This post continued our thoughts on what has happened to the collateral transformation trade, including available data on US Treasuries on loan in 2013.

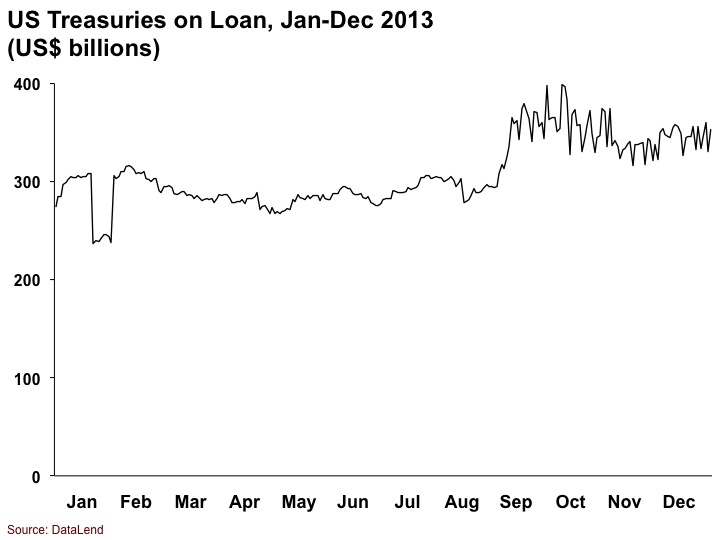

Under Dodd Frank, the US was the first to implement mandatory clearing. The first category of market participants, swap dealers, major swap participants and active funds were required to margin trades on an exchange beginning in March. This was followed by a second tier: commodity pools, non-active funds and entities primarily engaged in banking in June and all other participants including ERISA funds in September. With each successive role out the repo market expected a pickup in demand and with each successive role out the market was disappointed. The attached graph from DataLend shows only a modest pickup in US treasuries borrowed over the course of 2013. This is re-enforced by the Fed’s dealer surveys which show a decline in repo balance over the course of 2013 from $5 trillion to $4.5 trillion. So what happened? Why are we not seeing a pickup in demand for HQLA?

The assumption upon which this anticipated demand was based was that there are a large number of investors which hold exclusively non-liquid assets; equities, corporate, etc. These institutions would have to find a mechanism to exchange these non-liquid assets for liquid (eligible) assets to pledge on an exchange. For this reason, the market came to accept the need for collateral transformation on an industrial scale in order to source initial margin and for the repo-ing of non-liquid assets for cash to source variation margin. It was believed that these participants would not sacrifice yield by holding liquid assets or cash in their portfolios.

But there are a number of factors which may explain this lack of incremental demand. First, dealers by their nature hold a diverse spectrum of assets. With the pressure on them to shrink their balance sheets and conserve capital it does not make sense for them to take on incremental collateral transformation trades when they can simply optimize the collateral they already hold across the institution to fulfill all of their collateral requirements. As for other market participants, the answer is somewhat more complicated.

First of all, we see no significant effort on the part of market participants to migrate existing derivative trades to an exchange. In order to do this the parties would have to re-negotiate each collateral support agreement (CSA); a daunting task. Banks and dealers would be happy to novate trades to get them off the balance sheet but clients aren’t too interested. So therefore what we have is only the transactions which have occurred since mandatory clearing went into effect last year. Longer dated swaps and similar transactions are not necessarily trades which institutional investors enter in to every day. They are planned as part of the periodic rebalancing of portfolios and negotiated over a considerable period of time. Hence, it will take some time before we see the effects of these trades.

Another factor is that there are alternatives to derivative trades. Futures or options can be used in a portfolio strategy as an alternative to swaps or bonds can be purchased to gain duration. And, despite the belief to the contrary, these portfolios of non-liquid assets may contain some quantity of liquid assets or cash which at least initially can satisfy the margin requirements of derivative trades.

But there may be another explanation, one which is related to the current state of the global securities lending and repo markets: in the current regulatory environment the financing markets may not be relied upon to provide the collateral necessary to support derivatives trading. Consider the position of a portfolio manager who needs to enter into a 30 year interest rate swap. He needs to know with certainty that he will have access to HQLA over the entire term of that swap to provide initial margin and at any point in time he needs to know that he can source cash to provide variation margin on an extremely short term basis. Faced with this uncertainty, he may view the loss in return associated with holding cash or liquid securities in his portfolio as a necessary cost and therefore avoid a long term reliance? on securities loans or repo to provide him with the collateral he may need.

We’ve always been a little dubious about the success of the collateral transformation trade. As we wrote in a December 2012 research report on the collateral transformation trade: “Across the market, we expect that banks will need to pay substantially more to encourage cash providers and beneficial asset owners to increase their supply levels. We are much less concerned about a build-up of collateral transformations leading to systematic risk than we are the ability of the market to generate that same build-up in the first place.” We’re not ready to call the collateral transformation trade down and out yet, but so far the growth is much slower than what market observers, including ourselves, thought at the onset.