A recent survey of asset managers in securities lending showed that executives were interested in CCPs but lacked the information necessary to create a cost/benefit analysis and build their business cases. Part of this business case relies on data from a functional CCP, but other parts require an understanding of the main components. This article provides key points and a methodology for creating this analysis.

The two big theoretical arguments for the buy-side to participate on securities lending CCPs are improved pricing and greater utilization of their securities. Simply put, if the pricing is better on a CCP then why not participate? Finding the answer to pricing may be no further than asking a borrower already using the CCP for a bilateral quote and a CCP quote. If the borrower can offer a more favourable price for one or many securities loans via the CCP, then this can be extrapolated to a portfolio across general collateral and hard to borrow securities. This has already been seen in OTC derivatives markets, with dealers offering a basis between the same trade whether cleared or uncleared. In securities lending, it is expected that similar pricing will occur in time. Borrowers will benefit from capital efficient clearing models for securities finance transactions as well as straight-through processing efficiencies; some or all of this can be passed through to the lender as price improvement on the CCP.

The utilization question is harder to resolve without empirical data. Can loans be outstanding for a greater duration on a CCP just because of the improved balance sheet conditions? One single borrower is unlikely to provide an answer since they need a loan for their own purposes only. Arguably however, if the CCP transaction cost is lower than the bilateral cost, and if that cost is passed on to clients, then borrowers should be more inclined to borrow for longer periods than with a bilateral loan.

The CCP may also accept a greater diversity of borrowers leading to a larger pool of potential distribution for the buy-side. Buy-side managers may see this as both a positive and a negative. On the plus side, more participants mean more opportunities to make a loan. The negative might be that a buy-side firm would interact with a borrower that would not otherwise meet their credit criteria. In the Eurex Clearing Lending CCP model, asset managers can still pick their own lending counterparties before trades are sent to the CCP. The CCP gives the option, but not the requirement, to expand the range of potential borrowers.

Asset managers using an agent lender typically outsource the credit analysis function of counterparty selection to their agent lenders along with determinations on collateral acceptance and risk. As a counterparty, the CCP’s risk is increasingly well known and Eurex Clearing’s Lending CCP has a clearly defined model for accepting in the buy-side. The Lending CCP requires neither a default fund contribution nor margin, and offers a transparent plan for resolving any potential borrower defaults without compromising the risk management standards, stability and integrity of the CCP.

The criteria for a buy-side evaluation of securities lending CCPs is much simpler than for the sell-side. Taking out the cost of capital and risk-weighting of CCPs makes the conversation much easier. However, both the buy-side and sell-side still need improved analytics to ensure that their CCP transactions are optimal relative to actual or hypothetical bilateral transactions. Eurex Clearing’s Lending CCP will provide a portion of this information, while data vendors including Pirum will provide the rest. These are not pre-set calculations however and buy-side firms should be prepared to create methodologies that best suit their needs.

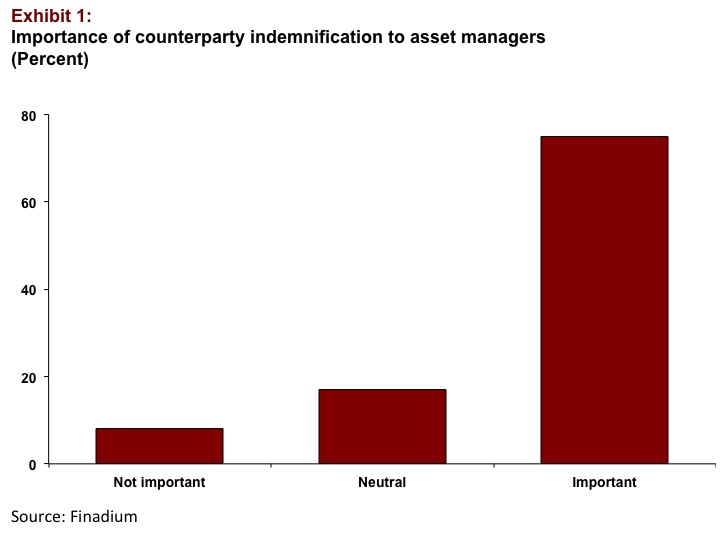

While the buy-side receives no capital relief for their CCP transactions, agent lenders and their borrowers do, and this is expected to help mitigate the cost of indemnification. Finadium’s July 2015 survey of asset managers found that indemnification remains a very important offering, even if managers recognize at the same time that collateral is the first line of defence in any default scenario. In addition, 75% of managers reported that indemnification was important or very important to their securities lending activities (see Exhibit 1).

