Pricing in the current Prime Brokerage market remains competitive due to various factors including excess liquidity, new entrants, and a renewed focus by institutions to attract and retain stable accrual revenue streams in light of challenges to historical commission businesses which have been impacted by regulatory frameworks (such as MiFID) and low trading volumes. Another factor which has been prevalent the past few years which has had an impact on bank’s securities lending desks has been the shift from conviction (single name trades) to more sector based (ETF’s) shorting strategies. The ability for institutions like Wells Fargo to understand the changing dynamic of client trading activity and leverage their platform to provide value to their clients is more critical than ever before. A guest post from Wells Fargo.

It is critical that there is open dialogue around pricing between Prime Brokers and their hedge fund clients in order to ensure the value proposition of the relationship is understood by both parties. As prime brokers and hedge funds have become increasingly sophisticated in understanding the financial resource consumption (Balance Sheet / RWA) and subsequent return profile of their activities, it is a key factor in valuing the relationship. Although return metrics are not the predominant driver that it once was as net revenue has been at the forefront in recent years given the excess liquidity which has been prevalent, Prime Brokers still review client profitability to ensure they are tracking to business targets. That may be offset by the advent of hedge fund treasury funding desks which allow a fund to have a holistic funding view across all of their funding counterparts and employ funding strategies to optimize the fund’s return profile. This review is not necessarily specific to prime brokerage, as hedge funds have deployed this approach across their equities, fixed income and derivatives activities.

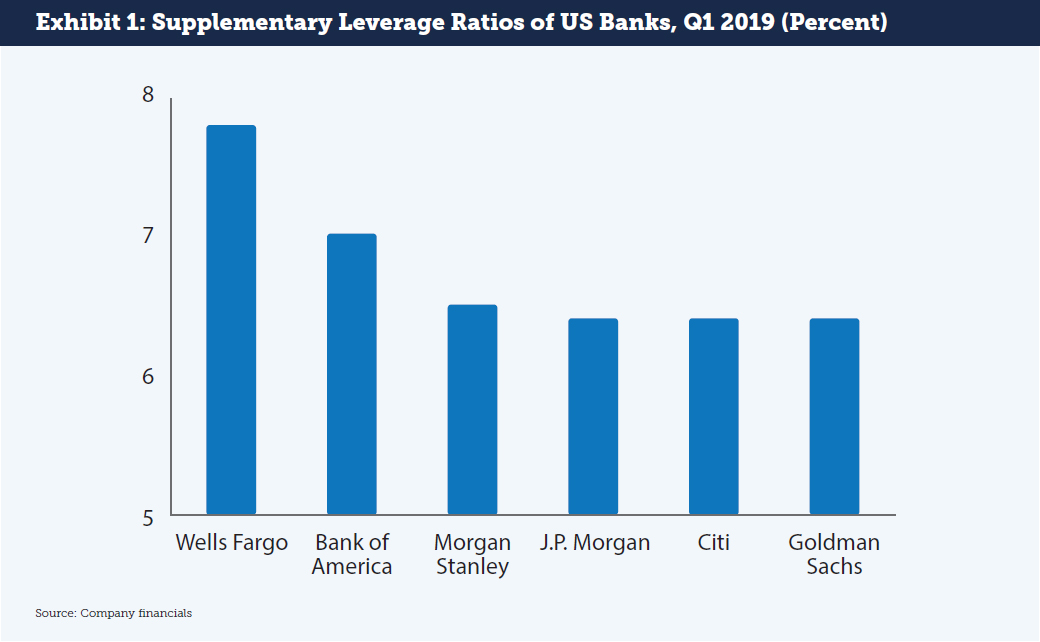

Strong bank balance sheets mean prime brokerage liquidity

An important dynamic in today’s prime brokerage market is that there is excess liquidity in the form of balance sheet that banks have been deploying in support of their prime brokerage activities, especially compared to the “tail exercise” periods of five years ago. Recent Supplementary Leverage Ratios (SLR) and Comprehensive Capital Analysis Reviews (CCAR) of major US banks show health across the board: across six leading US banks with prime brokerage operations, every one easily beats the 5% minimum SLR at the bank holding company level (see Exhibit 1). Every one of 18 banks tested in the 2018 CCAR passed, with only one requiring some additional review. The work of building up balance sheets and searching for High Quality Liquid Assets is largely complete: balance sheet assets are cleaned up and banks are positioned for growth going forward.

