US repo markets have seen rate changes in 2024, but 2025 already suggests a different kind of financial market environment following the recent election cycle. The dynamics that will impact repo rate volatility will be marked by a new set of regulatory priorities and a changing funding cycle.

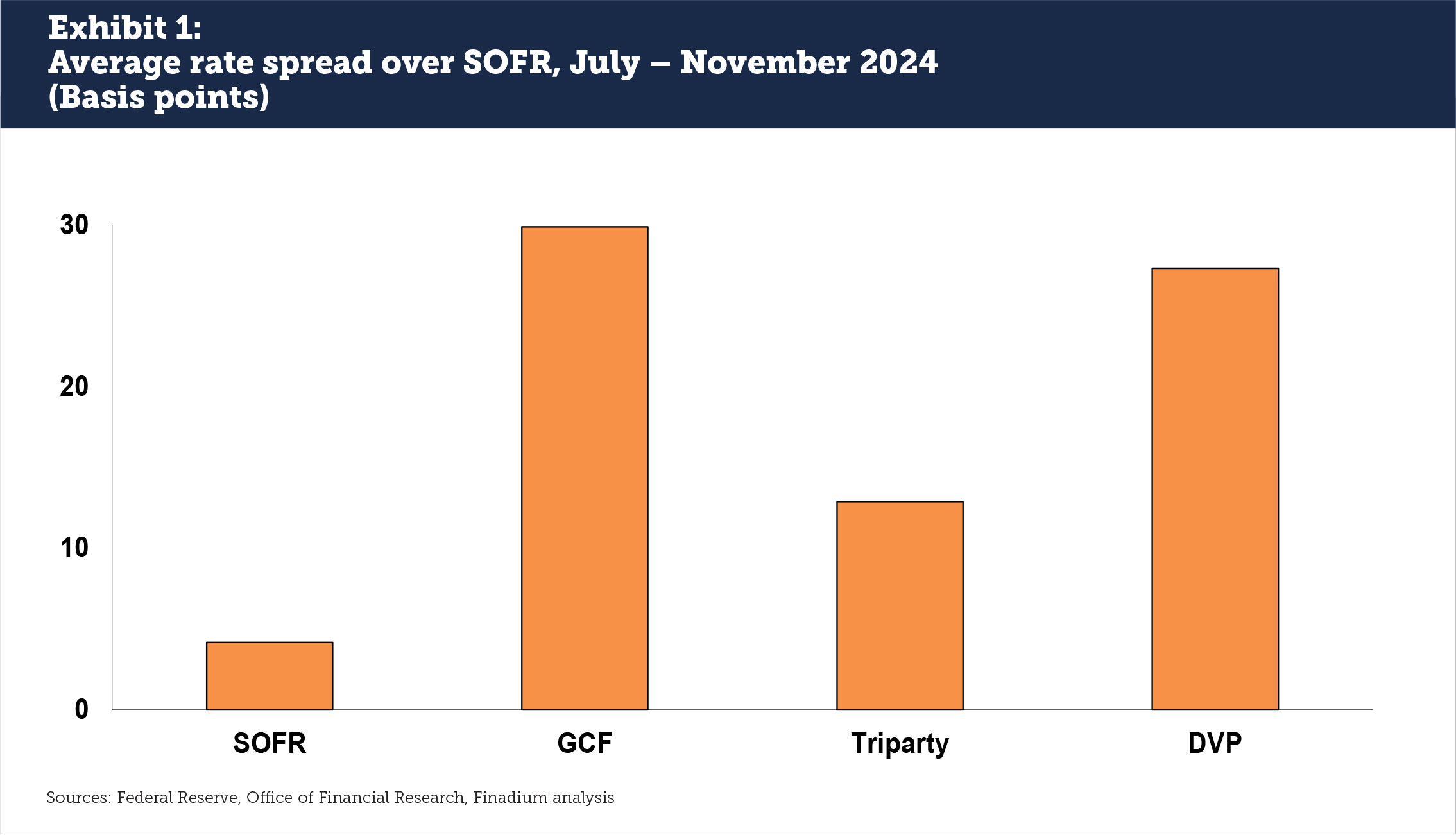

Quantitative Tightening is doing its job. Where US repo markets used to be entirely driven by the Federal Reserve’s Reverse Repo Facility (RRP) rate, dealer balance sheets matter again, with end of month rate spikes a regular feature of market activity. DVP rates are regularly higher than the RRP, SOFR and triparty, which means that the spread between borrowing and lending is working for dealer profitability. This is a healthy change from the Federal Reserve’s near-zero benchmark interest rate when the RRP was the single driving force in repo activity.

