The Basel Committee on Banking Supervision (BIS) released the results of its Basel III monitoring exercise for end-2023. It noted that Basel III capital and liquidity ratios remained stable for large internationally active banks, but there are also some warning flags about how well the world’s largest financial institutions are prepared for the next crisis in its latest report.

One of key findings shows €26 billion ($28.5bn) shortfall in Total Loss-Absorbing Capacity (TLAC) among two global systemically important banks (G-SIBs). These are the banks that regulators have determined to be “too big to fail” due to their size and influence on the global economy.

But with two major institutions falling short of the minimum, many will be left pondering just how resilient are these financial giants in reality. The shortfall points to potential cracks in the foundation. If the institutions meant to lead the charge in financial stability are struggling to meet their requirements, the risk of broader systemic failure remains real. It’s a troubling reminder that while reforms like Basel III aim to protect us from another global financial meltdown, they can only go so far if key players fail to comply.

LCR gap

The liquidity shortfall reported by three major banks is another red flag. These institutions fell below the minimum Liquidity Coverage Ratio (LCR), meaning they lack sufficient high-quality liquid assets to handle a short-term liquidity crunch. The €13.5 billion gap in liquid assets may seem like a drop in the ocean compared to the overall strength of the financial system, but liquidity crises have a nasty habit of spiraling out of control. When banks can’t meet their short-term obligations, confidence erodes, and financial markets can seize up.

This is exactly the scenario the LCR was designed to prevent, yet here we are, with several key players falling short. This raises the uncomfortable possibility that, should a sudden shock hit the system, some banks might not have the cash on hand to weather the storm.

“This report is a major wake up call for financial institutions currently reassessing their approach to liquidity management,” said Alex Knight, head of EMEA at Baton Systems, in emailed commentary. “In fast-moving global markets, banks need to lead the charge when it comes to streamlining operations, reducing costs, and ultimately maximizing the use of their assets. Only by making these operational changes can banks harbor any hope of meeting these liquidity demands without maintaining excessive buffers.”

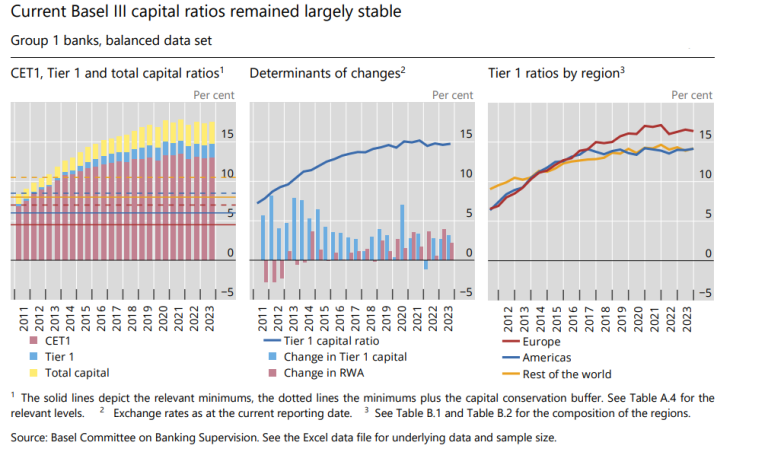

Competition realities

Perhaps one of the most telling aspects of the report is the uneven impact of Basel III across different regions. European banks are facing a 5% rise in minimum required capital, far outpacing the 0.3% increase seen in the Americas. This discrepancy could put European banks at a serious disadvantage, forcing them to raise more capital just to comply with the rules while their global competitors face far less pressure.

This regional divide could lead to broader issues of financial competitiveness. If European banks find themselves burdened with higher regulatory costs, their ability to compete on the global stage could be compromised. In the long run, this may lead to a more fragmented financial system, undermining the very goal of creating a stable, unified global banking framework.

Valerie Fontaine-Aubry, FRTB practice lead for the Americas at Murex, said in emailed commentary: “As outlined in this report, the impact of global divergences in Basel III implementation must continue to be front of mind. There is the risk that firms develop a solution that performs well in one jurisdiction but lacks the flexibility to adapt to others. This includes both the data model and performance capabilities needed to meet the demands of managing multiple jurisdictions.”

Smaller banks, classified as Group 2, are facing their own set of challenges. The output floor — a cap on how much banks can reduce their capital requirements by using internal models — will gradually increase until 2028, potentially pushing up their capital requirements by as much as 8%. While this measure is intended to ensure that all banks hold enough capital to cover risks, it could disproportionately impact smaller institutions, forcing them to raise significant capital just to stay compliant.