by another customer makes the sources of funding for dealer banks vulnerable in ways that are different from those of standard banks…”

The authors discuss two types efficiency:

- Collateral efficiency: the ability to rehypothecate collateral received from their clients. This is correlated with the size of the dealer – the bigger the dealer, the more efficient.

- Collateral financing efficiencies: the use of netting “to engage in a larger amount of collateralized lending than is reported on their balance sheets. A dealer bank’s collateralized financing efficiency is related to the amount of netting allowed by U.S. and international accounting standards; the accounting treatment of brokerage activities, such as shorts; the differential between the cost of internal sources of funding and external ones; and the fees/income earned on lending activities…”

Netting has been a hot topic in repo. The use of netting means that reported balance sheets are smaller than the actual book of business – and this opacity makes regulators nervous. The repo business dodged a bullet recently when the Basel Committee affirmed the use of netting.

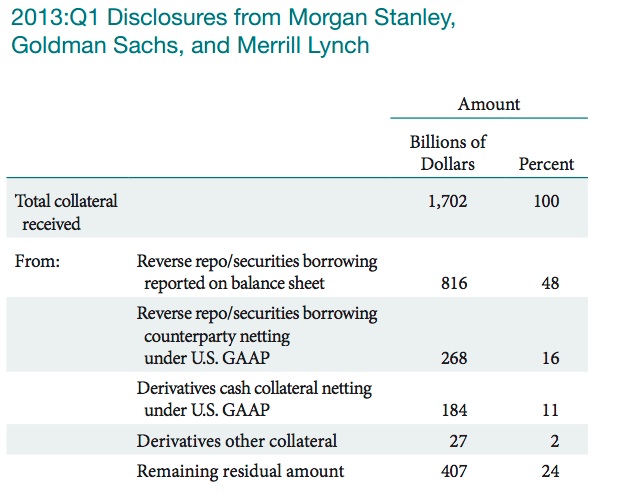

Just how significant are the benefits gained from netting? The study did some interesting digging using financial reports from Goldman Sachs, Morgan Stanley, and Merrill Lynch. The following chart looks at the amount of counterparty netting across several businesses. Focusing on just two numbers: “Reverse repo/securities borrowing reported on balance sheet” and “Reverse repo/securities borrowing counterparty netting under U.S. GAAP” shows that roughly 25% of repo books disappear in the netting exercise.

From the report:

“…Accounting netting…does not reflect true economic netting of risk exposures. This line of reasoning leads us to suggest that the recent consultative document of the Basel Committee on Bank Supervision (2013) that outlines a revision to the Basel III leverage ratio framework which, when measuring securities financing transactions excludes any recognition of accounting netting, may be warranted as a measurement approach…”

While the authors may not have realized that repo got a Basel pass on netting, it still is instructive to understand the argument against netting and remember that prohibitions against netting could pop up in other ways.

They suggested repo-specific capital and liquidity charges as a way to mitigate netting risk.

“…However, some capital and liquidity charge (as, for example, is the case with the Liquidity Coverage Ratio) for financing transactions that are currently subject to accounting netting treatment, and are therefore off-balance-sheet, does seem warranted…”

These ideas sound a lot like the ones we’ve read about for mitigating tri-party fire sale risk. We wouldn’t bet that the netting debate is totally settled. All regulators have to do is play the “opacity” and “regulatory arbitrage” cards and it will be open season. IFRS standards allow netting, but we are told the restrictions are harsher — the bonds actually have to be the same. If that constraint is introduced under U.S. GAAP, repo netting is pretty much history. We wonder if allowing netting when the securities don’t have to be (at least) correlated doesn’t create an economic fiction?