From July to November 2024, the average spread between RRP and SOFR, GCF, Triparty and DVP was between five and 27 basis points (see Exhibit 1). While the impact of less central bank intervention is evidenced, it also means that the market is open to greater volatility subject to the floor of the RRP and the general ceiling of the Standing Repo Facility (SRF), even if not all firms can participate on either side.

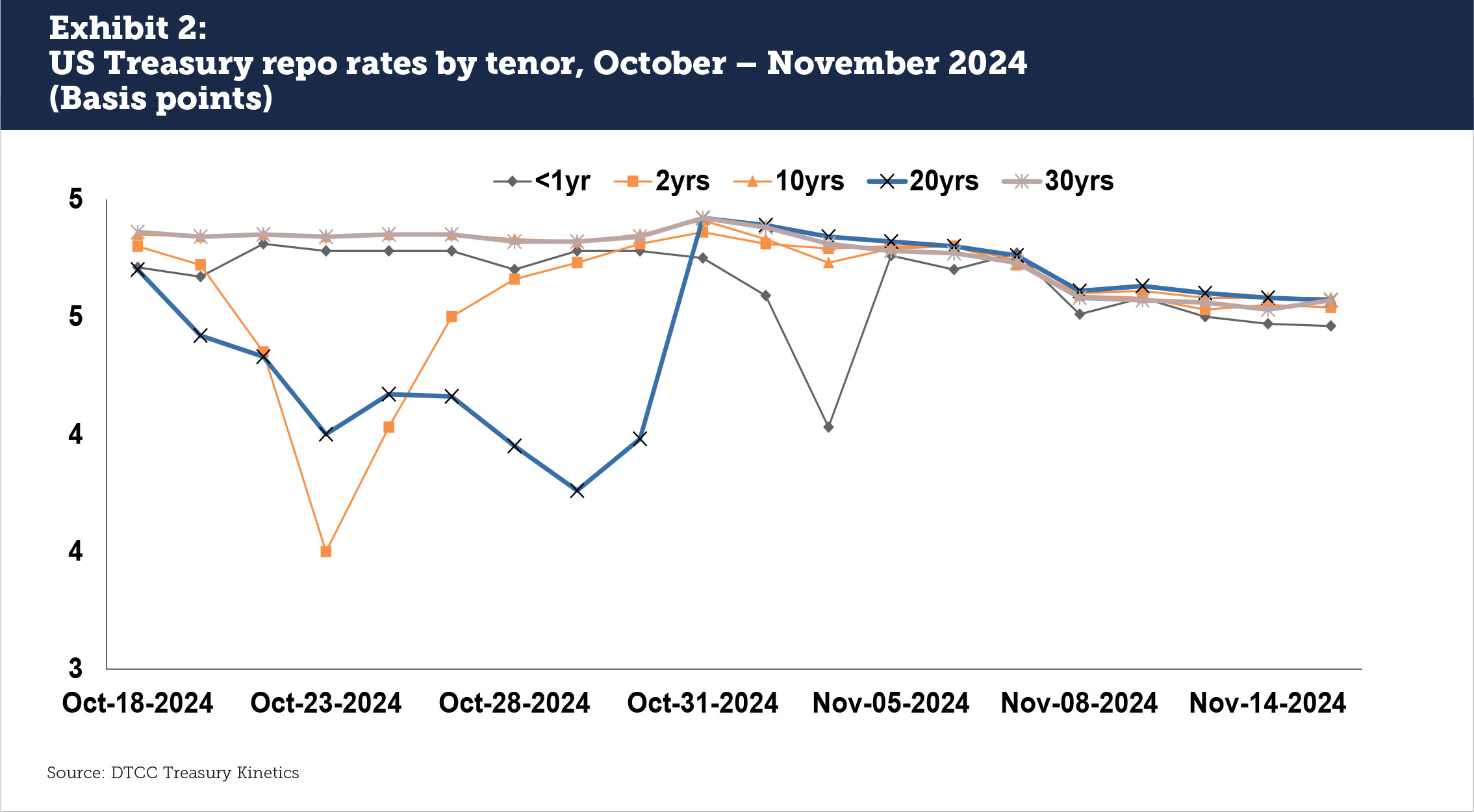

Individual US Treasury issuances continue to show signs of periodic repo rate volatility. Between mid-October and mid-November 2024, 2-year, 20 year and under 1 year issuance all turned special; US repo markets are not standing still, and there is reason to believe that further volatility will continue through next year (see Exhibit 2). There are additional concerns about term funding availability coming into year end, especially given the growth of cleared repo that operates on an overnight basis: speakers at Rates & Repo in New York in October 2024 noted that a lack of cleared term funding could become a potential problem.

A new regulatory outlook

A deregulatory agenda from the Trump administration is expected and will be evident across a Basel III Endgame re-proposal, the Securities and Exchange Committee’s rules on transparency and more. The window will be open for the adoption of permanent rules to exempt US Treasuries from bank Supplementary Leverage Ratio calculations. While the repo clearing mandate may be delayed, modified or even cancelled, this may not change the overall direction of market adoption however.

