A broader adoption of electronic repo trading across the buy-side and sell-side is creating opportunities for greater integration, efficiency and automation on trading desks. While most interdealer and dealer-to-client (D2C) trading platforms are stand-alone and do not interact with one another, new functionality from MTS simply segregates the trading activity on a single platform. This allows not only for simplicity in technical implementation and integration for dealers but also the choice and control for certain data to be seamlessly shared between these dealers and their clients. A guest post from MTS.

Electronic repo trading has firmly established itself as part of the bedrock infrastructure of the markets. According to the ICMA ERCC December 2018 European repo survey, the share of business conducted on automatic repo systems hit 29.6%, a steady increase over the last several surveys. On the MTS Repo platform, we see the ERCC figures reflected in our own volumes. No repo desk on the sell-side would now go without one or multiple platforms, and buy-side firms are catching up as well. It is rapidly becoming the norm that all commoditized trades be conducted over an electronic platform, as anything else simply takes up too much time with little benefit.

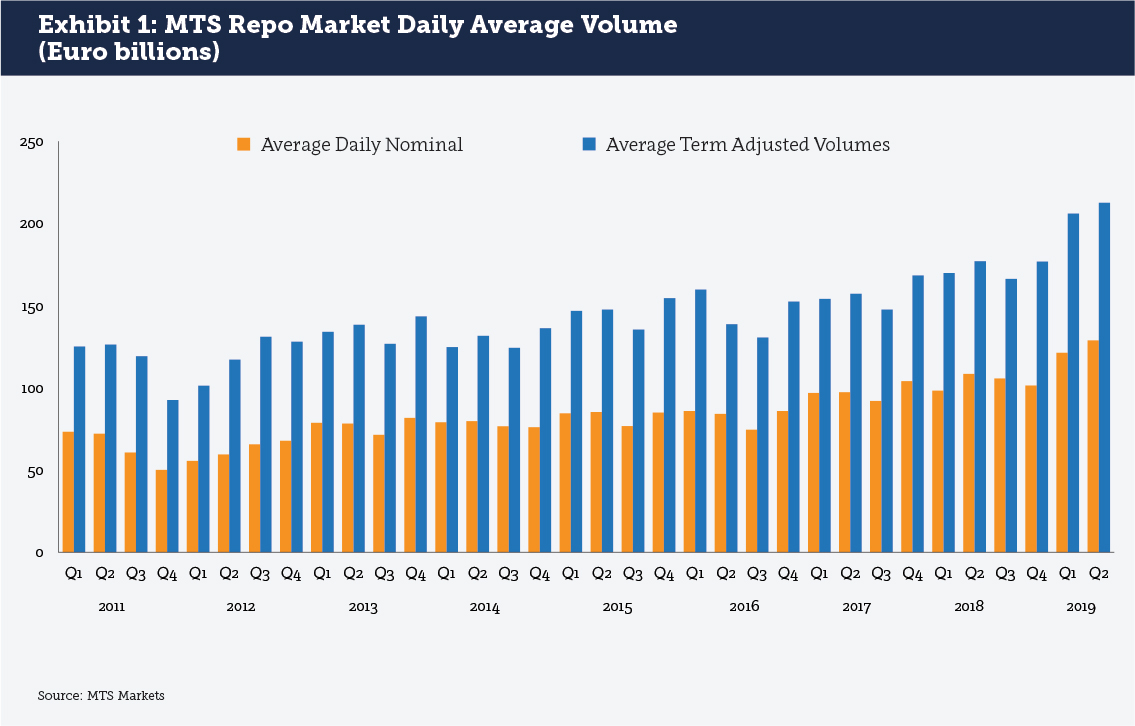

MTS first launched an interdealer electronic repo market over 20 years ago. At that time, the product was focused on helping dealers find matches to cover short positions in the outright cash bond market. But just as the repo product has evolved since then, so has the interdealer platform. The launch of MTS BondVision Repo in 2018 was another milestone; now, dealers could interact with their buy-side clients with as much efficiency as they were used to trading with their dealer peers. We have seen steady growth in the average daily notional volume on these repo markets, reaching €148 billion in July 2019 (see Exhibit 1).

While other interdealer and D2C repo platforms remain segregated, we are finding new ways to introduce automation across a single platform that leverages firm-specific data and trading preferences. Applying a straightforward rules-based approach allows both sell-side and buy-side firms to take advantage of new efficiencies such as axe sharing and price discovery that are driving capital markets as a whole. Better electronic repo markets, along with sponsored repo clearing and a further standardization of legal agreements, could result in a new sort of trading business model.

