A changing market structure means that the sources and uses of repo data will also change. DTCC’s Fixed Income Clearing Corporation (FICC) data is expected to grow in importance as most of the US Treasury repo market becomes centrally cleared. Market participants across dealers, cash providers and collateral providers should be prepared to capture and analyze repo data across current and expanding providers.

Regulations have created a new direction for US repo markets: starting in June 2026, FICC projects that an incremental US$4 trillion of US Treasury cash and repo trades will come into clearing. While not the entire universe, a move of this size could mean that individual data sets for this asset class become less relevant to a portion of the market as more settlement migrates away from bilateral counterparties and to central counterparties (CCPs). Intraday trading data and access to electronic markets will remain critical but a new and large segment of users may arise, looking mostly for end of day data; FICC is expecting to onboard a minimum of 7,000 new intermediary-indirect participant accounts before go-live.

A key question is whether the current relationship-based model of repo trading today could become less important as commoditized and standardized repo contracts become a market norm. Developments like the Agent Clearing Model and done-away trading with a segregated margin model could encourage a change in this direction. On the other hand, strong relationship-driven activity could lean more towards an omnibus model where a sponsoring dealer is responsible for posting margin.

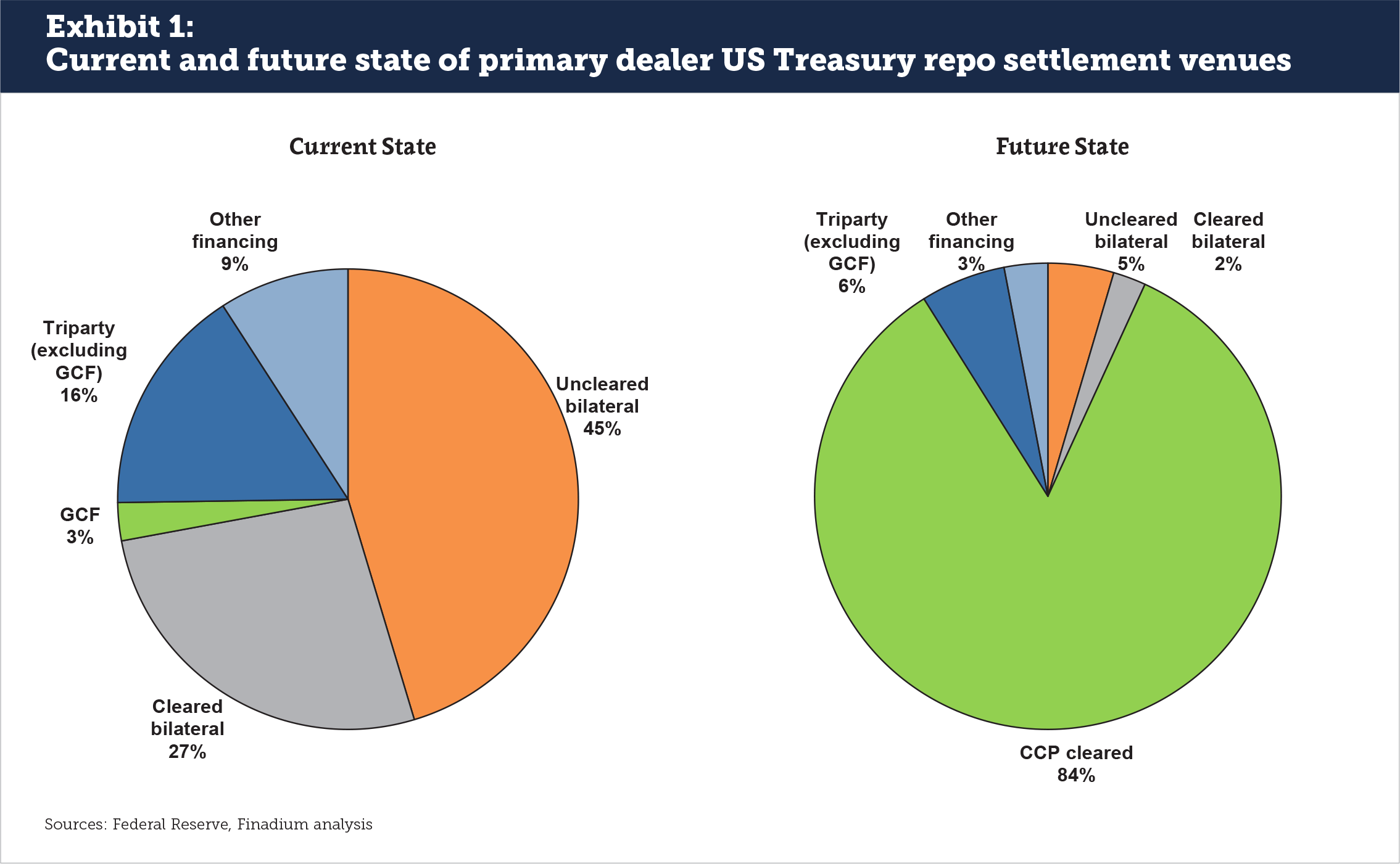

The scale of change in central clearing is significant. FICC Sponsored Repo currently settles around US$1 trillion daily and the GCF Repo service another US$42 billion (with US$460 billion outstanding). The future state will shift volumes from uncleared bilateral, triparty, and other financing to a CCP. In a May 2024 ruling, the US Office of Financial Research found that around US$2 trillion would move from the uncleared bilateral repo markets to central clearing. Based on primary dealer settlement data, we project that the percentage of cleared US Treasury repo will rise to 84% by the end of 2026 (see Exhibit 1).

The scale of change in central clearing is significant. FICC Sponsored Repo currently settles around US$1 trillion daily and the GCF Repo service another US$42 billion (with US$460 billion outstanding). The future state will shift volumes from uncleared bilateral, triparty, and other financing to a CCP. In a May 2024 ruling, the US Office of Financial Research found that around US$2 trillion would move from the uncleared bilateral repo markets to central clearing. Based on primary dealer settlement data, we project that the percentage of cleared US Treasury repo will rise to 84% by the end of 2026 (see Exhibit 1).