Making the US Treasury SLR exemption permanent is on the wish list of industry participants. ISDA wrote in its Q1 2024 update that “this will provide greater capacity for banks to expand their balance sheets and provide liquidity, enhancing the resilience of the Treasury market…. The letter to US agencies recommends the permanent exclusion should cover on- balance-sheet US Treasuries that banks hold in inventory or as part of their liquidity portfolios, as well as those received in repo-style transactions.” The Treasury Borrowing Advisory Committee, made up of industry professionals, recently told US regulators that “A permanent exemption could also be considered as part of holistic update [sic] of bank capital rules that balances the liquidity needs of the financial system while preserving resilience and stability of banks.”

The 2020 exemption allowed banks to exclude US Treasury repo from the SLR only if they included their broker subsidiaries in the calculation. Adding repo in any new rule would be a fresh innovation. The impact of exempting both US Treasuries and US Treasury repo on dealer balance sheets could be a surge in repo activity, given increased dealer capacity to hold and finance US Treasuries.

Based on the experience of 2020, making the exemption permanent could be a Federal Reserve decision and could be done quickly. Critics will argue that the move will increase systemic risk, but if conducted alongside mandatory clearing for US Treasuries and Treasury repo, much of the risk could be overseen and managed with strong oversight. Further, nearly everyone agrees that more US Treasury issuance is still to come, driven by large structural US deficits and it is uncertain who will buy this inventory. Allowing dealers to hold more US Treasuries without penalty solves an important funding problem for the US Federal Government.

