Stock borrowing is an inherent element of any leveraged equities trading strategy. Whether the trade is as simple as a traditional short or as complex as a long hedge against a short sector or ETF play, it will likely involve the borrowing of securities. This is true for both regular physical short sales and derivatives strategies that bake in the financing cost.

In today’s market, the cost of financing is actively debated by market participants and is driven by balance sheet availability, supply and demand of the security in question, and value of the client to the firm. In physical financing, this is easy to identify: stock borrow costs can vary depending on the size and importance of the client, and always factor in the bank’s capital exposure. This aspect of stock loan trading must be considered when interpreting historical data. In derivatives trading the situation is a bit more complex. There is still a financing cost but in options it is implied in put-call parity and expressed in the bid-offer spread. There is not a single bank to client relationship at play, rather a market making desk will offer a quote based on the cost of the underlying, the risk involved and, again, the balance sheet.

The cost of securities financing is a direct economic risk of any physical or equity derivatives trading strategy. Rate structures and forward rates exist in nearly every corner of financial markets and provide valuable transparency about the current state of the market and future expectations. In contrast, forward rates for financing costs remain elusive; managers who can capture and analyze these costs will have an inherent advantage over their competitors in risk management and portfolio execution.

Robust market data for short-term needs

The landscape for securities finance data, both historical and real time, is becoming more populated. Services like FIS’ Astec Analytics, Equilend’s Datalend and IHS Markit’s data suite collect, aggregate, analyze and publish global borrowing fees, encompassing equities and fixed income. Every market participant willing to write a check has transparency into what was once a very opaque and proprietary world. Further, several brokers provide at least General Collateral, easy to borrow rates on their website with no charge.

The data tools available to brokers and investors today are based on trailing indicators and self-reporting after the trade. They answer one principal concern: what was the last transaction fee, often from the previous trading day. Knowing this is powerful: a securities lending trader, portfolio accountant, short term trader or high frequency trader can have a good sense of their trading costs prior to hitting the buy or sell order, and can compare historical rates for fairness across multiple brokers. This is valuable for short term trading activity, hence the growth of the finance data space.

In addition, there are sources of data for options-based implied borrow data. Vendor sources usually only provide it for non-dividend paying stocks because of the complexity of modeling around discrete dividend payments, and because the required dividend forecast data is quite valuable in its own right. Some of these sources are high quality, such as the implied borrow rate displayed on Bloomberg option screens (e.g. OMON) even despite the limited coverage universe. Such screens provide one data point for each expiry at the current moment in time. For most names the dynamic range of bid-ask spreads, which is typically very noisy, makes these measures difficult to follow and not that informative at any one point in time. Some names routinely appear too easy or too hard-to-borrow on an implied basis and it requires more context to discern a signal from option derived financing rates.

New methodology for a securities finance rate curve: the Hanweck Borrow Intensity Indicator

The missing piece of the securities finance data puzzle is leading and term-rate information on borrowing or financing costs. To manage risk and make informed decisions, long term traders need to know what rates look like 30, 60, 180 or even 360 days into the future. There are no commercial data sources that provide this currently; data from securities finance vendors tend to be backward looking. This makes equity finance costs more difficult to manage on an informed basis compared to cash funding where there are transparent rates for OIS or US Treasuries, which have easily observed curves. Moreover, with only the overnight rebate rate in a daily historical series, it is difficult to know whether a recent reported level was simply an outlier – maybe noise, or just a function of the counterparties engaged in some major reported trades – or the start of a new rate regime for a security.

In response, we have created a new indicator based on what we call borrowing intensity. The Hanweck Borrow Intensity Indicator presents financing rates outwards based on the observed balance sheet costs of banks as presented in listed derivatives. This rich data structure enables trends to be more readily discerned, and acts as a basis for forming better predictions of future trends in overnight rebates and term financing rates. One can examine relative changes across different Borrow Intensity terms to corroborate or question the significance of a change in a single maturity. Borrow Intensity history can even be used to help clean overnight data collected directly, or from vendors.

