Finadium’s Rates & Repo Europe conference is around the corner and we’re highlighting early insights ahead of the event. We hear from our expert panelists from LCH RepoClear and State Street about the way US mandatory clearing of US Treasury (UST) and UST repo is part of how European market structure is shaping.

While the UST and UST repo clearing rules have been delayed for a year, there is no push to reject the overall mandatory clearing process, rather the industry seeks enough time to adapt and it’s no time to rest easy, said Olivier Nin, head of Product and First Line Risk at LCH SA RepoClear in the London Stock Exchange Group’s Post Trade division.

“There is a sense of urgency that people need to be prepared, even in Europe,” he said. “Some will have to make the choice: is it better to go clear or uncleared? But then they may risk being cut off from some of the biggest liquidity pools, usually provided by a CCP, I am not sure that’s entirely clear for everyone.”

The rationale behind mandatory clearing is to ensure that government bond trading is risk managed by the CCP, which is more transparent, automated, standardized and safe. Although transacting within a CCP is subject to margining practices, which can make it more expensive, these can be viewed as a means to combat excessive leverage in the market. At the same time, clearing frees up balance sheets for banks, which, during times of stress, bolsters financial stability.

The big difference between US and Europe is market structure, with European sovereign debt and collateral fragmented across numerous jurisdictions and settlement locations. Clearing can help with some of these related issues, but it is not the only solution, he noted.

The priority move is to create suitable operational models to ensure a growing number of firms join CCPs, with an overarching goal of a “harmonized and unified market” across settlement, margining, trading, operations and risk management to avoid extra costs, otherwise you end up with a less efficient market, said Nin.

“This is what we have to do as a CCP, to make sure the market can rely on a solution that would allow all types of entities, respecting certain criteria, to have access to this big liquidity pool, even if there is no mandatory clearing,” he said. “We are trying to create this ecosystem that will allow members of a CCP to benefit from optimization.”

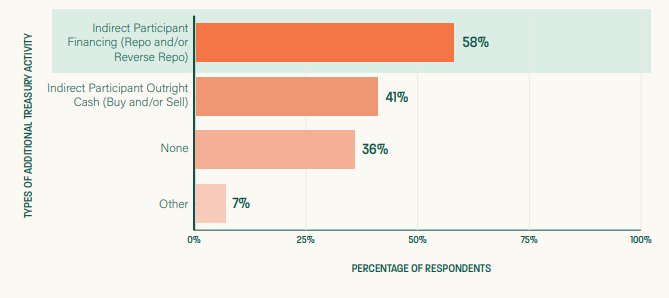

Chart: DTCC Survey participants were asked — what types of additional treasury activity will the netting member clear through FICC after implementation of the Treasury clearing requirements?

Clearing capture

The industry cannot overstate the shift that UST and UST repo clearing represents as one of the most liquid markets in the world that underpins secured dollar funding globally, said Darren Wilson, vice president and head of Sales in the UK and Middle East for Financing Solutions at State Street.

“The scope of those regulations as they apply to FICC [Fixed Income Clearing Corporation] members is effectively jurisdiction agnostic,” he explained. “If you are trading with one of those FICC members then, bar few exceptions, you are in scope for mandatory clearing…Everybody is potentially captured by that clearing mandate.”

He also noted there is a broad range of organizations impacted — including corporate treasuries, money market funds, mutual funds, pension schemes, hedge funds, or banks that do not have direct membership, some of which are expressing concerns about liquidity in a potentially bifurcated treasury market if the majority of USTs and UST repo shifts to clearing.

Wilson stressed that a one-year delay in implementation of the Uncleared Margin Rules (UMR) still came with a “mad rush for participants to get papered” and warned on the same situation brewing ahead of the mandated clearing requirements coming into force, adding that the sheer size of the market should be a wake-up call.

State Street has been a direct member of FICC for 20 years and has long been offering sponsored repo clearing, and Wilson noted the team sees roles for bilateral, cleared and peer-to-peer repo in multiple currencies, the latter of which has garnered significant interest in Europe.

European mandate?

Once the dust settles, if the US is successful in achieving regulatory objectives of safety and liquidity in the government bond market, it could be a good example for other jurisdictions to follow suit, although there are a variety of reasons it is unlikely to be a priority in Europe, he added.

“A lot of government bond repo is already cleared in Europe, particularly between the dealer banks, so the benefit might not be as pronounced as in the US where we are seeing potentially huge volumes moving into clearing,” he said.

At the same time, the European Central Bank and Bank of England is monitoring non-bank financial institutions, for which deleveraging activity in times of stress has shown volatility in the government bond market. Clearing could help dealer balance sheets during such unwinds but could also add to liquidity stress on cash margin calls, he explained.

“Whether (clearing) should be mandated at this stage I think needs some thought, also with T+1 around the corner there’s going to be a lot of calories burned on that project so maybe now is not the right time,” Wilson said.

Darren and Olivier will be joined by Nicola Danese from Tradeweb, Laura Klimpel from the Depository Trust & Clearing Corporation (DTCC), and BNY’s Simon Squire on the panel “Where is European Repo Market Structure Heading?” at Rates and Repo Europe on March 19. Rates & Repo is a conference for cash investors, dealers, market intermediaries, technology firms and other service providers. Register here for the in-person panel discussions.