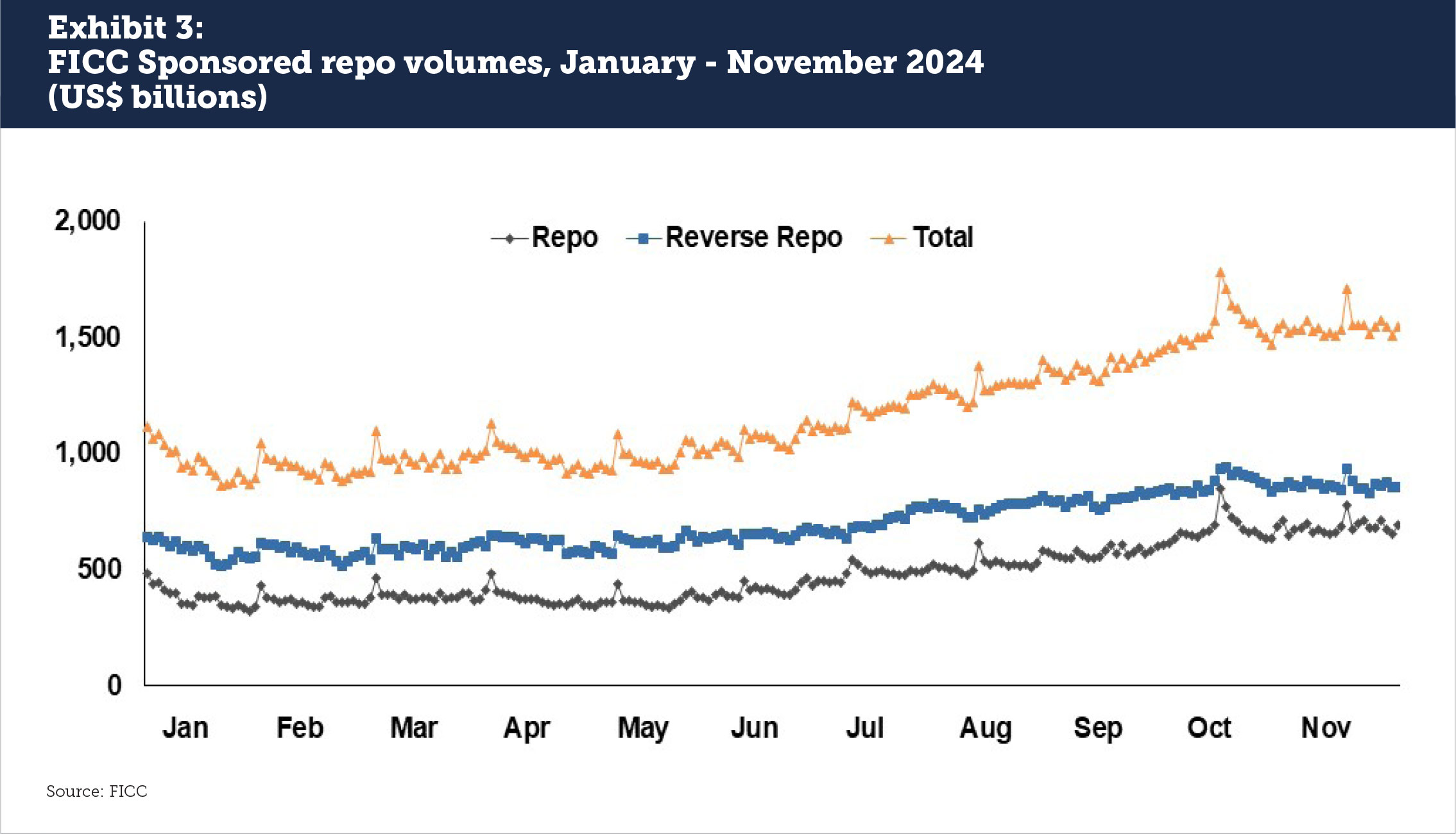

Some have also questioned whether the new administration will delay, pare back or eliminate the SEC’s mandatory clearing rule. The industry’s adoption of US Treasury repo clearing so far shows that there are benefits to be gained to the market (see Exhibit 3). Even if the mandate does not hold and there is no change to the SLR, our expectation is that adoption of repo clearing will continue apace. An SLR exemption and no mandate however could give further support to the bilateral market. Given the many areas that new regulatory heads will be looking at, these issues may not get resolved until later in 2025.

