In a recent Quarterly Review paper, the Bank for International Settlements (BIS) published a study on how government debt markets in emerging market economies (EMEs) have grown and matured. Not only has it become easier for foreign investors to participate in these markets, but also the local investor base has deepened.

“Our findings show that the investor base and size of hedging markets affect the liquidity and resilience of EME government debt markets. In times of stress, a greater presence of domestic banks helps stabilize liquidity conditions, while domestic and foreign non-banks could propagate external shocks. Countries with more developed hedging markets exhibit more resilient liquidity conditions after major shocks,” the authors wrote.

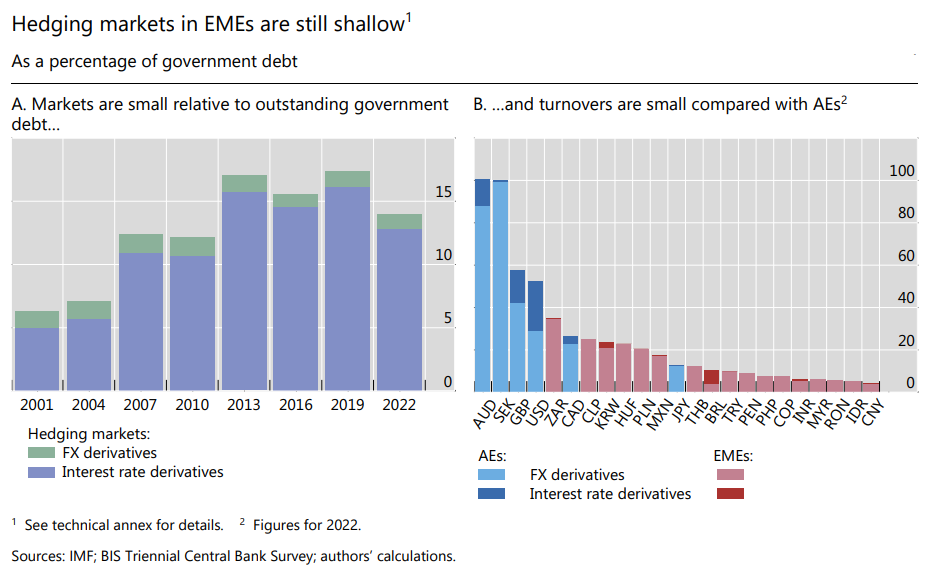

Hedging markets

Along with the presence of different investor types, market liquidity also depends on the presence and size of complementary markets, such as those for repos and derivatives. Repos allow investors to borrow against their securities holdings when faced with cash needs, rather than selling them. They also support liquidity provision more directly by allowing securities dealers to fund their trading inventories, to reuse securities held by long-term investors for trading and to lever up their securities portfolios. Derivatives, in turn, permit investors to adjust their exposure to exchange and interest rate risk instead of transacting in the market for the underlying bonds.

While the development of complementary markets has its merits, it also raises certain concerns that warrant consideration. Since repos tend to be short term, relying on them for funding leads to a shortening of maturities and higher roll-over risk. They can also be used to lever up excessively. This can give rise to procyclicality, increasing financial stability risks, especially if the underlying collateral is illiquid. Similarly, derivatives can transmit external shocks instead of dampening them.

Comprehensive data for repo markets are not readily available. According to the Committee for the Global Financial System (CGFS), in mid-2016, around $12 trillion of repo and reverse repo transactions against government bonds were outstanding globally. Of these, nearly $9 trillion were collateralized with government bonds.

While the share of EMEs in the global total is tiny, some EMEs have quite sizeable repo markets. For instance, in Mexico, the outstanding volume of repos amounted to 21% of outstanding government bonds in mid-2016, which was in line with most advanced economies (AEs). Over the past decade, growth in the markets to hedge currency and interest rate risk has not kept up with the increase in overall government debt in EMEs.

While the share of EMEs in the global total is tiny, some EMEs have quite sizeable repo markets. For instance, in Mexico, the outstanding volume of repos amounted to 21% of outstanding government bonds in mid-2016, which was in line with most advanced economies (AEs). Over the past decade, growth in the markets to hedge currency and interest rate risk has not kept up with the increase in overall government debt in EMEs.

While these markets continued to grow – both in terms of dollar volumes and relative to GDP – derivatives turnover fell when expressed relative to government debt outstanding (due to the strong rise of the latter). Some EMEs do have relatively deep markets, but they lag their AE peers. A common obstacle to developing hedging markets is an imbalance between players who want to hedge themselves against a specific risk and those prepared to take the other side. Since macroeconomic risks, such as exchange rate and interest rate risk, are not easy to diversify, financial intermediaries are often not prepared to sell the appropriate insurance unless they are able to offload their positions to investors who are exposed to such risks in opposite ways.