Data in repo markets

Unlike other markets that have already completed their process of automation, D2C repo trading is still in the first 30% of what could be accomplished. There is relatively little Straight-through Processing, and vendors have substantial opportunities to integrate electronic and manual information onto the same platforms. There is still much that needs to occur for repo markets to take advantage of available technology and more importantly, available data, and inroads are happening already. This next phase of market growth will be impactful, as data enters not just trading platforms but also downstream systems that generate pricing and liquidity requirements.

Repo has lacked the catalyst for greater electronification so far as the mandates of dealers, clients and regulators have not required it. The introduction of the Securities Financing Transactions Regulation (SFTR) in April 2020 will change all this; firms will need to turn to electronic markets to generate portions of the data fields necessary for submission; if the buy-side does not do this on their own, the sell-side may encourage platform use to facilitate reporting. Market trends suggest that electronic repo trading would grow without SFTR, but SFTR will speed up the process.

The aggregation of more trades, and hence more data, on electronic platforms will lead to a taming of the Wild West of repo.

Automation across interdealer and D2C platforms

As a natural progression of technology usage, we have observed how the volume of quotes in the interdealer market has grown significantly with the ability to automate the process.

Banks are willing and able to share entire inventories and short positions at the push of a button into the interdealer central limit order book. With the launch of BondVision Repo and platform integration at a central system level, dealers may now also share these very same quotes with their client community should they choose to do so. This enriches the relationship between dealer and client and assists the client in their pre-trade decisions.

Without the integration at platform level, this process would be more manual and technically complicated with little information shared. But when both sides of the market are connected by a common platform then barriers come down. Clients benefit from the axe data that otherwise would not be available to them, and dealers have control over which clients receive what information.

Dealers leveraging their quotes in the cleared interdealer market can mirror these prices to their clients based on rules-based preferences, and adjust the prices/sizes appropriately for each bilateral client relationship. This tailored pricing is a new functionality based on a single, separate platform. Dealers can advertise their interests better and wider and clients can achieve faster and better execution.

The benefit of automation is not limited to dealers; buy-side firms benefit by having much more granular information from their counterparties about what volumes are available, and pricing if that is revealed by the dealer. This speeds up the process of trade negotiation and lets buy-side trading desks feed back trade information into their own technology platforms.

What happens next

While we do not foresee a convergence to “All to All” repo trading in the immediate future, there are several innovations that are changing the market in important ways. First among them is the growth of the sponsored clearing model for repo. Buy-side firms can gain access to their counterparties while potentially taking up only a fraction of the dealer’s balance sheet compared to bilateral trades. This is having positive impacts on dealer business with both cash providers and Alternative Investment Funds looking to finance assets. A reduction in cost is already showing that the overall market has room to expand.

Another move forward is the standardization of legal agreements that make repo a more homogenous business. This does not mean All to All, but rather a continued ease of doing business between dealers and clients, as well as on electronic platforms.

Lastly, electronic trading generally means that more trading is possible. Smaller trades and trades with tighter spreads become more cost effective in an electronic environment. Adding automated settlement to tri-party agents and central securities depositories extends this value-add of electronic platforms.

While repo may never be as standardized as foreign exchange or equity trading, the potential for greater alignment across clients means that repo dealers could look at new business models that combine standardization and sponsored repo to further reduce internal costs. As one idea, a decade from now, repo could be something of a commission market where instead of a spread, dealers charge clients a fee for providing balance sheet or clearing sponsorship. The relationship and credit components of repo are important factors to consider and may never go away, but the platforms, infrastructure and business models used could see important shifts.

The benefits of an evolving repo market are very much for the buy-side. Buy-side firms can take advantage of automation and repo markets for more transparency, better and competitive pricing, and understanding volume and collateral trends. This in turn can lead to the creation of smarter technology on the buy-side trading desk across a range of cash investment and funding products in a cyclical loop. MTS Markets is helping to unlock these opportunities by providing better data tools across markets for the benefit of all participants.

About the Author

Tim Martins, Head of Product for Repo and Money Markets, MTS

Tim Martins, Head of Product for Repo and Money Markets, MTS

Tim has over 20 years’ experience in repo, including 11 years on the trading desk at Bank of America. During his five years at MTS, Tim has overseen the development and launch of BondVision Repo, a new dealer to client repo trading venue.