Funding needs driven by asset class

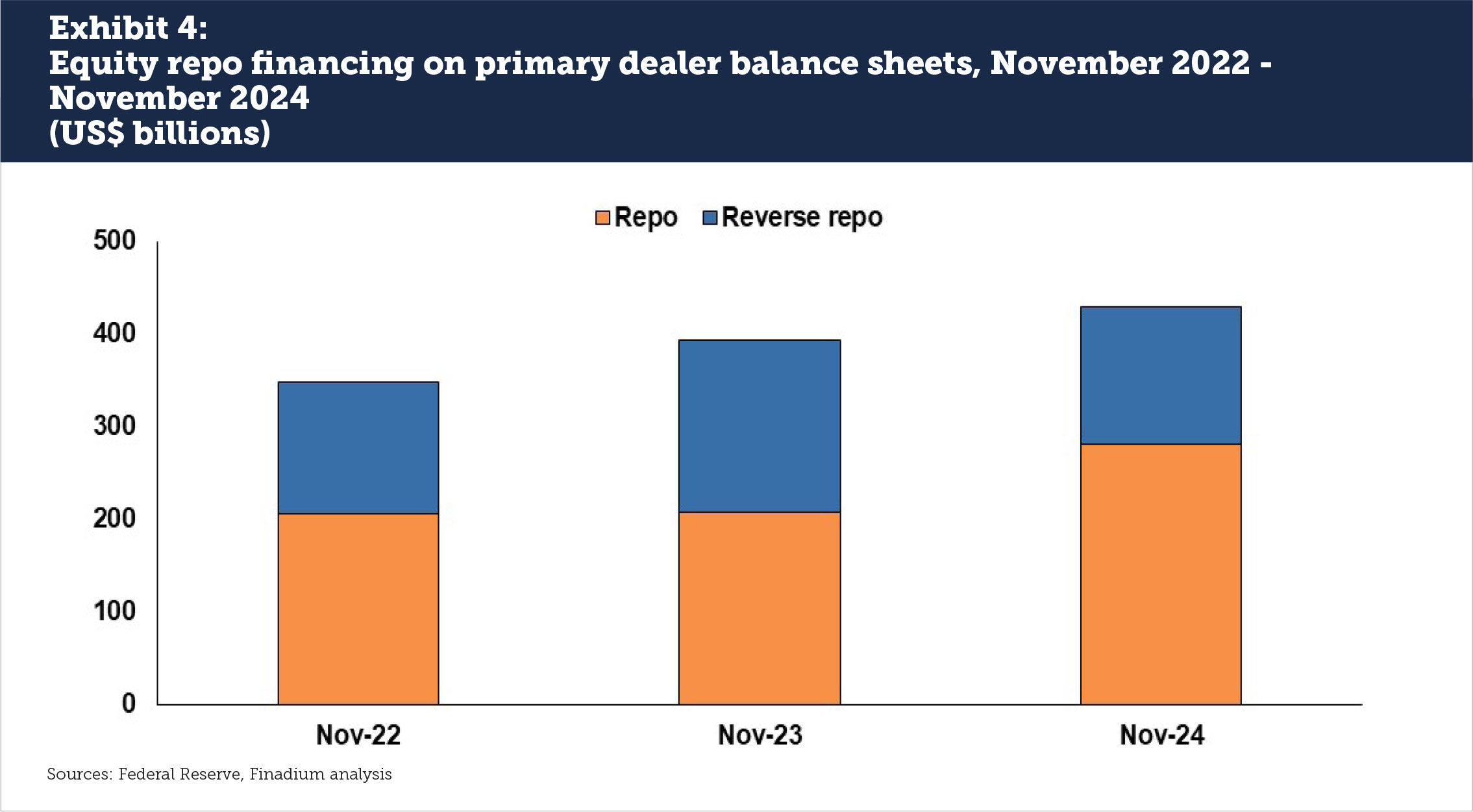

Funding and financing markets are reactive to broader market trends. As an example, with the S&P 500 on a recent upwards streak, the need for equity repo financing has also increased. From November 2022 to November 2024, the amount of equity repo on primary dealer balance sheets grew by 24%, or $82 billion (see Exhibit 4). A market defined by greater volatility across sectors due to uncertainties in policies or geopolitics will see similar ups and downs in both volumes and rates.

