We came across some interesting data that presents some subtle revenues dynamics at play in the securities lending market. The issue at hand has to do with cash vs. non-cash collateral, what drives demand and how agent lenders are generating profits.

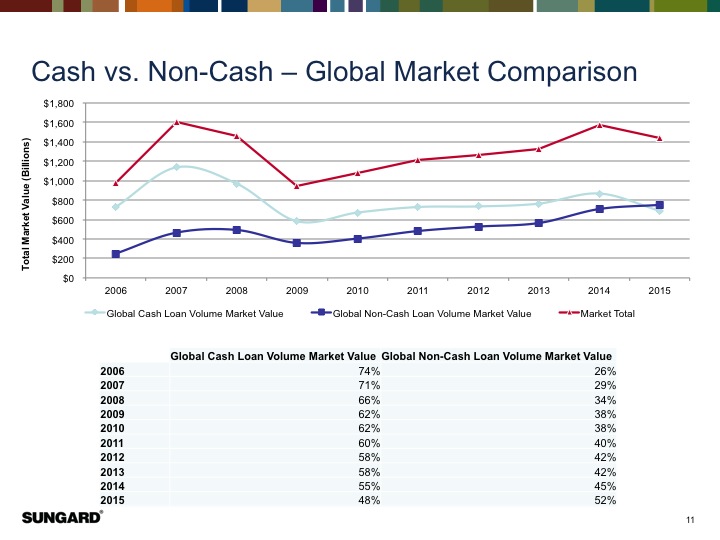

The data are courtesy of SunGard’s Astec Analytics and show that while non-cash collateral volumes are rising, the percentage of revenues coming from cash are still much higher. Why should that be, if more non-cash loans are going out the door? Here’s the SunGard graph on cash vs. non-cash, which show non-cash at 52% of the market. This is up from 26% in 2006, a solid doubling of volumes.

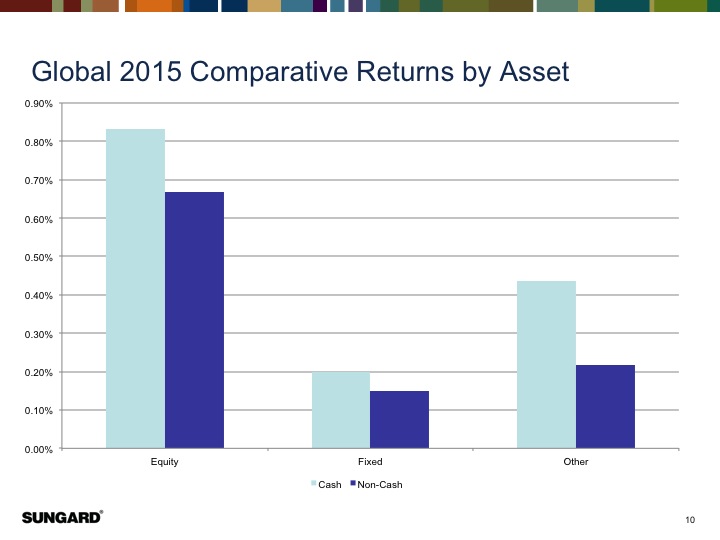

Meanwhile, here’s the graph on cash vs. non-cash revenues in securities lending on a global basis. Let’s keep in mind that this number is pretty US-centric given the size of the US market, but even so is a global figure.

So why are cash revenues greater than non-cash when non-cash is over 50% of outstanding loans? The answer is in demand for harder to borrow securities. When demand is weak, borrowers are able to post a greater amount of non-cash. Another way to say this is that non-cash is more prevalent for GC loans than specials. Meanwhile, in the large US market, when demand is hot then lenders can ask for and get cash. The returns on these specials trades against cash, although smaller in number, more than outstrip revenues from the GC non-cash business.

This trading pattern is a sign of the times. We expect more twists and turns to come.