US Treasury repo data consumers should consider now what kinds of data they will need to source and where they will get it from. As most of these trades move to central clearing, what value will different market data sets provide? Will FICC data across market segments like GCF Repo service and Sponsored become the same or will there be important differences to consider? And what complementary data sets may be necessary to get a full picture of the market?

Data users: from human to database to AI

The transition is ongoing from humans looking at trading screens to quantitative databases to artificial intelligence (AI) that digests information on a massive scale. In a June 2024 survey of 10 of the largest securities lending agents, Finadium found that 100% were using AI within their organizations for tasks from writing text for Requests for Proposals to actively analyzing market opportunities and proposing trades to humans. While no large bank is ready to have AI push the “trade now” button, and regulators have voiced their discomfort with this last step as well, the technology is capable once humans decide the time is right.

The market for data users is global and highly segmented. Some institutions are placing cash and want to ensure they have a fair rate; not even the best rate, but at least a fair rate relative to their liquidity needs. Collateral providers operating in competitive trading environments on the other hand may insist on the best rate relative to the importance of the relationship or are prepared to take their business elsewhere. Treasury and risk management teams, along with regulators, may be creating exposure or liquidity models based on repo inputs.

A new generation of data-hungry end-users may emerge that need repo data plugged into their reporting platforms. A main objective is to show themselves and their investors that they are exercising proper care when getting financing rates. Without this data, they may open themselves up to criticism or potentially lose business to competitors who are better prepared. AI or versions of heavy automation will be a core component of this process.

Sources of data

The evolution of clearing models will impact use data requirements. If FICC offers several different popular repo clearing services (Sponsored, Agent, GCF), then the market will want to see how it is priced on each one. There could potentially be pricing differences and hence arbitrage based on settlement venue, and this could give rise to a new kind of market data demand to take advantage of a new kind of basis trade. A consolidation of clearing data at FICC will bring convenience as well: interfacing with FICC alone instead of multiple settlement venues means fewer vendors to manage and fewer points of interconnectivity.

