Regulators are focusing on the risks associated with counterparty exposure and collateral management following multiple instances of buy-side leveraged trades going awry. In every case, some of their recommendations could be met with distributed ledger technology (DLT) solutions at a reasonable cost, and with a high degree of accuracy across the industry. Could this be the catalyst for market-wide adoption of DLT in the collateral space?

Managing collateral liquidity and risk exposures can be a complex task even for experienced market participants. For firms newer to the practice, the idea of installing collateral technologies and processes can be perplexing. Secured financing and derivatives DLT solutions already exist that work on the back end, that require no proactive client connectivity, and that deliver the industry wide benefits that regulators want. DLT for collateral risk management could complement the role that industry consortia have in the past, enabling an efficient resolution to common problem sets.

DLT can deliver on intraday collateral management, which meets the regulatory standard in “faster” collateral settlement. Guido Stroemer, CEO of HQLAX, notes that “HQLAX’s core functionality is ideally suited for enabling instantaneous, precise and real-time mitigation of counterparty credit exposures, not only during normal business hours, but conceivably also on a 24/7 basis. Given the recent BCBS and the FSB consultation papers on counterparty credit risk management, we expect the banking industry to complement its attention on managing intraday liquidity as a scarce financial resource with a similar, laser-like focus on mitigating intraday Risk Weighted Assets (RWA) related to intraday counterparty credit exposures.”

While regulators will likely never state that capital markets should move to DLT as a technology choice, market participants can see that DLT offers direct solutions to recent proposals. This is no longer a conversation about DLT as a solution in search of a problem but rather the exact opposite. Regulatory calls for accurate and timely counterparty and collateral tracking across banks and non-bank institutions are solved by DLT as a starting point of the technology. Workflows for collateral and margin management in capital markets are already built out. The next step is to match the range of regulatory mandates with a look at functional outcomes.

The Basel Committee speaks on counterparty credit risk

In an April 2024 consultation paper, “Guidelines for counterparty credit risk management,” the Basel Committee on Banking Supervision (BCBS) asked regulated banks to beef up their supervision of collateralized activities in particular with non-banks. This is the long tail of the response to the collapse of Archegos Capital Management in 2021 that caused tens of billions in losses at major banks and prime brokers. Securities financing transactions (SFTs) feature prominently in the BCBS’s thinking.

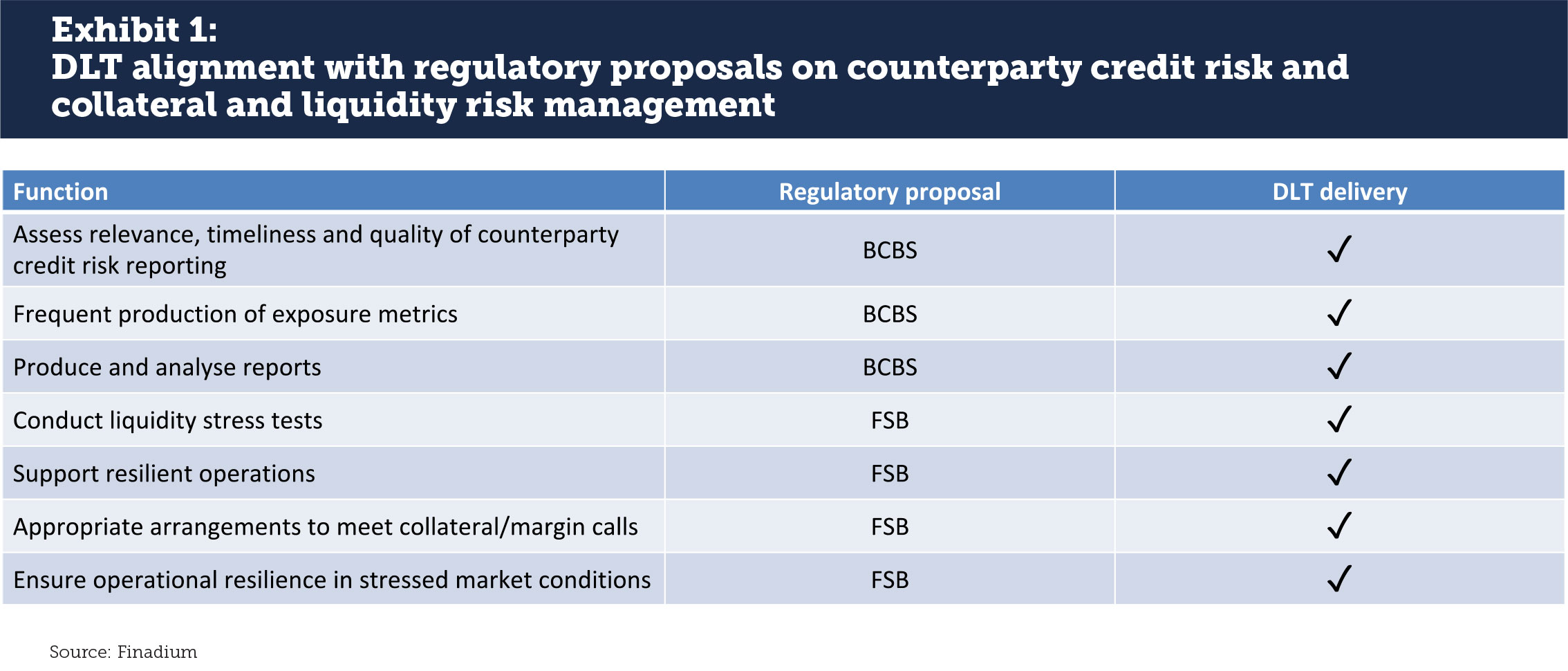

The consultation paper asks banks to create a robust Management Information System, to deliver timely reporting and to compute counterparty credit risk (CCR) metrics frequently, all functionalities that DLT delivers on day one. The paper notes:

