The Office of Financial Research (OFR) published a report “Repo and Securities Lending: Improving Transparency with Better Data” (April 23, 2015) written by Viktoria Baklanova. There paper makes some interesting points.

It should come as no surprise to SFM readers that no one really knows how big the securities financing markets are. Double counting on one side and missing participants on the other doesn’t help the cause. Certainly there is more reporting for securities financing than there used to be, but one segment of the market — bilateral trades – is still pretty much a mystery. The paper took a good look at what data is collected and some embedded assumptions.

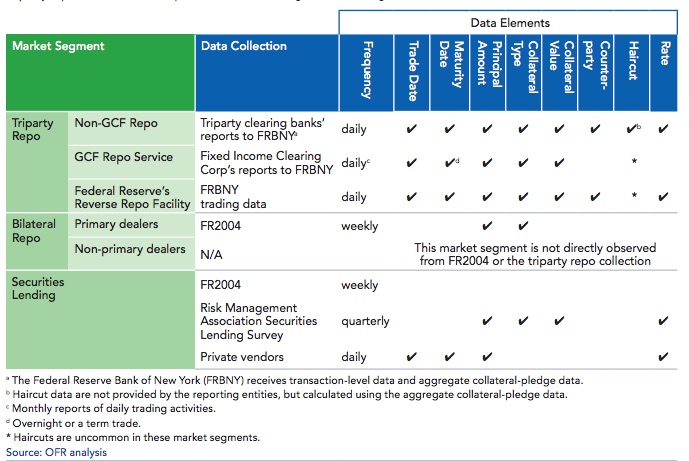

There are two places to look for securities financing data: regulatory filings and market segment. Some of the data is public, some is not.

“…the Consolidated Reports of Condition and Income for depository institutions — typically referred to as “call reports” — and Form FR Y-9C for bank holding companies require individual firms to supply quarterly data on the value of their repos and reverse repos, as well as data on the valuation of collateral in these transactions. Mutual funds, insurance companies, and mREITs report their financing activities, including those conducted in the repo market, as part of their regulatory filings. In addition, detailed (or granular) data are available to supervisors of financial firms though their regular examinations. However, examination reports are confidential and not available for market monitoring or research purposes…”

This data is not always very granular. From the report:

“…The data are usually highly aggregated and focused on quantity traded. The data do not answer questions about rates, haircuts, or counterparty exposures…”

And there is missing data from those simply not required to report.

Information on a segment basis perhaps is a little bit better. For example, tri-party data published by the Fed gives a good sense of what is going on by asset class, haircuts, and volume. Primary dealers report on their bilateral repo activity weekly on FR2004. But what about those who are not primary dealers, yet still active in repo?

“…data on repo and securities lending by smaller, stand-alone dealers — dealers not affiliated with bank holding companies (BHCs) — are not systematically collected. Although non-BHC-affiliated dealers are presumed to make up only a small share of repo activities, this presumption lacks any certainty. The market share of this type of firm has to be extrapolated from the triparty repo data, where primary dealers account for 90 percent of the total volume…”

The report had a good graphic “Sources of Data on Repo and Securities Lending by Market Segment”

What about Securities Lending?

“…Section 984(b) of the Dodd-Frank Act directed the SEC to adopt rules to increase the transparency of information available to brokers, dealers, and investors about securities lending. However, to date, the SEC has not yet issued a proposed rule…”

There are data overlaps.

“…regulatory reports greatly overstate the size of the market because each transaction is reported at least twice by different parties on their regulatory reports. For example, a money market mutual fund reports the same transaction on Form N-MFP that a dealer reports in its repo positions report and a triparty clearing bank reports in its daily submissions to the Federal Reserve…”

The report noted that the OFR has been advocating the use of Legal Entity Identifiers (LEIs) for financing trades. This would allow analysis that avoids double counting. But the data needs to be more comprehensive than, say, reporting a cash corporate bond trade. Type of collateral and counterparties, haircut, maturity and rate would be a bare minimum. Remember, regulators globally are trying to figure out if there is instability on the horizon. Knowing if the financing market is tilted in one direction or another is a good leading indicator.

Processing all that information and making sense of it is big data at its best. Regulators will never capture every trade. It will always be a statistical sample. Understanding what is missing — especially if entire segments of the market — is important in order to avoid incorrect conclusions. It reminds us of Donald Rumsfeld and unknown unknowns. We have written about this before. Take a look at “What can the OFR securities financing data collection project be used for?” (Dec. 17, 2014) and “Office of Financial Research takes a look at repo and sec lending data collection (Dec. 8, 2014).

The OFR and the Fed are working hard on collecting the data. A pilot project started in 2014 is expected to yield results by the end of 2015.

The Financial Stability Board has international coordination of securities financing data on their agenda. Collecting and analysis of data based only on where a trade was booked is a fool’s errand. Securities financing has always been geographically fluid with booking centers moving around. We hope regulators can play nicely together.

The report also revealed “…the OFR will release reference guide on U.S. repo and securities lending markets…” That will make for some interesting reading.