The buy-side has an opportunity to take control of its own collateral activity, bringing both financial and operational benefits. Breaking this process down shows that a robust collection of tools and services are available; buy-side firms do not have to go it alone.

For many years the esoteric world of securities finance existed inside of a well-crafted and well-oiled ecosystem where investors willingly ceded the responsibility of collateral and liquidity management to their custodian or asset manager for a fee in exchange for an enhanced yield on their portfolio. In the agent lender custodial model, the yield was enhanced further by agreeing to have the portfolio re-hypothecated for cash that was invested in higher yielding but safe and annex-prescribed, lower quality assets of which the agent lender kept part of the proceeds.

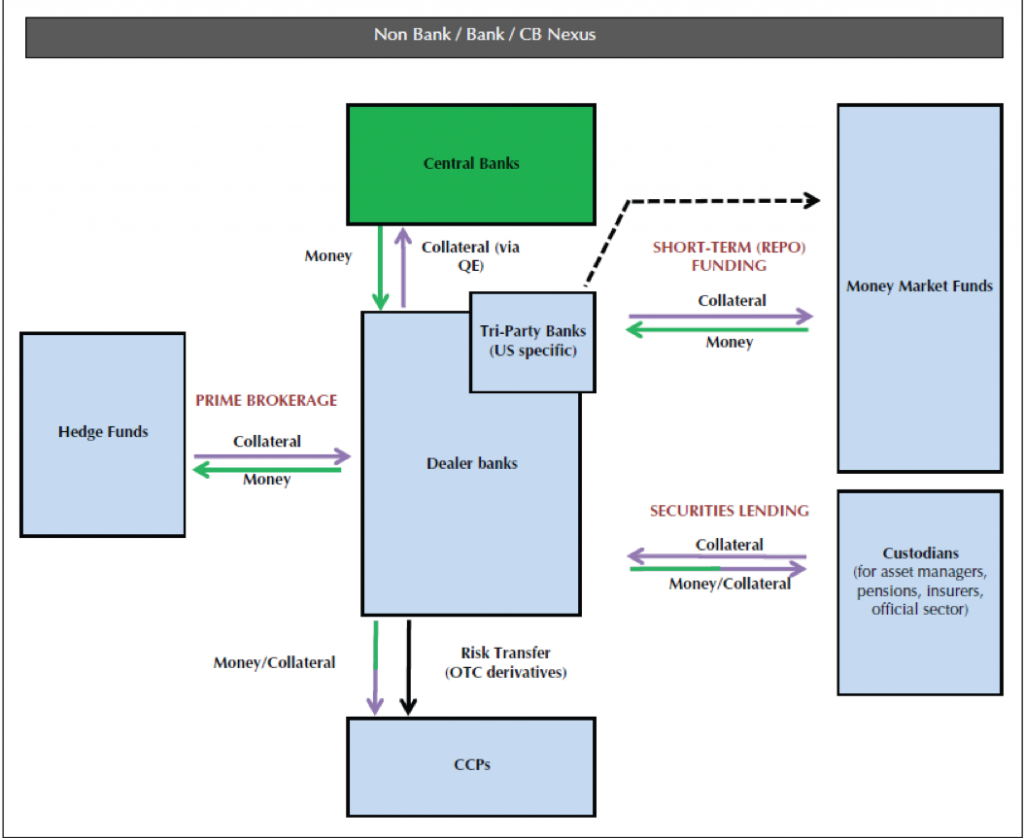

The re-hypothecation of those bonds was facilitated by the banks and assigned the “bank rate,” which was driven by Fed Funds or other benchmarks, with standardized haircuts at fairly static and well-understood spreads. Dealers could take the client’s collateral and repo that back out at the “market rate.” The accounts that captured the difference between the bank rate and market rate were known as matched books. This functional model was occasionally tweaked by central banks when reserves needed to be injected or withdrawn to keep those well-understood rates in balance (see Exhibit 1).