We continuously mine “raw” real time implied borrow data comprehensively across thousands of equity options series, and then transform it with machine learning to generate maturity weighted views of stock borrow fees and term curves available throughout the trading day. Our Borrow Intensity Indicators are generated using a proprietary process that further modifies implied borrow calculations to create a time-series with constant maturity characteristics.

Predictive analytic screens automatically alert users to rising or easing borrow conditions and detect major movers intraday. Indicators are constructed from weighted observations across the entire volatility term structure, providing a constant-maturity view across time. This includes a historical data set and a means of observing intraday departures from historical patterns.

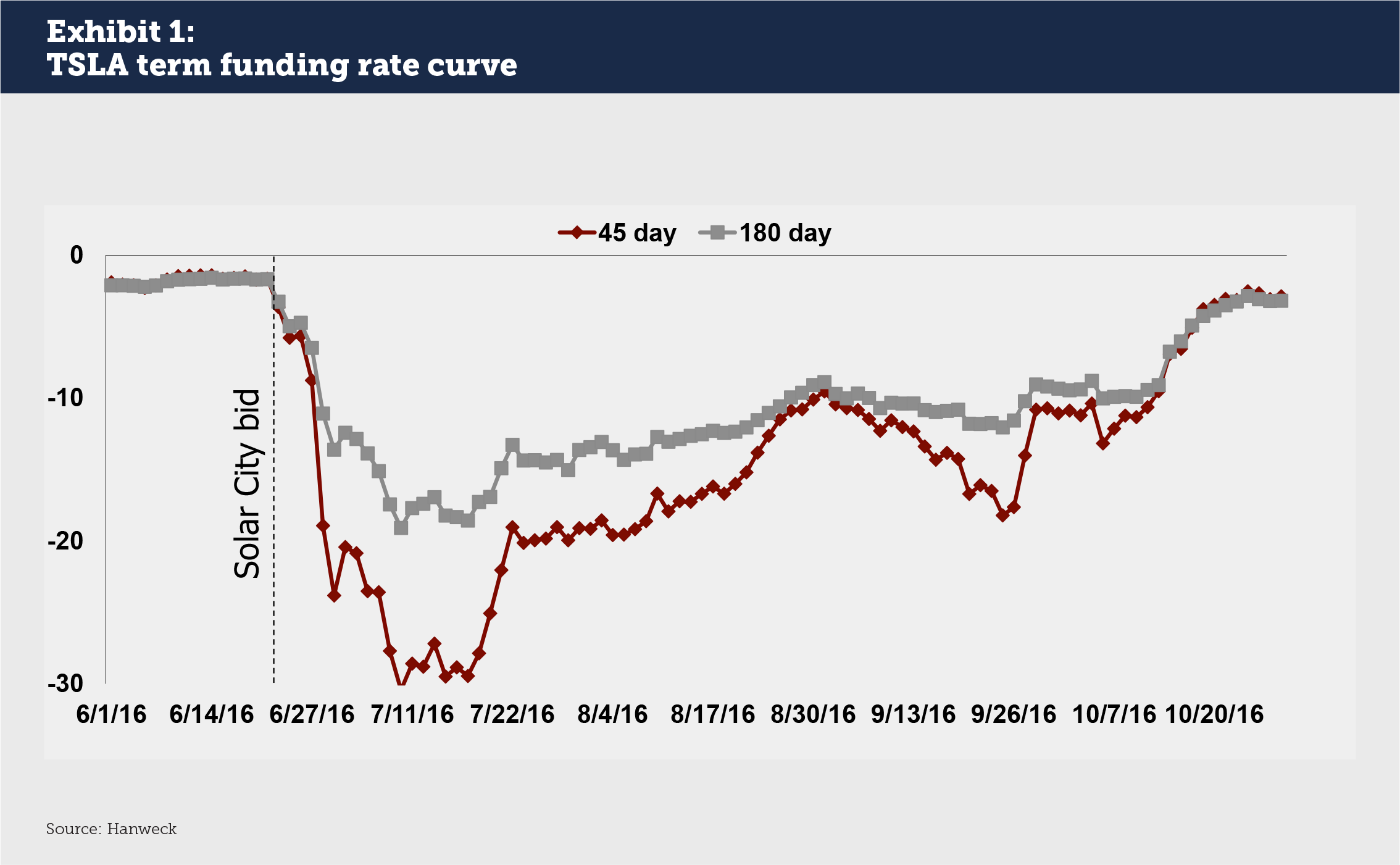

As an example of the term curve that we observe from the data, the funding rate for Tesla (TSLA) on a 45- and 60-day period varied by 12% shortly following the Tesla bid for Solar City (see Exhibit 1). This divergence eased over the course of the next three months, but for an investor shorting or buying put options on Tesla in early July 2016, a known difference of 12% could be factored in to the expected profitability of the trade.

We leverage a related product, Hanweck Option Analytics, for continuous insight into reverse-conversion rates for every listed option expiry. These data include the cost of crossing bid-ask spreads in the options market, and offer comparative views of full American model vs. European model assumptions to highlight the impact of early exercise risk.

As noted above, we are not the first company to pull out implied financing rates from options prices: this is old news. The new capability is the massively parallel processing and statistical learning that Hanweck uses to create both history and real time updates that provide consistent views one can follow across time and into the future. This is then readily consumable for applications ranging from securities financing to automated trading strategies and market making (e.g. risk aversion parameters).

Over 4,000 of the most actively traded securities are covered in our model, which is nearly the entire universe of US equity securities with listed options and 80% of the 5,200 US equities listed on the NYSE and Nasdaq. Although this is a small sample compared to the 60,000 securities that could potentially be financed, industry experts estimate that it covers approximately 75% of the names most actively traded in the securities financing market where professional investors concentrate their interest.