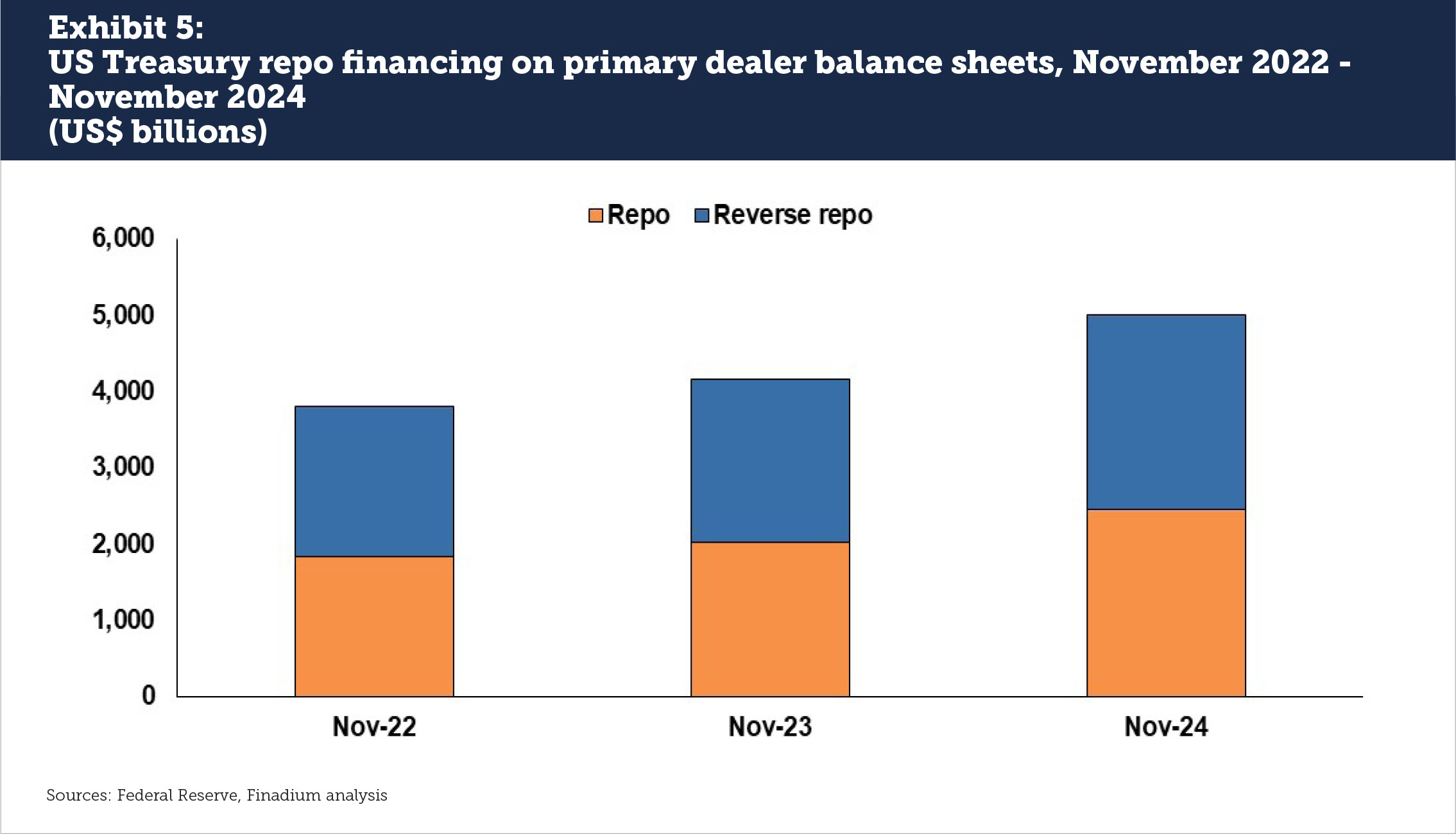

US Treasury funding demand has been up steadily from 2022 to 2024 but for very different reasons than equity repo. In US Treasuries, increased issuance means a surging overall market. Over the last two years, US Treasury repo on dealer balance sheets has grown 31%, or $1.2 trillion (see Exhibit 5).

In US Treasuries, funding needs will continue to be a function of issuance and client purchasing behavior, or a lack of same. The more real money buyers of US Treasuries, the less need for repo financing, but if the basis trade continues to make an impact, then more repo will be required. Likewise, increased issuance could mean fewer real money buyers and a greater need for primary dealers to finance the positions they are holding.