As a result of strong capital positions, there should be ample liquidity in US funding markets. Pricing competition between prime brokers is active, and banks are able to leverage their balance sheet flexibility as well as other internal efficiencies to provide a more compelling business proposition to gain additional market share. In addition, sophisticated bank resource management strategies have enabled prime brokers across the Street to maximize their inventory utilization, resulting in still lower costs. Both prime brokers and their clients are have become more sophisticated around the funding markets and values of internalization and hard-to-borrows. This has led to a buyer’s market for prime brokerage services.

Pricing dynamics in stock loan

Trends in US equity markets have impacted how hedge funds engage in securities finance. There has been a move away from directional shorts on single name assets towards more broad based ETFs or other sector strategies. In recent years hedge fund returns in traditional value oriented stock picking have not yielded the returns they have seen historically. There has been a number of factors that may have had an impact including quantitative easing deployed by Central Banks and foreign governments and the impact of quantitative strategies.

The current securities lending market has seen historical low percentages in non-General Collateral inventory utilization. This factor coupled with increased pricing transparency has resulted in more active re-pricing of non–GC collateral which at times has made it difficult for funds to be long-term holders in names given the pricing uncertainty. While a rate can start out reasonably, a belief that a name will turn into a highly contested short sale across multiple firms, leads to the expectation that rates will increase substantially. Inventory can disappear and market participants can use data tools to reprice quickly to maximize income. Generally, hedge funds know the rate they need in order to make a trade profitable based on their investment models. A low rate at the beginning that becomes a very high rate later creates additional costs which may lead a hedge fund to exit the position. Some funds are simply electing to stay out of the market when this type of directional trade seems to develop.

Given the factors mentioned above, hedge funds looking to short are often turning towards ETFs and other sector strategies that allow them to take a broad view of market movements. While there can be strong demand for an ETF in the short market, this does not translate into high stock loan pricing. When rates get too high, ETF marking making desks can step in and create more inventory, then redeem it later when the trade comes off. This keeps pricing stable for hedge fund borrowers by preventing a shortage of supply. While ETF-based shorting strategies offer value to hedge funds, these are commoditized and don’t provide some of the Hard-to Borrow revenue streams that have been historically important revenue streams for prime brokers. A commoditized market can drive volumes and enhance revenues, but these are not the types of transactions that sustain a broad prime brokerage franchise.

A combination of the lack of directional shorts and an increase in the lower value commoditized ETF trades has resulted in lower spreads for prime brokers in 2019. This has been mentioned as one reason for reduced equity sales and trading revenues in Q2 2019 over the prior year. A lower revenue environment plus ample bank liquidity means stiff competition for balances from both incumbents and newer entrants. At the same time, banks still need to meet their client profitability targets.

One possible outcome of a long-term narrowing of spreads will be the breakup of intangible services that large banks can provide, with each bundled offering now bringing its own costs. While this is not the way that neither banks nor hedge funds would like to conduct business, it may become necessary for banks to continue to justify the range of services that hedge funds expect, especially as they grow increasingly conscious of financing costs.

The view from Wells Fargo

Historically, the buildup of a prime brokerage franchise happened after the growth of the equities or fixed income division; banks were able to leverage their long-only businesses by introducing leverage to clients interested in short selling. This was a good idea for firms that already had large footprints with the traditional buy and hold market. “Selling the bank” is a well-known catchphrase.

At Wells Fargo, we are gaining ground in the other direction. We are starting with a significant prime brokerage operation and the opportunity to introduce clients to our equity, fixed income and derivatives desks. This is a version of selling the bank but in the reverse of the traditional pattern. As we build out this strategy, we must, like all banks, monitor the value of each client across the firm, but we are not forced to grow only in prime brokerage as a means of capturing market share. A hedge fund client that elects to do business with Wells Fargo outside of prime brokerage brings excess value that can be measured as a benefit and cost of the new desk relationship.

While the stock loan business is going through a phase of commoditization, we are taking the long view in building client relationships. Starting with our prime brokerage franchise, and even as client balances fluctuate due to cyclical forces, we are introducing clients to other ways that Wells Fargo can potentially add value in trade and balance sheet-linked activities. Continued balance sheet competition is to be expected in prime brokerage; the next phase of competition will be in growing the overall franchise accordingly.

Robert Sackett runs global securities lending at Wells Fargo Securities.

Robert Sackett runs global securities lending at Wells Fargo Securities.

Disclaimer

The Information is not intended to provide, and must not be relied on for, accounting, legal, regulatory, tax, business, financial or related advice or investment recommendations. You must consult with your own advisors as to the legal, regulatory, tax, business, financial, investment and other aspects of the Information.

Any opinions or estimates contained in the Materials represent the judgment of Wells Fargo Securities at this time, and are subject to change without notice. Interested parties are advised to contact Wells Fargo Securities for more information.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC, and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.