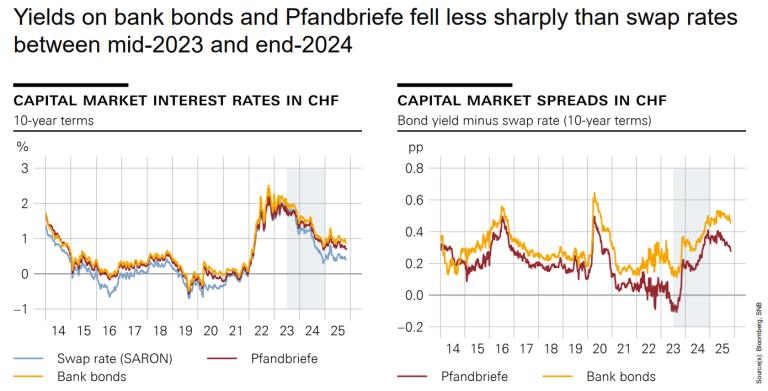

the interest rates at which banks secure funding in the financial market have fallen less sharply than the general level of interest rates, meaning that bank funding costs in the financial market have increased relatively speaking.

What explains the rise in swap spreads, i.e. in bank funding costs? In a recent speech, Petra Tschudin and Thomas Moser, member of the Governing Board and alternate Member of the Governing Board at Swiss National Bank (SNB) highlighted three key explanations.

- the higher yields on foreign government bonds relative to the corresponding swap rates;

- the structural change in the Swiss banking market following the acquisition of Credit Suisse by UBS; and

- developments that have made banks’ liquidity management more challenging.

“These three factors have led to a higher liquidity premium on funding instruments. Given that the creditworthiness of the Swiss banks and mortgage bond institutions has remained stable, we can practically rule out the rise in the swap spread being attributable to higher credit risk,” they said.

Future expectations

The international environment currently suggests that a rapid decline in funding costs is unlikely. It is true that quantitative tightening by central banks – in other words, the pace at which they are selling securities – has slowed of late. However, a reduction in the spread between government bond yields and the corresponding swap rates is counteracted by high government borrowing needs.