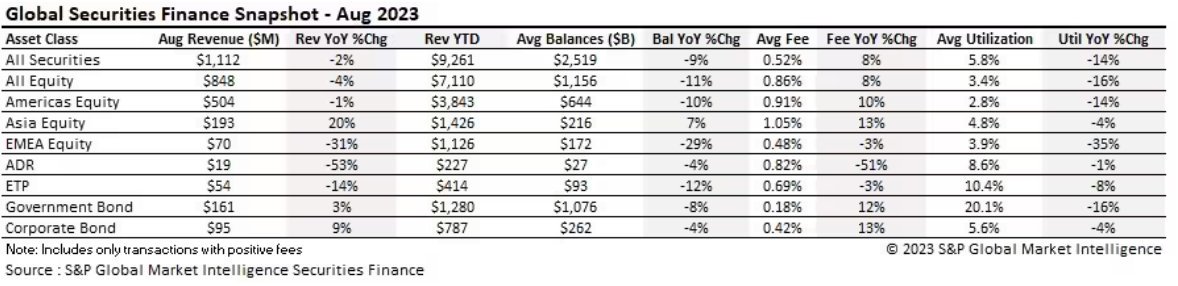

S&P Global Market Intelligence released its securities finance snapshot for August, reporting securities lending revenues of $1.112 billion generated throughout the month of August. APAC equities outperformed, posting +20% year-over-year (yoy) increase in revenues. Specials activity persisted across US equities, while across Europe, Middle East, and Africa (EMEA), borrowing demand softened.

Securities lending revenues were down 2% yoy and 1% month-on-month. Despite this decline, revenues during the month remained significantly higher when compared with both August 2021 ($897 million) and August 2020 ($648 million). Revenues are also approximately 9% higher year-to-date when compared with 2022, 28% when compared with 2021 and an impressive 46% higher when compared with 2020.

Fees across all securities increased 8% yoy whilst balances declined 9% and utilization fell by 14% yoy. This is a common theme throughout the securities lending market during this year – higher revenues supported by higher fees but smaller on loan balances.

Equities across Asia performed well throughout the month posting an increase in revenues of 20% yoy. Revenues declined across the Americas and Europe, with EMEA being the only region to also show a decline in average fees (yoy).

In the fixed income markets, continued strength was seen across both government and corporate bonds. Revenues continued to grow yoy, posting increases of 3% across government bonds and 9% across corporate bonds. Balances continued to decline across both asset classes over the month, but average fees remained strong, despite corporate bonds posting their lowest monthly average fee (42bps) of the year so far.