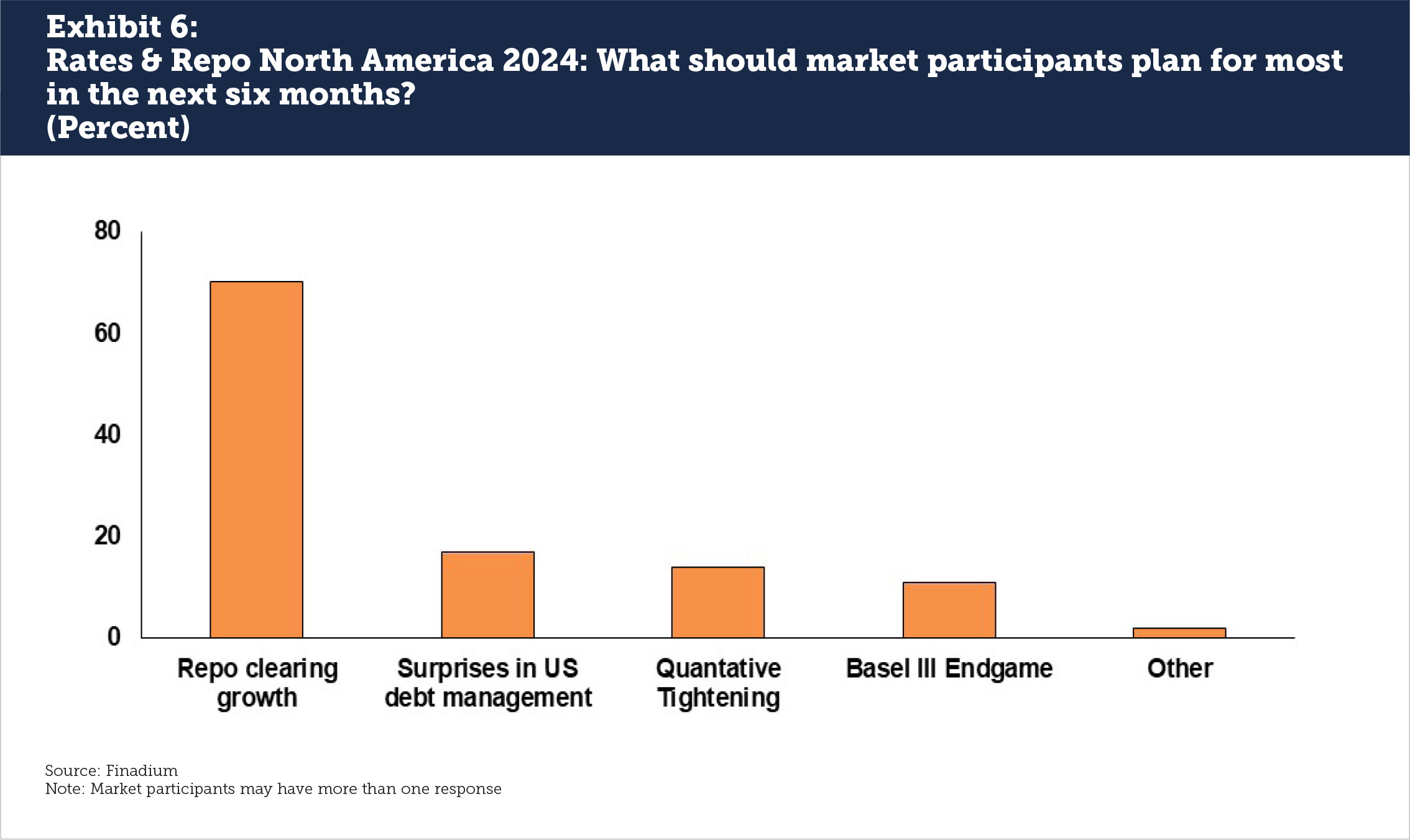

Market participants are watching the ground closely for drivers of repo disruption: at Finadium’s Rates & Repo North America 2024 conference, 70% of respondents said that repo clearing was the most important area to plan for in the next six months, followed by surprises in US debt management and additional Quantitative Tightening (see Exhibit 6).

While the specifics of how volatility and demand will play out in 2025 remain to be seen, a framework for understanding the market is already coming into place. Quantitative Tightening that leaves more room for dealer repo activity, deregulatory priorities likely to impact repo and repo clearing, and asset class specific trends will combine to drive individualized dynamics for investors and intermediaries. 2025 is likely to be a year to remember.

This article was commissioned by DTCC Data Services. However, the opinions expressed herein are solely those of Finadium and the article’s author. DTCC does not endorse these opinions, and they do not necessarily represent the opinion of DTCC or any of its affiliates.