Implications of an equity funding rate

The creation of a term funding rate for specific equity issues opens up new possibilities in securities finance and derivatives trading. The most obvious is the robust creation of cost projections and better risk management for existing or theoretical portfolios. Unknown borrowing costs are a risk in any trading strategy; we want to mitigate this risk through transparent data delivery and a view into market expectations of borrow intensity.

Our real time feed integrates with algorithmic trading systems as a new indicator for making trading decisions. For example, if a stock with a large short base pre-earnings (indicating negative market expectations) is becoming easier to borrow according to our data, this could be a signal that market expectations are incorrect and could present an opportunity for alpha generation. By providing visibility into term borrow expectations, the Hanweck Borrow Intensity Indicator can reveal market dislocations.

Looking forward, we see potential indices that could be created, for example term funding rates for baskets of securities such as constituents of sector ETFs. Such indices would be informative, and could even be realized in listed or OTC derivatives that would allow hedging of funding costs.

Having created the Hanweck Borrow Intensity Indicator, we now turn to the market for conversation. We expect to find new ways of thinking about financing rates based on this information and look forward to further iterations of our Indicator based on market demand.

Bob Levy leads business development activities at Hanweck, with responsibility for expanding the reach and scope of Hanweck’s products in the financial industry, and developing new product lines in risk and signal analytics. He joined Hanweck in 2012 from Merrill Lynch where he headed Portfolio Risk Analytics in New York for six years. He helped found MarketAxess, where he developed electronic trading businesses in fixed income credit and rates products. Mr. Levy has held a number of senior positions in sell-side firms, including running fixed income arbitrage desks. He began his financial career at J.P. Morgan where he traded US Treasuries and rates derivatives for eight years. Mr. Levy holds an MBA in Finance from the University of Chicago, and a BES in Electrical Engineering from The Johns Hopkins University.