Following the crisis, high volume, low margin businesses like repo were unable to meet the return hurdles on a bank’s cost of long term capital, forcing a change in their business models. Since capital goes where it’s treated best, banks responded as one might expect and began resizing their businesses to return them to profitability. This is a guest post from Elixium.

Repo desks in particular are recovering through a combination of aggressive balance sheet management and passing on increased regulatory costs to small- and medium-sized clients. No one begrudges the banks widening spreads to meet these return hurdles, but what’s less clear is why the buy-side needs to pay for it.

At Elixium, we have created a trading platform that repositions the conversation away from bank spreads towards a transparent marketplace. Our new model solves real-world pricing and repo access problems for investors and intermediators.

Although bank net balance sheets have come down 80% across the entire spectrum of fixed income, make no mistake, these businesses are still generating substantial revenues. The challenges to executing business model changes in the face of Basel III, Dodd-Frank, CRD IV and similar regulations have mostly been met, and many banks have succeeded in returning to profitability. The process is not yet complete, however, as equity markets indicate.

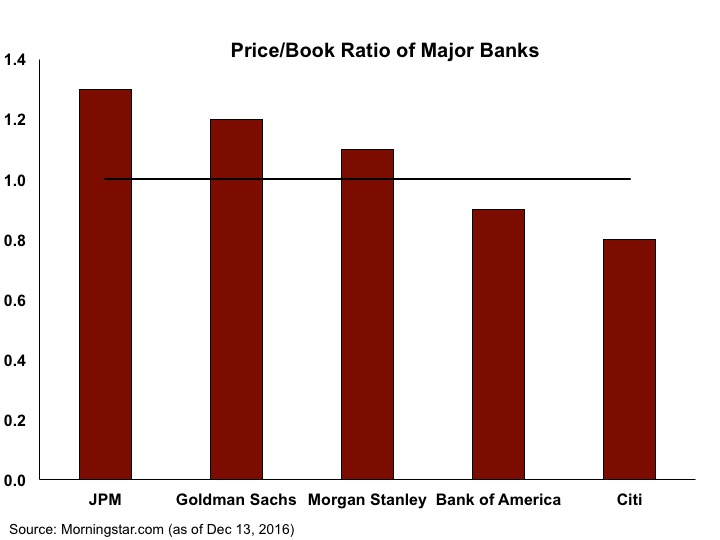

In spite of progress, the equity markets recognize that big banks still have work to do: major banks are trading close to or significantly below their price to book value, meaning that the market thinks that management has little chance of improving the profitability of their assets beyond what the actual price of those assets are today (see Exhibit 1). And in the case of Bank of America and Citi, the expected break-up value of these banks is more than the value of the assets they hold. Put another way, the market thinks that the value of these banks is going to decline. While there are many variables that go into a bank’s equity valuation, the fact that the price to book ratios are close to or below zero is a telling sign that their revenue model is hampered by the types of business they can do and the capital they are required to hold.

Exhibit 1:

How Banks Are Making Money in Collateralized Trading

It is well known that capital ratios have changed how banks make money in repo. As an example, if the Leverage Ratio says that a bank must hold additional Tier 1 capital to balance out non-netted repo positions, then that Tier 1 capital eats up cash that could go towards supporting another liability elsewhere in the firm. In the Liquidity Coverage Ratio (LCR,) a short term repo means that a bank needs to cover that position with enough cash to pass the LCR’s stress test. This consumes cash or other high quality assets.

In response to these constraints, banks have conformed their businesses by reducing net balance sheet utilization while widening out spreads materially, especially around quarter end. They have “juniorized” trading desks to reduce costs, and cut unprofitable clients while treating collateral and liquidity management as a utility. At least some of them now excel at netting up to 90% of their gross balance sheet, down from 50% in years past. The impact on overall activity or gross balance sheet has been much less severe, however, as volumes outstanding are down roughly 10%-20% industry wide. These actions have resulted in repo desks slowly returning to profitability.

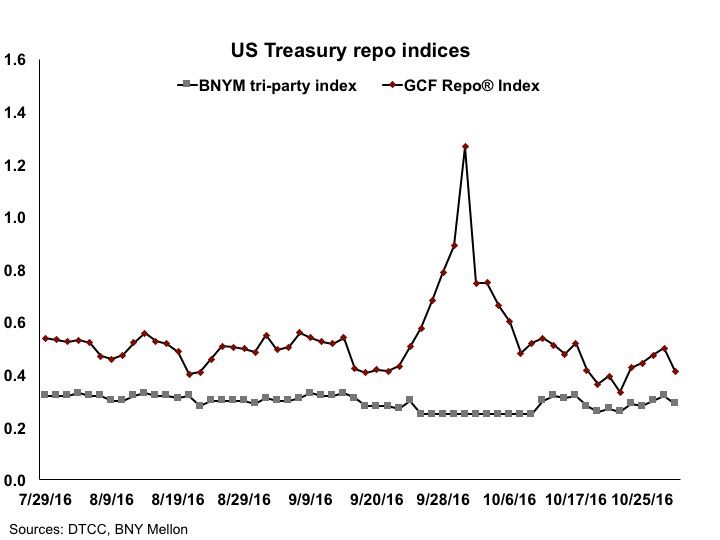

These days, banks make most of their money in collateralized trading in just eight weeks of the year: these are the two weeks around every quarter end when repo balances tighten severely and bank funding is under the most duress. Data for US Treasuries around September 30, 2016 from the DTCC’s GCF Repo Index® and the BNY Mellon Repo Index show the revenue opportunity (see Exhibit 2).

