With the end of the hiking phase in sight, investors focused on macroeconomic developments during the Bank for International Settlements’ (BIS) review period (1 June through 8 September 2023), while staying attuned to their policy implications. Government bond yields rose in advanced economies (AEs), with term structures reflecting increasingly diverse economic outlooks. Despite a spell of de-risking in August, risk-taking was generally resilient, including in emerging market economies (EMEs).

In early August, US Treasuries were at the center of heightened market volatility in early August. Yield rises accelerated as investors became more convinced that higher rates were here to stay following better than expected US growth numbers. In addition, several, almost concurrent announcements fueled investor unease and led to a sell-off: an unexpected increase in the issuance of long-dated bonds by the US government; the greater flexibility in the Bank of Japan’s yield curve control policy; and a downgrade of the US sovereign credit rating. The upward pressure on US yields spilled over to other AE government bond markets.

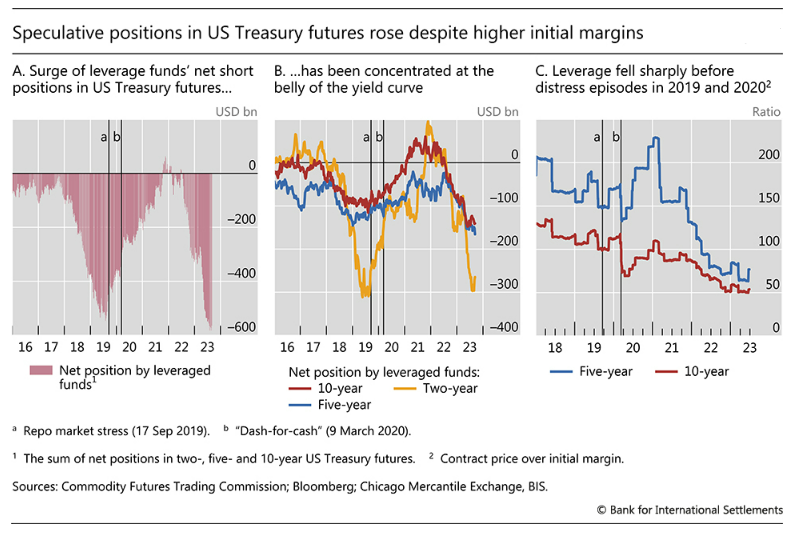

The BIS noted that “the current build-up of leveraged short positions in US Treasury futures is a financial vulnerability worth monitoring because of the margin spirals it could potentially trigger”.

Risky assets extended their gains from the previous quarter, despite a brief pause in August alongside the heightened volatility in fixed income markets. With the end of the hiking cycle perceived to be in sight and the prospects of US recession fading, primary market activity in corporate credit markets regained some dynamism, particularly in the US high-yield segment. However, bank lending remained subdued across jurisdictions, the BIS’ overview noted.

In a separate feature article, BIS researchers examined international banks’ deposit funding – traditional deposits, repos and interbank lending. Netting out interbank lending and abstracting from the effect of central bank quantitative tightening, they find that during the banking turmoil in the first quarter of 2023 the source of banks’ deposit funding rotated from the non-financial sector to non-bank financial institutions.

This rotation was material in a handful of jurisdictions. In particular, residents of Switzerland moved deposits from international banks located there to domestically oriented banks. Dollar funding of banks in the United States shifted to money market funds, which then increased their (repo) dollar funding of non-US banks.