Building on our conversations with dealers on what DTCC-Euroclear Global Collateral Ltd’s Inventory Management Service (IMS) could offer them, we looked further at the business rationale for why US market participants would want to consider mobilizing their US assets in European tri-party platforms.

Global repo markets remain in transition. As a recent Bank for International Settlements paper, “Repo Market Functioning,” noted: “Underneath the relative stability in headline measures of activity and pricing, there are signs of banks being less willing to undertake repo market intermediation, compared to the period before the crisis.”[1] In other words, dealers want to go home breaking even at the end of the day. While some may argue against the idea that even now there is relative stability, all would agree that banks are taking a lower risk view towards credit intermediation in the market, which impacts liquidity.

At the same time, US tri-party repo reforms have created structural changes in how the market functions on a daily basis. The extension of credit by tri-party repo clearing banks is now comfortably under 10% of the entire book of business; repo settlement happens at 3:30PM, and data collection has been increased for the benefit of market participants. Along the way, a market closing at 3PM for the day has increased stress and limited access to tri-party repo for money managers, creating new obstacles. J.P. Morgan’s decision to exit government clearance means that BNY Mellon will become the sole clearing agent for FICC’s GCF platform.

Cash supply and demand in US tri-party repo

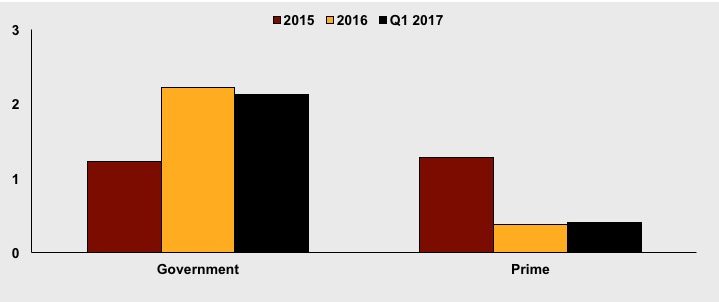

Supply and demand trends are changing as well. Investment Company Institute data show significant changes in money fund assets since the final implementation of money market reform. Government money fund assets shot up by US$1 trillion before losing almost US$100 billion in assets between 2016 and 2017 (see Exhibit 1). Meanwhile, prime fund assets have shrunk by 69%.

Reforms targeting triparty repo and money market funds have compressed the market for cash into a narrower set of outlets. Whereas top rated prime funds once had a wide range of investment outlets, they are now constrained to the same limited class of investments as other cash investors – HQLA government backed debt. Cash investors seeking enhanced yields through more generous prime funds, or simply an incremental boost over a residual bank deposit, no longer have this option.

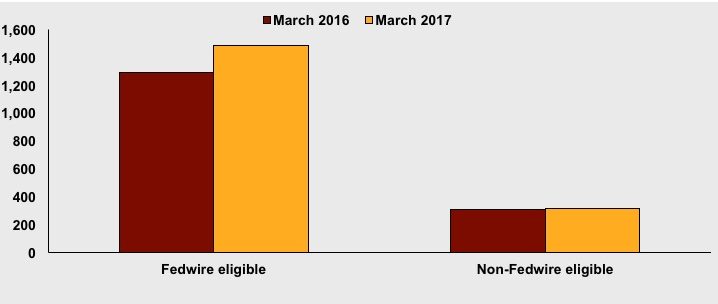

Federal Reserve data on US tri-party repo show how flat the market is for non-Fedwire eligible collateral, and just how concentrated the market has become. While there was a measurable jump in total tri-party repo activity between March 2016 and March 2017, nearly all the increase has gone towards Fedwire eligible instruments (see Exhibit 2).

There appears to be evidence that major market participants have absorbed the majority of changes related to leverage ratios, asset mix, and capital liquidity requirements. In March 2017 and December 2016, major events and reporting periods have not resulted in sharp rate spikes.

Market feedback on tri-party functionality

Functionally, the US tri-party repo market is working well. The FICC can process large volumes of transactions, the Federal Reserve’s Reverse Repo Facility recently hit a high watermark of nearly US$500 billion, and BNY Mellon and J.P. Morgan report that all systems are working. Outside of the mechanics however, there is the question whether market participants are getting what they want out of repo. On this point we are less certain.

For cash investors, the 3PM cut off is a challenge, and all investors have felt or at least heard of the liquidity/balance sheet difficulties in repo and reporting periods. Especially at quarter-ends, cash investors say that they know who they can trust and who they expect will disappear on them. This is not a reliable system.

While US CCPs are working to expand access to the buy-side as repo cash providers, there’s little excitement generated so far. The buy-side does not yet see what is really in it for them. Dealers are also uncertain; if facing off against cash providers only, they would lose the balance sheet benefit of netting and would face higher CCP charges to cover buy-side participation.

Direct, Peer to Peer, and All to All markets are being considered as an alternative and some of this would go through tri-party. To gain traction though, these programs may require some fundamental changes in both the behaviors of repo participants and serious rethinking of risk models and credit standards, particularly on the part of the most restrictive cash investors. While insurance companies and corporate and public pensions may be more amenable to these opportunities than asset managers, large segments of the market will remain dependent on the traditional dealer-driven repo model for some time to come.

Would mobilizing US assets in European tri-party platforms help US participants?

The vast majority of the repo business has concentrated into a handful of places: CCP’s, fixed income tri-party, and fixed income bilateral repo. Regulators and market oversight bodies seem well-satisfied with a state of affairs where most repo cash is centrally cleared through regulated dealers or cleared through the next best thing: a major tri-party agent.

That said, the US and European models for tri-party repo settlement are different in a way that might provide an advantage to US market participants accessing DEGCL’s Inventory Management Service. To start with, collateral schedules are more flexible in Europe especially for equities, whereas the US culture of repo is highly focused in US Treasuries and other Fedwire-eligible instruments.

The key advantage the IMS offers the market is to provide operational integration between US market participants and the Euroclear tri-party environment. Limited appetite for these transactions and more restrictive collateral schedules in the US make the European market a more flexible alternative. By eliminating a large risk component and significant part of the costly overhead that comes with cross-border transactions, Euroclear could become an easier venue for US firms to consider as they look at their overall opportunities and strategy.

Prior to the IMS, it has been an operational challenge and a potential risk for US dealers to transact bilaterally in corporates and asset backed securities with counterparties that would prefer to see this collateral run through the Euroclear infrastructure. Where dealers have cross asset and cross jurisdictional flexibility, those benefits should translate into better spreads and yields throughout the system.

The benefit to repo investors and their dealers in this effort is to provide an operationally and capital efficient bridge between US and European participants, without requiring any significant changes in either credit standards or investor behaviors. For US cash providers, this will help to open up the Euroclear tri-party environment as an alternative to BNY Mellon tri-party, giving investors access to a greater number of cash buyers. We do not see this as major competition to BNY Mellon at this point but rather as a useful alternative, especially for equities-backed tri-party.

[1] “Repo Market Functioning,” Committee on the Global Financial System, Bank for International Settlements, April 2017, available at https://www.bis.org/publ/cgfs59.pdf

This article was commissioned by DTCC-Euroclear Global Collateral Ltd.