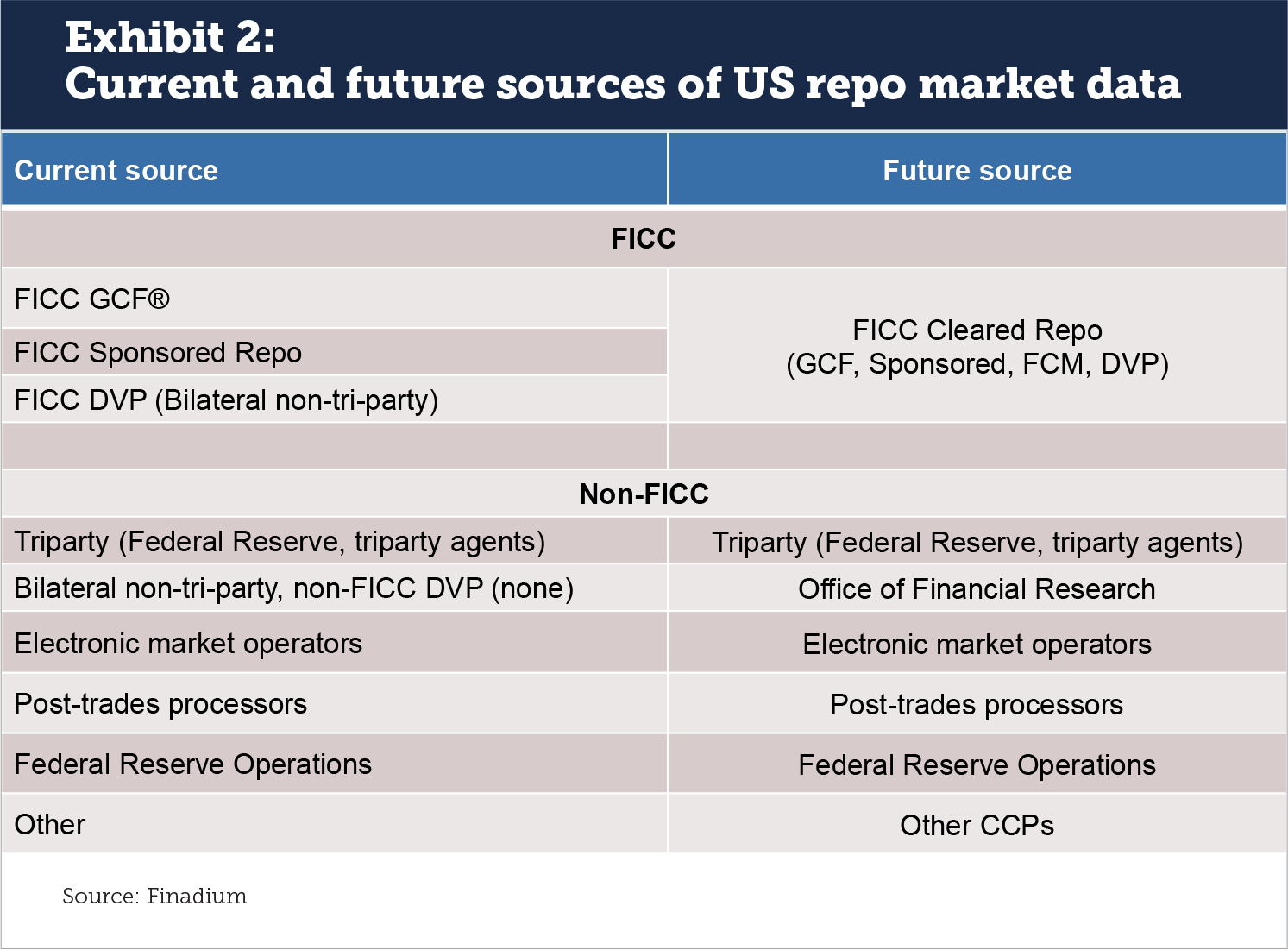

While there will always be demand for intraday data, users that need end-of-day-data only may gravitate to CCPs where transactions are cleared. A variety of DTCC and non-DTCC sources may become more necessary for the industry going forward (see Exhibit 2). Intraday data should still be provided by electronic trading platforms, market data platforms and the remaining messaging platforms.

While there will always be demand for intraday data, users that need end-of-day-data only may gravitate to CCPs where transactions are cleared. A variety of DTCC and non-DTCC sources may become more necessary for the industry going forward (see Exhibit 2). Intraday data should still be provided by electronic trading platforms, market data platforms and the remaining messaging platforms.

DTCC’s Treasury Kinetics product serves the market as a powerful tool that could enhance data requirements as a result of the evolution of clearing models. Sourced from DTCC’s Fixed Income Clearing Corporation’s (FICC’s) Government Securities Division (GSD) platform, the DTCC Treasury Kinetics service provides users across the dealer, hedge fund, and asset manager communities additional transparency into the Delivery vs. Payment (DVP) repo market.

Relationship or commodity?

In a market where relationships matter, measuring best execution is difficult and may not be important relative to the bundle of other services a client receives from a bank. Clients can say to their investors that they are treated well on a holistic basis without the need to prove that quantitatively. At the other extreme, best execution in a market like large cap equities can be necessary to demonstrate to institutional investors. It is not yet known how much US Treasury repo clearing will commoditize the market, but this should be on the minds of both dealers and clients on both sides of the trade.

The next two years will start to answer the question about whether the new repo landscape will be driven by relationships or standardized, commoditized products. This may seem like ample time to answer questions about data use and sourcing. However, the real timeline is closer to 12 months: UST repo clearing goes live in June 2026, meaning that dealers and clients must decide on a data strategy some time in 2025 to start working on execution. After that, firms will need to begin executing on contracts and adjustments to technology systems to ensure readiness for the US Treasuries cash portion of the mandate by the end of 2025.

If even a portion of the market migrates to a more commoditized repo environment, a new generation of data utilization may emerge by humans and machines that dwarfs the size of today’s demand. The more central a data set, the greater the likelihood that market participants will adopt it as a standard that the entire user base can agree on. This in turn may push commoditization even further, leading to a self-reinforcing feedback loop in data-driven trading and analysis for the repo markets.

This article was commissioned by DTCC Data Services. However, the opinions expressed herein are solely those of Finadium and the article’s author. DTCC does not endorse these opinions, and they do not necessarily represent the opinion of DTCC or any of its affiliates.