The merging of siloes across repo and securities lending operations continues at a steady pace. In a new development, S&P Global Market Intelligence has launched a data product that compares repo and securities lending rates and can lead to actionable trades. It creates new opportunities for banks, agent lenders and investors to analyze data, optimize their operational frameworks and consider the value-add of their own funding and financing strategies.

The historical separation of repo and securities lending desks happened naturally: securities borrowers at prime brokers were working for hedge funds shorting securities while repo was more of a financing tool for funds looking to raise cash and leverage. While this model held up well for decades, the pressures of balance sheet management in the Basel III era forced a rethink. Now, with both repo and securities lending used alternately to support regulatory capital and client trading needs, should they be seen as one stream or still separate depending on usage?

Some firms have already concluded that all funding and financing activities should be traded on one desk while others have merged operations for collateralized trades and kept different client-facing teams for each product. Still others have created Financial Resource, Treasury or Central Collateral desks that take an overview position of each individual trading desk to optimize exposures across the firm. And in the most recent twist, a few firms are undoing the merger of siloes on the front end to re-create securities lending and repo desks while building up their collateral optimization and inventory management capabilities across the firm.

The next step in driving cross-product efficiency between repo and securities lending is a data set that compares the same product’s fees across different markets. This can be done by individual ISINs or rolled up to create real and synthetic indices in bilateral and exchange-traded markets. This complex task relies on two main factors: a large amount of data and the ability to manage it effectively either by a trader or computer. The new repo and securities lending comparison service from S&P Global Market Intelligence delivers both.

This creates a new opportunity for firms of all sizes to better understand their market positioning, pricing and next collateral trading opportunities. If better data is an enabler of more efficient trading and post-trade activity, then taking advantage of data that compares identical products across multiple markets is a fundamental building block of the process.

The value of assessing repo and securities lending data side-by-side

Data-driven borrowing and lending decisions have become standard in both repo and securities lending. From sophisticated vendors to artificial intelligence (AI) models that price a wide range of securities for automated trading, market participants have grown comfortable with large data sets that are consumed in near-real time.

A side-by-side analysis of repo and securities lending data takes what firms already do manually to the next level by delivering a faster and more standardized means of determining optimal assets for each product use. Whether the activity is lending in one market or the other, or accessing liquidity to help avoid shortages and maximize funding efficiency, comparable data across markets is the first way to start. This can lead to enhanced lending strategies by assessing demand and pricing trends as well as provide flexibility to both trading parties on terms and collateral requirements. Better data also support conversations with regulators and internal risk teams on market monitoring across collateral quality, counterparty risk and volatility management.