Exhibit 1: The Historical Non-bank, Bank and Central Bank Repo Framework

Source: Manmohan Singh, “Collateral and Financing Plumbing,” 2014

Source: Manmohan Singh, “Collateral and Financing Plumbing,” 2014

Going into 2017, this model is slowly going out of favour as the dealer community can no longer credit intermediate to the extent necessary to meet end-user demands. This impacts both pricing and availability for cash investors, and creates conditions where, for their own safety, the buy-side should take control of their own affairs.

A Breakdown in Money Markets, Repo and Collateral Utilization

Part of the value of the historical mechanism was that it clearly effectuated the transmission of monetary policy and utilized a full range of collateral across both securities lending and repo; this is no longer happening effectively. The markets rely more and more on central banks as they conduct financing operations to utilize the public balance sheet. The majority of High Quality Liquid Assets (HQLA,) the most sought after collateral, now sits idle in the portfolios of the buy-side, unable to be mobilized. Pricing in financial markets has been fractured by regulations and central bank activity, siphoning off buy-side cash. Tri-party reform, money market reform, Basel Committee/IOSCO rules for cleared and uncleared swaps and the lack of interoperability of BNY Mellon and J.P. Morgan in the DTCC’s GCF Repo space just add to the problem.

Regional trends have diverged on the impact of central banks on the repo market. Post the 2008 global financial crisis, ZIRP central bank policies, along with negative rates, and numerous episodes of QE, have caused the supply of excess reserves, now exceeding $4 trillion, to expand beyond central banks’ control. While US banks make a tidy sum on their Fed deposits ($6.9B in ’16) it has cost their European brethren dearly. Even negative returns on this excess cash cannot lure banks to make unprofitable loans that put further demands on their capital.

As noted in an article I wrote some months ago, banks have responded to regulation and market conditions by reducing the size of their net balance sheet to the tune of 80%, while netting 90% of their trades and culling their sizable account base severely.[1] They have reduced the amount of activity with the money market funds at precisely the time when money funds have produced an even larger surfeit of cash. This has led banks to widen repo spreads on what is essentially the same basket of securities, predicated on where the funds sit and which customer is asking for the marginal usage of the bank’s balance sheet. This now takes place routinely based on client profitability and importance.

Banks are also working closely with CCPs to create a bank to non-bank financing solution. Clearly there is a place for that kind of platform in the finance arena but it’s not at all certain to me that the buy-side gets either best price and execution, while it is taking on the increasing risk associated with another market liquidity hiccup. Banks are quickly coming to the realization that the spreads they’ve worked so hard to widen, to improve profitability, are in danger of compressing significantly should large liquidity providers get access to their once guarded CCPs. Additionally, the buy-side is still price takers in this sponsored agent model (how else for banks to get paid?) and banks get to have their cake and eat it too in the form of more netting opportunities. That said, unlike an all-to-all solution, these CCPs all have restrictive membership requirements and banks will continue to pony up large amounts of capital in the form of haircuts and increased default funds.

The Change Has Come

There was an interesting development at a recent conference where the opening panel consisted of a hedge fund, a representative from Elixium and an agent lender. This is the first time in recent memory that this complement of panelists gathered, and there was an active discussion afterwards by buy-side only participants about alternatives to the bank repo or securities lending model, typically called Direct or Peer to Peer (P2P) lending. Normally that kind of panel would be scheduled for the last slot on the last day of the conference cloaked in some title like “the future of securities lending,” while people were checking out of the hotel and catching their flights home. Clearly, the future is now.

P2P lending has been taking place for the better part of the last decade, but current estimated volumes are just 3% of the global repo and securities lending market. A move towards P2P will require the buy-side to be able to safely and efficiently mobilize their collateral, at best price and execution, with all the transparency an electronic trading platform accords them. Signed legal agreements governing the transactions at pre-set and monitored credit lines, inside of client-defined risk parameters, should provide the buy-side with the same level of comfort they assume today. The liquidity of the underlying, the credit-worthiness of the counterpart and a standardized haircut all remain the same.