During quarter ends, the fractured nature of pricing for various clients, for what amounts to be the same basket of securities, is extreme. The data show that even outside of quarter end, there is no standardization in repo pricing.

Exhibit 2:

In the search for balance sheet efficiency, banks have segmented their client base carefully. Banks look for clients that can net transactions in order to reduce bank risk exposure; repos which cannot be netted, such as those done with money funds, are considered a dead liability. Banks then take their resulting exposure from the netted trade and look to offset their remaining risk on repo central counterparties (CCPs) on a delivery versus payment basis (DvP). This results in bank CCP balances increasing along with the volume of transactions they net with clients. The one exception to this story is French banks, which reverse collateral in from CCPs and then repo out that collateral to money funds, earning the spread; the difference is that these banks measure balance sheet on a quarterly basis while US banks measure daily. But generally speaking, if a client cannot net their transactions or is not a platinum account or a CCP member, they will pay significantly higher prices to access a bank’s marginal net balance sheet.

US banks and their clients have faced other recent adjustments to their client pricing models. Tri-party reform has changed the times banks would need to fill tri-party shells as well as when cash would need to be returned. That has the potential for a bank to run a negative cash balance at their custodian, which would create daylight overdraft charges and reduce the incentive of banks to trade with money funds. IOSCO/Basel rules on non-cleared derivatives margining, as well as collateral demand on CCPs, require bank clients to mobilize their collateral to raise cash. With cash now a resource to be held close, securities lenders can no longer count on bank balance sheet to create liquidity for their clients. And in a sharp reversal of historical patterns, bank fixed income and equity desks are working together to borrow bonds from securities lenders against equity collateral. Add to that the end of interoperability in the GCF® repo space between BNY Mellon and J.P. Morgan, and you can have quite a volatile elixir of pricing and repo access.

Most clients on the receiving end of repo rates typically have no frame of reference for knowing if they got the best rate or not, or really any indication of fairness at all. For the biggest platinum clients, there is in fact some transparency as banks compete fiercely with one another to do their business; the biggest funds may have already done the work to figure out their own cash investing and collateral requirements, what the “market pricing” is, and how to get it. However, large swaths of clients are not getting market rates, not getting transparency and are seeing wider spreads than they used to. These clients have ceded the responsibility of mobilizing collateral to a bank, and they will take the bank pricing that they are given with no argument.

The Elixium Solution

We at Elixium have worked in the markets and carefully considered why banks’ business models are now impaired, how clients are priced, and what type of arrangements can improve pricing and hence profitability for end investors. We concluded that the market needed an all-to-all platform where anyone could sign up and get a fee based on a single prevailing rate. This repositions the conversation away from banks spreads and the bank model of credit intermediation. It’s a necessary move for the successful growth of collateralized trading products.

Our market has three important qualities:

- The collateral provider and the liquidity provider transact at a market price, not a bank price. This solves the problem of best execution for the benefit of regulators (MiFID II) and investors, who want to know that their Treasury, asset manager or cash collateral reinvestment fund is doing the best possible job. Of course, we have to educate clients about why they don’t need to pay for bank spreads and can get comfortable with extending credit to other buy-side accounts, but that is part of the process.

- We endeavor to industrialize the onboarding process with a universal Global Master Repurchase Agreement (GMRA). There is no need to be a clearing member or contribute to a guarantee fund with Elixium; an investor just needs a credit line, risk parameters and a signed legal agreement. Investors have the option of sticking with the banks they have always done business with or expanding their credit agreements to include counterparties like insurance companies or corporations. This is a specific choice for each investor, and we leave it up to them, but the legal framework is now in place for the decision to be made.

- We provide options in post-trade processing. We have worked out the plumbing across multiple scenarios—bilateral, triparty and CCP—that allow investors to settle and manage trades the way they want. The Elixium platform does not dictate which mechanism must be used, but instead offers a menu selection. Most recently, we partnered with Pirum to help firms automate their post-trade activity.

Just as bank net balance sheets are being reduced, the growing need for clients to access them and mobilize their High Quality Liquid Assets (HQLA) is on the rise. And should volatility pick up, the demand for cash to meet margin calls could easily outstrip the supply of HQLA to the market. At Elixium, this is the space we are looking to occupy to provide a financing solution.

The Elixium model is not going to replace the role of banks in financial markets, but it does provide an important alternative for investors looking for collateralized trades at a recognized market price. Banks have increased their costs to clients to meet return hurdles ⎼ a rational decision, but not one that means clients need to pay for this change in their business model.

Stephen Malekian is Head of Business Development – US for Elixium.

He has over 35 years of experience in the global financing markets, having run Global Fixed Income Finance and Prime Services at Citi and European and Asian Fixed Income Finance at Barclays. Steve has been Chairman of SIFMA’s Executive Committee of their Funding Division, member of the New York Federal Reserve Task Force on Triparty Reform, as well as a member of the European Repo Council and the LCH Risk Committee.