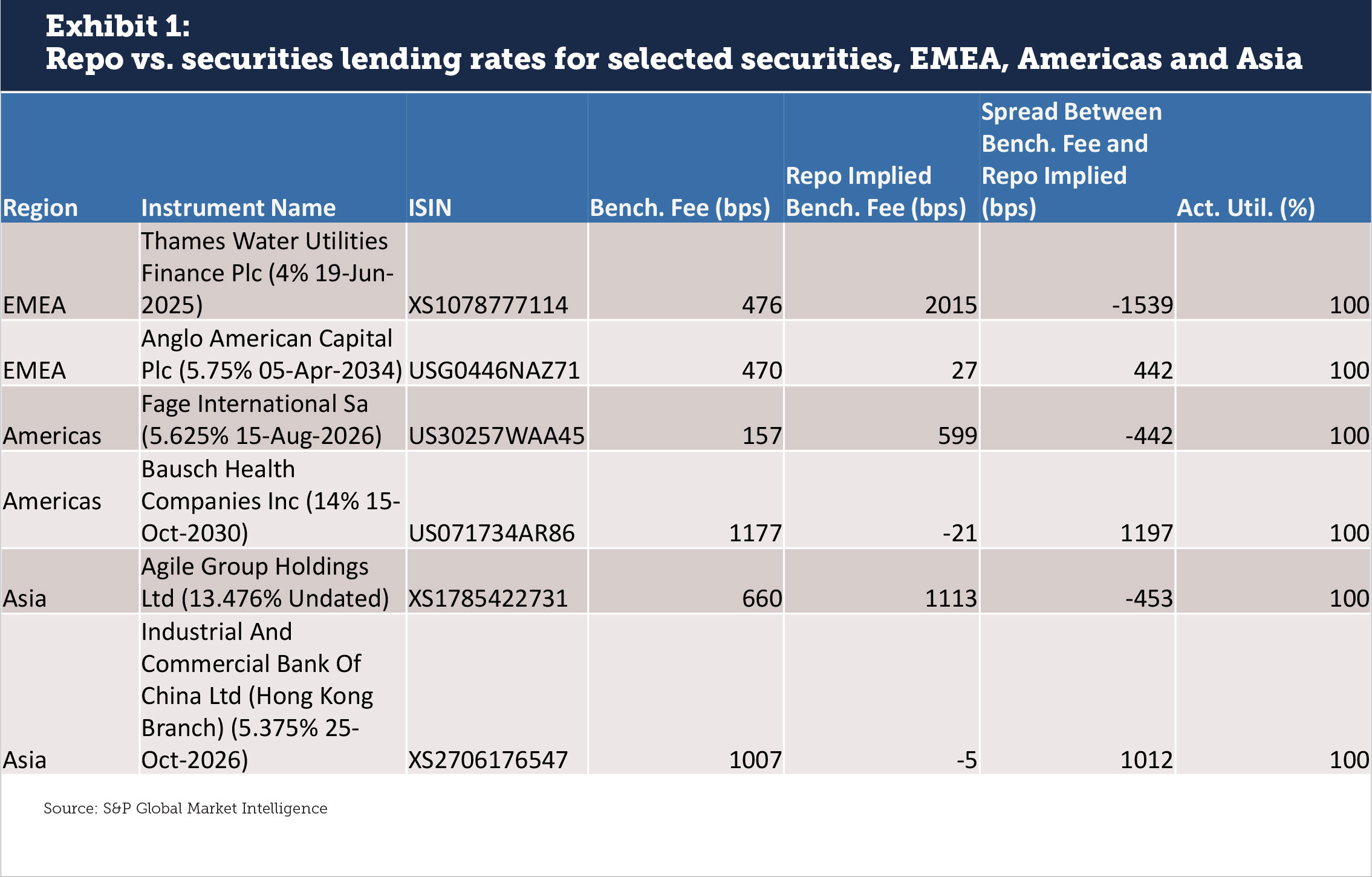

The data now provided by S&P offer snapshots and visualization tools for market analysis. A recent review provided to Finadium found no fewer than 60 ISINs where the spread difference between the securities lending benchmark fee and the repo rate for the same security varied by at least 133 bps and hit a high point of 1,539 bps. Rate discrepancies are evident in Europe, Middle East and Africa (EMEA), North American and Asian securities, including names with high utilization rates (see Exhibit 1).

Data digitization, standardization and AI

A challenge in any data analysis in capital markets today is who has the bandwidth to assess large amounts of information in a short enough time to make actionable decisions while the data are still fresh. Automated analysis has become the only real way to get this done, with AI tools and natural language processing (NLP) as the next step in the evolutionary chain.

