Excerpts from speech by Agustín Carstens, general manager of the Bank for International Settlements, at the FT Banking Summit, London, 4 December 2018

In contrast to banks, big tech firms do not have a traditional branch network through which to interact with customers. Instead, big tech lenders build a picture of their customers using proprietary data from their online platforms and from other sources, such as social media and customers’ digital footprints.

Notably, decisions on whether or not to lend are based on predictive algorithms and machine learning techniques. This gives big tech lenders a method of client scoring that in itself could give them an advantage over traditional banks, which commonly rely more on human judgment to approve or reject credit applications. Moreover, this could also be applied to small and medium-sized enterprises (SMEs) that cannot provide audited financial statements.

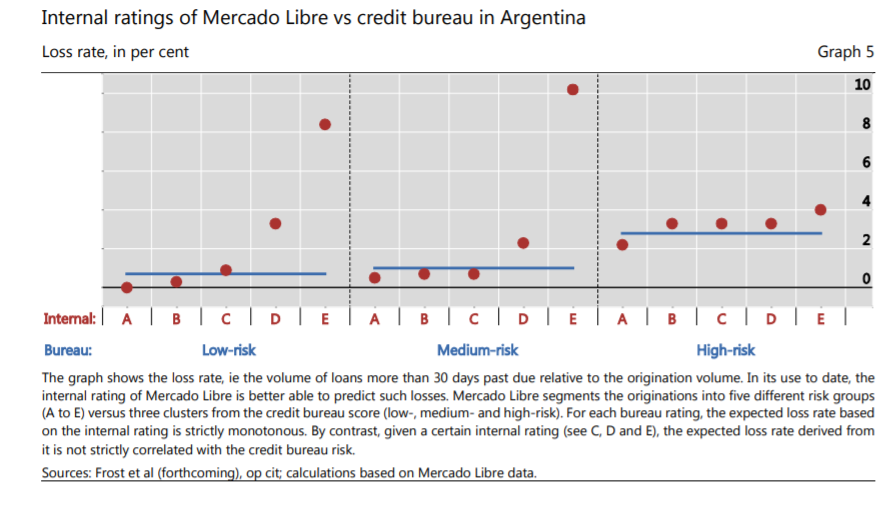

Preliminary evidence suggests that leveraging transactional data with artificial intelligence and machine learning could help predict repayment prospects. For instance, Graph 5 shows that the credible model of Mercado Libre in Argentina has, in the short run at least, outperformed the local credit bureau in predicting losses of corporate borrowers.

Fintech credit in China, India and Latin America is typically provided to SMEs that do not meet the minimum requirements for completing a bank loan application. Big tech firms are able to overcome these limitations by exploiting the information provided by their core business, such as e-commerce or social media, thus reducing the need for additional documentation from merchants. Moreover, the use of machine learning enables a direct and fast assessment of credit risk that could improve the underwriting process by increasing its speed and also preventing, in some cases, human bias from entering the decision, according to research from the University of Geneva.

China’s big tech policies

In China, the move of big tech into finance has had accompanying regulations. The central bank, PBC, has, among other reforms, introduced reserve and central clearing requirements. Since June 2018, big tech firms have had to channel payments through an authorised clearing house. The establishment of a two-tier clearing system improves transparency in the Chinese payment system. This allows the PBC to monitor customer funds on third-party payment platforms.

And from January 2019, the PBC will require big tech firms to keep a 100% reserve requirement on the custodial accounts. The effects of this change are similar to being in a narrow banking system, as it reduces big tech firms’ ability to supply platform credit.

Concluding remarks

Regulators have to provide a secure and level playing field for all participants, incumbents and new entrants alike. At the same time, they have to foster innovative and competitive financial markets. Firms providing similar services or taking similar risks cannot operate under different regulatory regimes. This would create regulatory gaps, with new business models shifting critical activities outside current regulation.

At the same time, new challenges are emerging. Some of these lie beyond the traditional remit of financial regulation – for example, the collection and sharing of client data. Still, these trends may have profound implications for the evolution of traditional models of financial intermediation and competition among players.

Authorities around the world have a joint interest in an open and frank discussion of public policy goals and responses. We must work together both to harness the promise of big tech and to manage its risks. Global safety and soundness will benefit from more cooperation between supervisors and more information-sharing, especially as big tech firms operate across national borders. As in most financial regulation, international coordination is the name of the game.