About a month ago we looked that National Futures Association published data on required collateral for cleared derivatives. We were pretty surprised how small the numbers were. We have a couple more data points and wanted to take another look.

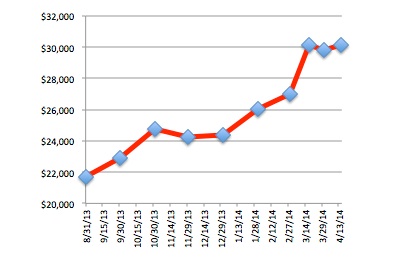

Not a lot has changed. Total required collateral for cleared derivatives clocked in at $30.151 billion as of mid-April, 2014, the latest numbers available, virtually unchanged from the last figures we observed on March 17, 2014 ($30.110 bio). Total collateral held (which represents required and excess collateral) by FCMs for cleared derivatives came in at $35.570 bio., a touch above mid-March numbers of $34.994 bio.

Required Reserves on Cleared Derivatives Trades

In billions, source: http://www.nfa.futures.org/basicnet/

Versus the trillions of dollars of collateral projected by some to be required going forward, the market seems to be getting off to a very slow start – if cleared derivatives required collateral is a decent indicator of collateral demand. We still maintain that collateral demands will go up, but that this will take a long time. Derivatives books have to turn over, a process that won’t be quick (although it can be hastened by rising interest rates).

Looking from the repo and sec lending point of view, cash needs to be a less attractive asset to throw at the problem before securities lending markets will see a material pick up in demand for collateral transformation and other collateral optimization related products.

There are some other matters that will need to play out. On April 21st, we wrote a post “Segregation of initial margin: buy side elections are coming soon. Will it impact swaps pricing?” looking at how collateral segregation on non-cleared swaps might impact the markets. If segregation means that cash and securities held as collateral can no longer offset funding costs, then pricing will change. This may push some buy side clients into the cleared derivatives markets, although not necessarily with great enthusiasm. If and when the capital police come out in force, allocating capital down to the derivatives business line, novation of trades to CCPs will become more urgent, increasing the required collateral held.

As of mid-April, the largest 5 dealers accounted for 81% of the required collateral held. This was identical to the percentage of total collateral held.

|

Required Cleared |

||

|

Derivatives Margin |

||

| Credit Suisse |

18% |

|

| Barclays Capital Inc. |

17% |

|

| Citibank |

15% |

|

| Morgan Stanley & Co LLC |

13% |

|

| JPM Securities LLC |

11% |

|

| Goldman Sachs & Co |

7% |

|

Source: http://www.nfa.futures.org/basicnet/

The Credit Suisse number was a little surprising, on the high side. Looking at other market share numbers – for example the Underwriter League Tables for Corporate Bond (All) where according to Bloomberg CS has 3% market share, the 18% number stands out. Bank of America Merrill Lynch didn’t make it into the top 80% in collateral held on cleared derivatives (they were 7th at 5% market share). Deutsche Bank, long seen as a derivatives trading power house, also didn’t make it into the top tier, with 4% market share of required collateral.

One possible reason for the low numbers published by the NFA could be the realignment of derivatives businesses to offshore entities. A May 2, 2014 article in the Nw York Times “Wall Street Embraces a Rule It Hates” about the Dodd-Frank swaps push-out rule may have some clues. The article said

“…banks have started to shift substantial amounts of derivatives trades into offshore affiliates that the parent banks do not guarantee…”

and

“…So why are the banks doing this? In short, they are trying to avoid other derivatives regulations that are unrelated to the push-out rule….Specifically, the banks want to reduce the impact of new rules, also part of Dodd-Frank, that aim to improve pricing transparency in the derivatives markets…”

These market share disconnects can also be attributed to business model. Just because a bank wants to be a major player in derivatives trading doesn’t mean they want equally high market share on the FCM side, and visa-versa. The days of being all things to all people have receded. Buy side clients still focus their clearing on a small number of FCMs, often with one primary and one back-up. Will being a client’s FCM of choice give a leg up on getting the derivatives flow? Time will tell.