In order for this to happen on a functional basis, the buy-side needs to take a greater degree of responsibility for their own financing than they do today. This may seem daunting at first, but breaking the process down helps as well as realizing you do not have to go it alone. Even with outside trade support, there are several other factors that the buy-side needs to consider:

- Order management systems along with collateral and liquidity management and optimization vendors are everywhere these days. Most of them are good; some are exceptional.

- The mining and harmonizing of data, while creating position dashboard to facilitate mobilizing cash and collateral quickly is essential

- Digitizing CSAs to optimize collateral is also a must.

- Plugging into post trade hubs to help navigate your cash and collateral and direct it to the proper clearing and settlement agent or triparty provider takes the pain out of post trade.

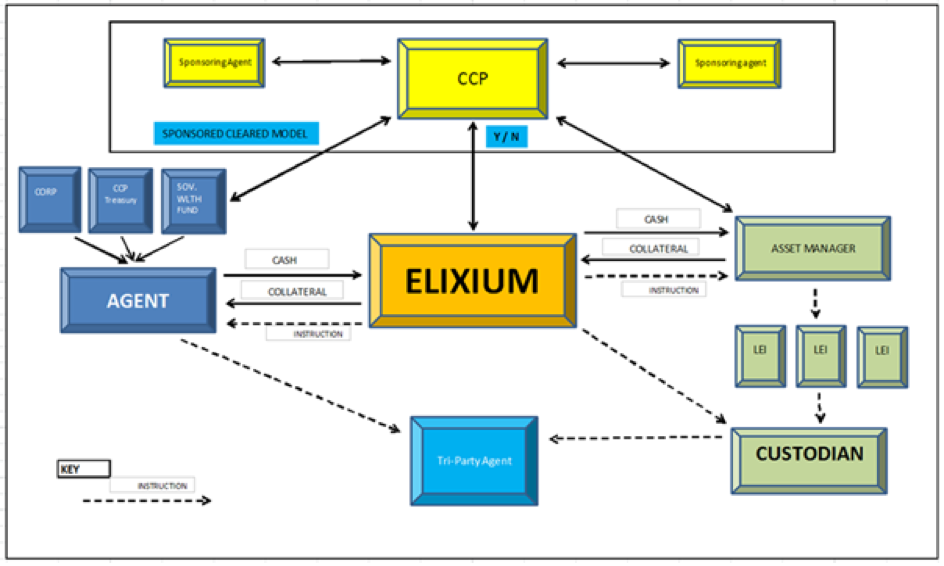

At Elixium, we provide the trading platform that gives the buy-side access and transparency to repo funding at market prices instead of bank prices (see Exhibit 2.) We also feed the systems that enable effective data reporting and trade management. The big change here is that the buy-side can move from being price takers to being price makers, a fact that has increasing relevance in the age of MiFID II best execution compliance. For the buy-side, taking control of collateral trading is a one-time only fix that pays for itself in no time.

Exhibit 2: The Elixium Solution

Source: Elixium

Market participants are at an inflection point. Bank profitability, driven in large part by passing on their regulatory cost to the buy-side, is beginning to increase; banks have made the adjustments necessary to meet their return hurdles. The buy-side now has a choice whether to pay for increased regulatory costs through wider repo spreads with less access to bank balance sheets, or take control of their own collateral activities including a move towards P2P. The tools exist for the buy-side to reduce or remove their dependency on the banking system and enhance their profitability. Owning the process front to back is the way to achieve this.

Stephen Malekian is Head of Business Development – US for Elixium.

He has over 35 years of experience in the global financing markets, having run Global Fixed Income Finance and Prime Services at Citi and European and Asian Fixed Income Finance at Barclays. Steve has been Chairman of SIFMA’s Executive Committee of their Funding Division, member of the New York Federal Reserve Task Force on Triparty Reform, as well as a member of the European Repo Council and the LCH Risk Committee.

This is a guest post from Elixium.

[1] “Bank repo spreads are widening, but do clients have to pay the bill? Here is the Elixium alternative,” Stephen Malekian, Securities Finance Monitor, January 12, 2017, available at http://finadium.com/bank-repo-spreads-are-widening-but-do-clients-have-to-pay-the-bill-here-is-the-elixium-alternative/