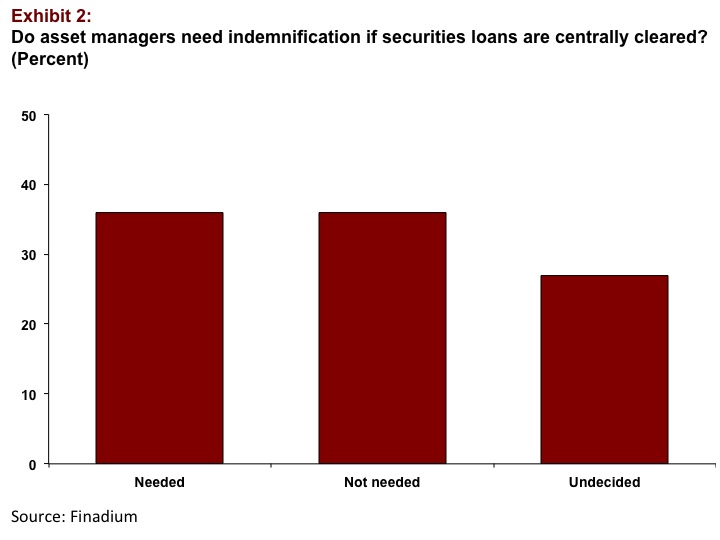

Some asset managers want to keep counterparty default indemnification from agent lenders even in a CCP environment. Finadium’s data show that 36% of managers believe that indemnification will be required with or without CCPs; 27% remain undecided (see Exhibit 2). This plan works for agents too; counterparty default indemnification on a bilateral basis may be expensive, but conversations with agent lenders suggest that a CCP counterparty will use less capital for indemnification than a bank borrower. Another option will be for agent lenders to forego indemnification and rely instead on the CCP’s default fund, in a form of “CCP-based indemnification.”

Another benefit of the Lending CCP that has not yet been widely explored is cross-product trading and netting: having both repo and lending on one CCP offers additional netting opportunities from a RWA, balance sheet and leverage ratio perspective. There are also re-use possibilities across lending, repo and collateral for OTC derivatives. The more business that a buy-side firm does on Eurex Repo and Eurex Clearing across products, the greater the possibilities for their securities lending borrowers, repo collateral providers and futures clearers to net down their own margin and balance sheet exposure. This is a subtle change in the markets but one that may grow in importance as Basel III and regional regulations become more firmly entrenched in the markets. Any cost benefits to the buy-side may not be quantifiable at first but should be considered as part of a business case strategy.

Once the business case is in place, Eurex Clearing’s Lending CCP and its connected Flow Providers and Tri-party Agents are currently working to make onboarding and the automation process as easy as possible. Pirum reports that agent lenders are engaged and are comfortable with Pirum’s technology and process. Their CCP Gateway provides a process where setting up and going live are seen as straight-forward activities. Similarly, Eurex Repo is actively upgrading its users to become participants to the new Eurex Repo-SecLend Market F7 trading system that was successfully implemented earlier this year. Eurex Clearing is working on how UCITS funds can hold assets so as not to violate their pledge agreements. This is a vital operational activity for UCITS funds to successfully use the Lending CCP under ERISA rules. Eurex Clearing is already working with major agent lenders and prime brokers including State Street, BNY Mellon and Morgan Stanley to implement CCP operations for the buy-side.

In some ways building a buy-side business case is a chicken-and-egg problem, where the CCP needs liquidity to show the buy-side that pricing and utilization is better than in today’s bilateral transaction. Gaining a full dataset will take some time and will be earned from the steady adoption of both lenders and borrowers on a CCP platform. This is happening however, and may lead to a situation where first movers have an advantage over latecomers in understanding the dynamics of the CCP operating model.

This article was authored by Gerard Denham and Jonathan Lombardo, Eurex Clearing