- Banks should regularly assess the relevance, timeliness and quality of CCR reporting. This should include, but not be limited to, an assessment of input data quality, analysis of comments on potential data anomalies, assessment of the frequency of reporting and ensuring adequate socialisation of reports within key business and oversight functions.

- Exposure metrics should be produced frequently and in a timely manner and include all trades giving rise to CCR, across product types (eg bilateral, centrally cleared and exchange traded derivatives and SFTs), as well as across business lines and legal entities.

- Management reports should be comprehensive, accurate, consistent, actionable…. A bank should be able to produce and analyse reports in both normal and stressed market conditions.

The consultation paper also calls for sound practices to carry out closeouts when needed, including collateral liquidation and trade replacement, whereas the automated, frictionless, enforceable and controllable features of DLT point to a new way to answer those requests.

Market participants will once again be asked to create new reporting, systems and potentially methodologies that will deliver on a new Basel Committee mandate. The industry could take individual approaches to the quantitative and data elements or could coalence around standards similar to data delivery under the Securities Financing Transactions Regulation (SFTR). Choosing a DLT solution as an industry-wide solution may be easier than going it alone.

The Financial Stability Board on non-bank collateral and margin risk

In their own April 2024 consultation paper, the Financial Stability Board (FSB) made a call for robust liquidity risk management in collateral and margin with a focus on non-bank financial intermediation (NBFI). The paper, “Liquidity Preparedness for Margin and Collateral Calls,” has eight recommendations for how this gets accomplished, many of which are functionalities that DLT supports. These include:

- Conduct and improve the quality of liquidity stress tests

- Support resilient and effective operational processes and collateral management practices

- Establish appropriate collateral arrangements to meet margin and collateral calls

- Ensure operational resilience particularly in stressed market conditions

Similar to the BCBS, the FSB wants to ensure that an Archegos (or Long-Term Capital Management, or LDI) style buy-side collateral breakdown does not happen again. While hedge funds operate differently to corporates or long-only asset managers, the ideas of the paper are broadly applicable to any non-bank entity.

Following the FSB’s thinking, non-banks will need to start with visible and transparent data on their collateralized holdings and agree on that information with counterparties. Erica De Rosa, Solutions Architect at HQLAX, said that “HQLAX‘s connectivity to multiple market infrastructure providers and custodians, and its role as a collateral registry, mean that data across all a firm’s collateral holdings can sit in one digitized location. This makes data retrieval and analysis a fast and easy process for daily management or stress testing purposes.” Other FSB recommendations are problems that DLT solves as a default starting position. Tying HQLAX back to the FSB recommendations, HQLAX’s Digital Collateral Registry is a “resilient and effective operational process” and is an “appropriate collateral arrangement to meet margin and collateral calls.”

Delivering what the regulators want

Mapping the consultation proposals from the BCBS and FSB to services that DLT platforms can provide, it becomes clear that solutions exist to deliver on new regulatory objectives with a minimum of new industry technology development (see Exhibit 1). Challenges of operations, margin movements and data accuracy for stress testing are all solved for with a DLT offering.

Moving forward on implementation

Should regulators just take the next step and mandate DLT as the solution for counterparty risk and collateral exposure? This is unrealistic, as regulators have historically not wanted to propose any specific technology to solve for new requirements. However, each new consultation paper recommending improvements to counterparty and collateral exposure monitoring and liquidity tools is asking for deliverables where DLT is an ideal fit.

The market meanwhile is inching towards DLT in phases. HQLAX recently passed the €1 billion notional milestone in outstanding agency securities lending Delivery vs Delivery (DvD) transactions using HQLAX‘s Distributed Collateral Registry. This is not crypto but rather a set of auditable platforms that unlock the benefit of the technology while meeting institutional standards. More banks and non-banks may connect to DLT infrastructures as a way of responding to regulatory mandates while gaining the efficiencies that DLT provides.

The market may ultimately move towards DLT in response to regulatory requirements by virtue of cost, speed to market and reliability. While DLT counterparty and collateral platforms may have started as a means to solve specific problems, they can now become the solution for a broad swath of regulatory standards in counterparty and collateral exposure management. Rebecca Gong, Corporate Development & Regulatory Affairs Lead at HQLAX, said that “While we are yet to learn more about the timing for the adoption of these standards, integrating DLT and its functionalities equips a firm to follow best practices and adhere to regulatory guidelines. We are already witnessing innovative and commercially-compelling DLT-based solutions being used at scale now.”

This article was commissioned by HQLAX.