The impact of regulations on the securities lending industry has been frequent and profound, but the market remains vibrant. Volumes decreased in 2015 for the first time since the Global Financial Crisis although they remain near post-2008 highs. Growth in two key areas demonstrate the market’s adaptability: transactions backed by non-cash collateral have increased steadily since 2008 and direct lending is slowly growing between borrowers and lenders without an intermediary bank. With more regulations coming online in the near future, including the Financial Stability Board’s new margin rules, firms are well-placed to scrutinize available strategies in a bid to optimize returns.

Changes to the non-cash collateral markets

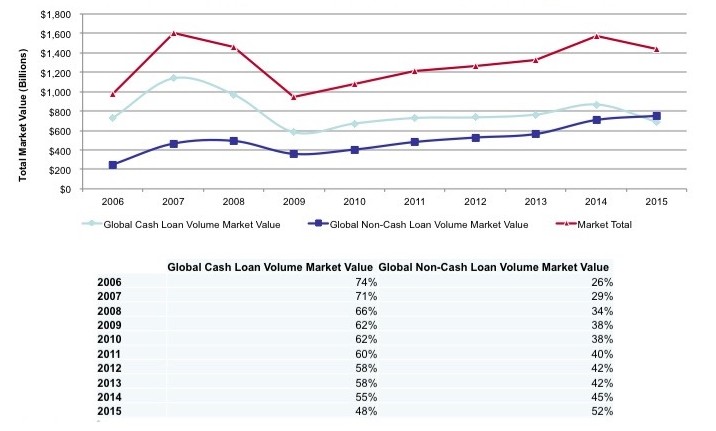

The pronounced increase in the use of non-cash collateral in the securities lending market has not been lost on any market participant. Already, the use of non-cash in securities lending has crossed 50%, according to FIS’s Astec Analytics; this is up by 26% in 2006 and 14% from 2009 just after the Global Financial Crisis (see Exhibit 1).

Exhibit 1:

Cash vs. non-cash in securities lending – global market

Source: FIS’ Astec Analytics

The primary drivers of this non-cash use have been identified as the Liquidity Coverage Ratio (LCR) and the Leverage Ratio. Multiple analyses have shown that when borrowers post non-cash collateral for a securities loan, their LCR and Leverage Ratio impacts are a fraction of what it could be when posting cash collateral. While the rationale for the rules can be argued, the fact is that cash collateral posted to an agent lender is a cash loan; non-cash collateral is not. Cash is a High Quality Liquid Asset (HQLA); equities can be HQLA Level 2B but more often are simply an excess and unused asset on the balance sheet. For bank borrowers, posting equities as collateral is an ideal optimization technique. Lenders must then choose to accept the loan terms or risk losing out revenues to competitors that have more confidence in the transaction.

Direct securities lending

The direct securities lending market offers an intriguing opportunity for lenders and borrowers alike. The basic idea is that direct removes a bank intermediary from the transaction; lenders and borrowers are directly exposed to the credit risk of the other party. This is proving to be an attractive trade for repo cash providers willing to accept high quality collateral such as government bonds or US agencies from REITs and hedge funds. It has so far proven relatively less attractive for securities lenders willing to accept cash from hedge fund borrowers.

The potential to go direct comes with a need to carefully manage incoming collateral. As recent US Treasury volatility and Bund Tantrums have shown, even the highest quality collateral can see liquidity and price fluctuations. Securities lenders and cash providers need to be certain that they hold appropriate collateral to cover their loan exposures; this is even truer when loans are made to relatively small, non-bank counterparties.

Lenders have two options for collateral management in a direct transaction. The first is that they manage collateral internally including valuations and collateral calls. This requires an understanding of collateral mechanics, as well as the operational capabilities and technology to manage the process. The second option is to outsource collateral functions to a bank or service provider; securities lending agents are well placed to take on these responsibilities. In this case, the agent lender conducts all the same functions as if the loan were made in an agency program. Instead of a fee split however, the lender would pay a service fee. There would be no counterparty default indemnification in this type of transaction, which is an important service differentiation between the agent providing a regular lending service and the agent acting as the valuation and operations provider for a direct transaction.

Agent lenders may also start hybrid service offerings that combine valuations, operation and/or counterparty default indemnification for a service fee. This could be a “best of all worlds” approach where direct lending participants pick and choose the services they want and pay on an a-la-carte basis. With collateral and valuation responsibilities turned over to the agent lender, asset holders can then select when to engage in lending and can project a profit after costs. As direct lending evolves, this selection of bespoke services may become more common across the securities lending landscape.

