The Bank for International Settlements released its quarterly review for the period 9 September through 24 November 2023.

- Bond markets remained volatile, with yields oscillating on evolving investor perceptions of the future path of policy interest rates; announcements of sovereign debt issuance also played a role.

- Risky asset markets lost ground before recovering, following the path set by bond yields, while conditions in credit markets remained benign.

- Emerging market economies (EME) financial markets grappled with swings in US yields and changing pressures on domestic currencies. Portfolio outflows continued, reflecting a divergence in expected interest rate paths.

Markets oscillated as monetary policy interest rate hikes appeared to be coming to an end. Long-term yields surged and then retreated on investors’ evolving perceptions of future policy actions. After reaching highs in some cases not seen since the run-up to the Great Financial Crisis (GFC), yields declined rapidly in November.

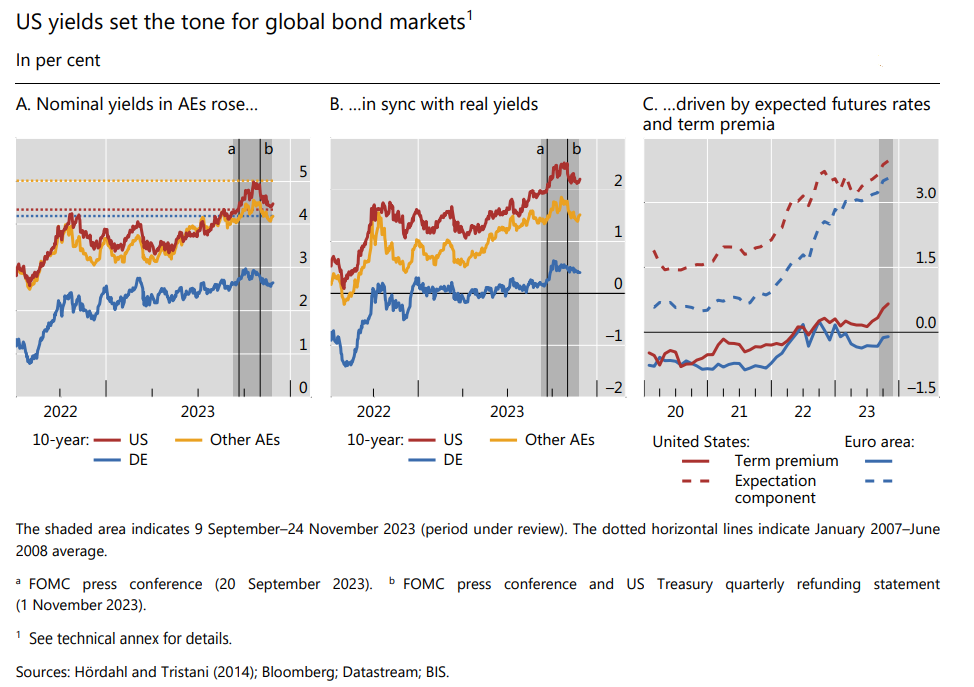

Developments in risky asset markets, as well as exchange rates and capital flows in EMEs, were closely intertwined with the evolution of core bond markets. The path of long-term yields reflected market participants’ strong reactions to statements by public authorities and news about the economic outlook. With inflation slowing, nominal and real yields followed similar paths in major advanced economies (AEs). Long-term yields started the review period under upward pressure from rising term premia, amid expectations of an increased supply of long-term debt, as announced earlier by the US Treasury. The rise in yields accelerated following the September Federal Open Market Committee (FOMC) meeting, as investors began to expect policy rates to stay high for longer than previously anticipated.

Fixed income markets reversed course in November, when investors interpreted central bank communication and macroeconomic data releases as suggesting an earlier end to the hiking cycle. In addition, pressures on term premia eased on announcements of lower than expected issuance of long-dated Treasuries.

Long-term yields in Japan reached highs not seen in a decade, with the central bank further relaxing its yield curve control (YCC) policy and the yen briefly depreciating to its lowest level since 1990. Bond spreads temporarily widened within the euro area on country-specific fiscal concerns. Developments in risky asset markets were closely linked with those in fixed income markets. Stock prices declined for most of the review period and then rallied in November, in tandem with those of government bonds. The correlation between equity and government bond returns has remained positive since inflation took hold in 2021, thus weakening investor demand for bonds as a hedge and contributing to higher yields.

Credit market conditions continued to be relatively benign, although credit spreads did widen temporarily. Fairly compressed credit spreads reflected relatively subdued corporate debt issuance, solid balance sheets for many corporates and possible lags in the transmission from higher policy rates to debt service burdens. Banks kept lending standards tight amid a pickup in default rates, while loan demand remained weak, especially in the euro area. Emerging market economy (EME) financial markets continued to grapple with high US yields and the prospect of accelerating capital outflows, before getting some respite in November. Long-term local currency government bond yields increased, albeit less than in the United States, with term premia edging up, particularly in Latin America. EME portfolio flows were mostly negative, both in Asian and Latin American funds. While some EME currencies went through a short bout of depreciation against the US dollar, most ended up flat on net over the review period.

Among the special features, the BIS highlighted: Liquid assets at CCPs and systemic liquidity risks; and Who borrows from money market funds?.