In its quarterly review between December 24 2024 and February 28 2025, the Bank for International Settlements (BIS) spotlighted “Markets caught in cross-currents”.

The BIS observed that long-term government bond yields in core markets rose despite easing monetary policies, tightening financial conditions. In contrast, corporate credit remained buoyant, equity valuations stayed elevated and US dollar appreciation halted. This resulted in easier conditions despite the uncertain outlook, which seemed not fully priced in financial markets.

The rise of long-term rates led to a material steepening of yield curves. Term spreads turned solidly positive in most advanced economies, particularly in non-US markets. The yield curve steepening was exacerbated by a notable increase in term premia, indicating that investors demanded greater compensation for holding long-term interest rate exposure. Moreover, market-based gauges of neutral interest rates also rose steadily throughout the review period, and especially sharply for the euro area.

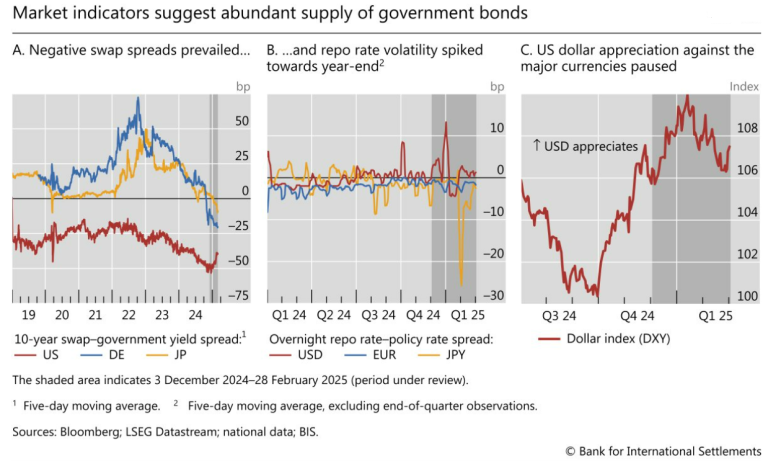

The increase in term premia coincided with market signals of abundant government bond supply. For instance, interest rate swap spreads – the difference between the fixed rate leg of an interest rate swap and government bond yields of the same tenor – turned negative for Japanese yen swaps during the review period, joining comparable US and German instruments. Swap spreads have been negative in the United States for a prolonged time, but touched multi-year lows during the review period.

Short-term funding markets in the United States also reflected the influence of more abundant bond collateral, in combination with typical year-end constraints on dealer intermediation. The spread between the US overnight repo rate and the effective federal funds rate experienced a significant spike towards the end of 2024. This spike appeared to reflect the heightened need for repo financing to accommodate large Treasury issuances and constraints on dealers’ balance sheet space due to end-of-year regulatory reporting requirements. No such jumps were observed in Europe or Japan, where bond collateral at this juncture seems relatively less abundant.