The new rules on margin for securities lending

An important new factor in securities lending is incoming rules on minimum margin requirements set forth by the Financial Stability Board (FSB). But the impacts may be felt more in reporting and compliance than in changes to broad market behavior.

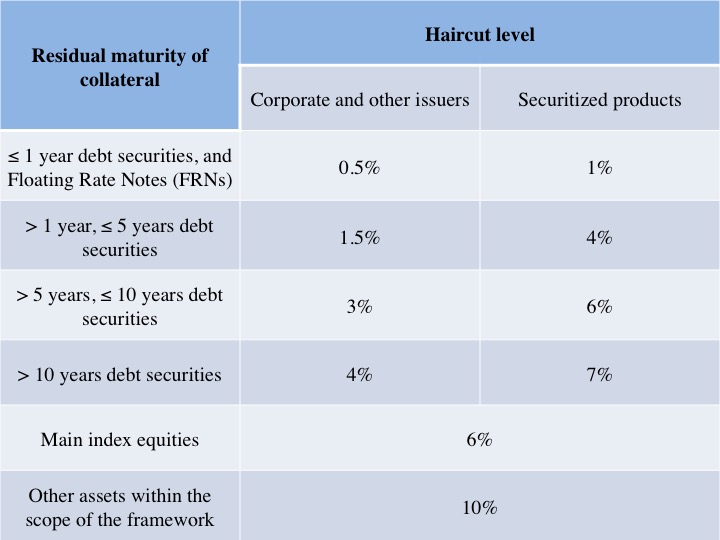

The haircuts themselves are not overly complicated but they must be factored in to any collateral management strategy. The haircuts are fairly similar to current market practice, for example 6% for equities in the FSB rules versus a typical 8% for equities in US tri-party repo (see Exhibit 2). In any case, they comprise another requirement for any sophisticated manager to consider in their overall collateral management framework.

Exhibit 2:

Numerical haircut floors for securities-against-cash transactions

Source: Financial Stability Board

The FSB states that the rules apply to “non-centrally-cleared securities financing transactions in which financing against collateral other than government securities is provided to non-banks.” There is a lot that is not covered here:

- The rules only apply to bilateral transactions collateralized by equities, corporate bonds or other relatively illiquid securities, and only where financing is provided to a non-bank.

- Transactions on a Qualifying Central Counterparty are exempt. This means that if financial actors adopt CCPs for their financing transactions, they do not need to adhere to the FSB’s haircut schedule. It is too soon to say where the market will move but the CCP exemption remains a potential carrot.

- Banks and securities firms that receive securities financing are also exempt; the argument is that the new rules could duplicate other rules currently in effect.

- Central banks are exempt, presumably due to their low risk.

Securities lending transactions collateralized by cash are exempt from the rules but only under specific conditions that may impact how cash is invested; this is one instance of a possible material impact to a small group. The FSB requires that any cash invested not create a “material maturity or liquidity mismatch” with the original loan. This means that a lender cannot take the cash associated with a securities loan of an expected one week term and invest in two year higher risk instruments. This exact strategy is a source of significant income generation for a small portion of securities lenders and may cause consternation.

There is another potential exemption to collateral upgrade trades, which are nothing more than non-cash securities lending transactions. The FSB distinguishes collateral upgrades and allows these transactions to be exempt from the new haircut rules if lenders “are unable to re-use, or provide representations that they do not and will not reuse, the securities received as collateral against the securities lent.” Since the majority of lenders do not rehypothecate or reuse non-cash collateral received in a securities lending transaction, and some are legally prevented anyhow, this should not be much of an issue. Still, the transaction must be verified as meeting the exemption.

Managing increased collateral complexity

The evolution of non-cash collateral, regulations and direct lending in the securities lending market is a natural progression of today’s markets. It is also a natural point of integration with any firm’s broader collateral management activities including categorizing their rights and responsibilities for collateral under their control. Collateral management specific to securities lending is a growing piece of this broader challenge. The emerging marketplace requires an additional level of control and reporting of collateral that can only be achieved with technology.

The critical question remains whether to outsource or invest in technology to do the job in-house. This remains a pressing issue for a large number of firms that have yet to figure out a robust collateral strategy. Direct lenders can outsource their collateral management activities to an agent but at a cost; the question is then whether there is enough volume to warrant the internal investment and whether there is enough business for an outsourced agent to invest time and energy into the relationship. In both cases, collateral management will remain a critical and technology-focused activity for the foreseeable future.

This article was commissioned by Calypso Technology. More information about Calypso is available at www.calypso.com.