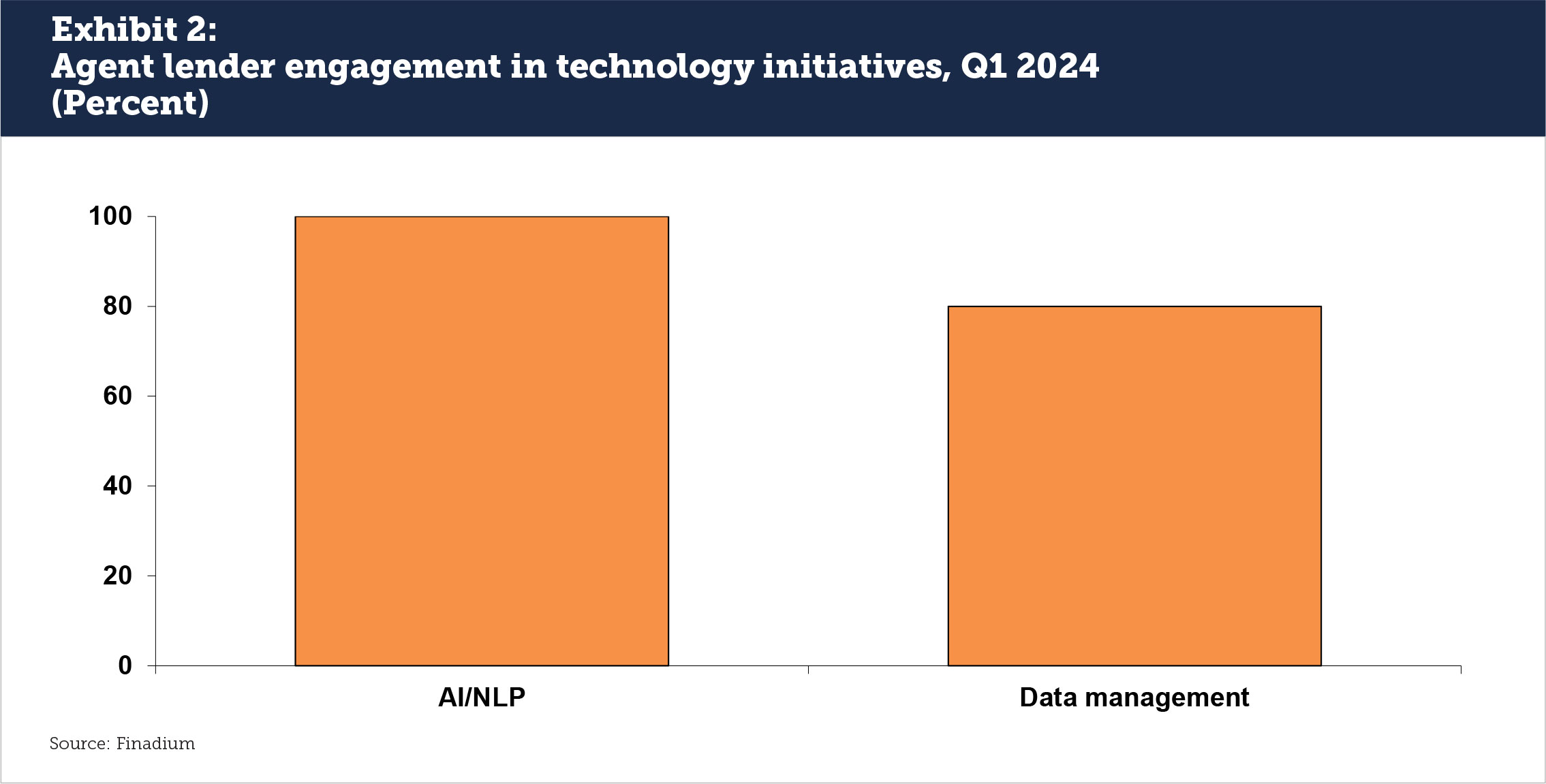

Securities finance market participants are already employing AI in their daily work environment: Finadium’s 2024 survey of agent lenders found that 100% of firms were using AI and NLP but most of the implementations so far were in writing text and other non-trading desk functions (see Exhibit 2). However, 80% of agents were focused on data management as a priority for 2024. The more that data frameworks are in place, the easier adding another element becomes versus starting from a visual trading screen.

For firms without their own data infrastructures, a service that pre-organizes all repo and securities lending rate data categorized by comparable ISINs is a substantial leap forward. Securities lending and repo data arrive in unstructured formats across multiple markets. The work of standardization has been made easier in some cases by Europe’s Securities Financing Transactions Regulation but more difficult at the same time by the magnitude of reporting obligations that firms face across multiple jurisdictions and formats. The value proposition of the S&P service then is to deliver this standardization using tools that can be absorbed in a variety of formats, from human trader to data algorithm.

Will specials repo rates become standardized?

Data providers are a principal reason for the standardization of securities lending rates. Traditionally, every firm used to price their General Collateral (GC) and specials according to their own needs, with the market converging on a range of expected GC fees based on the regular collection of data. If any firm is off the market on trade date, they are now able to reprice on T+1 to get an expected better deal for their client. This in turn creates the opportunity for performance reporting by agent lender, prime broker and client segment.

Such a dataset has never existed in repo specials trading until now; the specials market has continued to be priced based on counterparties, availability and opportunity. The standardization of repo data alone into a new type of feed could become a launch pad for reducing disparities and creating uniform pricing. When compared against securities lending data, pricing differences could potentially get arbitraged out of the market as firms recall and redeploy their assets to better markets, or reprice based on equivalent outcomes.

This is not a foregone conclusion: even with standardized data, there will still be opportunities for differentiated pricing in bilateral markets that may favor one counterparty or another: scarcity, legal documentation and counterparty relationships continue to matter, as they do in securities lending. This may lead to a natural variation in pricing that extends far beyond clearing mandates for government bond repo and other market structure changes. There is no certainty that just because market data exists, traders will arbitrage all opportunities down to a minimum spread.

However trading patterns evolve, the new data set from S&P Global Market Intelligence advances repo and securities finance rate analysis by considering parallel trading opportunities in two closely related markets. As discussed on a recent Finadium webinar on cross product arbitrage in collateral markets, for anyone managing a collateral book, having a holistic view across the financing market is now essential for both margining and optimizing collateral positions efficiently. The opportunities for data analytics in this space continue to be large, creating ongoing efficiencies for market participants in funding and financing optimization.

This article was sponsored by S&P Market Intelligence.