- FX swaps, forwards and currency swaps give rise to dollar obligations that were backstopped in 2008 and 2020 by central banks acting on little information about who owed the debt.

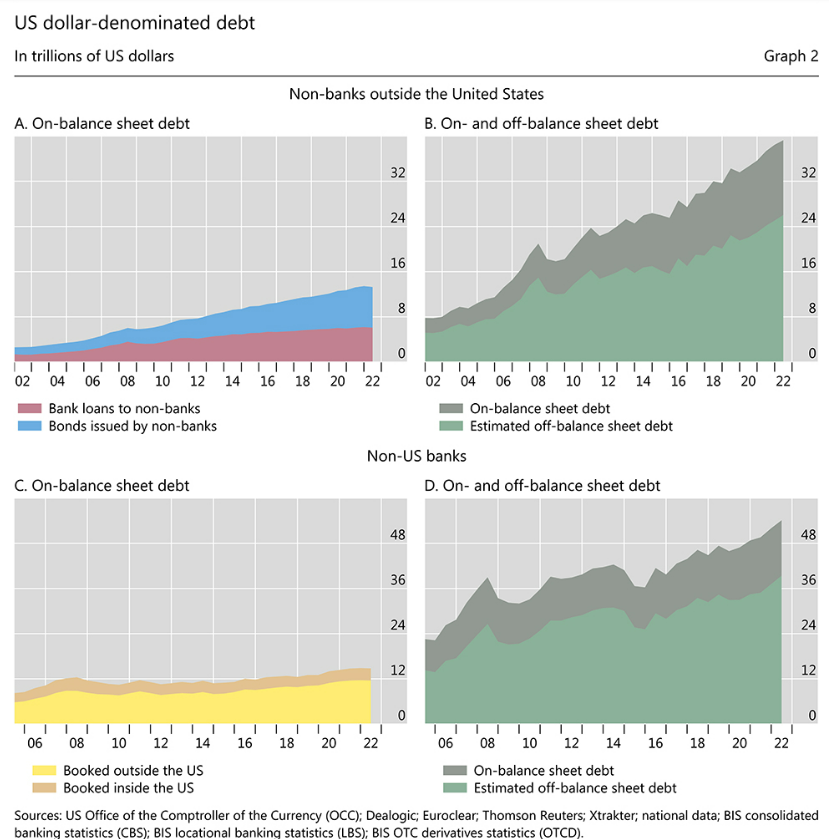

- For non-banks outside the United States, dollar obligations from FX swaps, forwards and currency swaps have grown fast, reaching $26 trillion or double their on-balance sheet dollar debt.

- In mid-2022, non-US banks with direct access to Federal Reserve credit only in their US operations owed an estimated $39 trillion in dollars from FX swaps, forwards and currency swaps.

Embedded in the foreign exchange (FX) market is huge, unseen dollar borrowing. In an FX swap, for instance, a Dutch pension fund or Japanese insurer borrows dollars and lends euro or yen in the “spot leg”, and later repays the dollars and receives euro or yen in the “forward leg”. Thus, an FX swap, along with its close cousin, a currency swap, resembles a repurchase agreement, or repo, with a currency rather than a security as “collateral”.

Unlike repo, the payment obligations from these instruments are recorded off-balance sheet, in a blind spot. The $80 trillion-plus in outstanding obligations to pay US dollars in FX swaps/forwards and currency swaps, mostly very short-term, exceeds the stocks of dollar Treasury bills, repo and commercial paper combined. The churn of deals approached $5 trillion per day in April 2022, two thirds of daily global FX turnover.

FX swap markets are vulnerable to funding squeezes. This was evident during the Great Financial Crisis (GFC) and again in March 2020 when the Covid-19 pandemic wrought havoc. For all the differences between 2008 and 2020, swaps emerged in both episodes as flash points, with dollar borrowers forced to pay high rates if they could borrow at all. To restore market functioning, central bank swap lines funneled dollars to non-US banks offshore, which on-lent to those scrambling for dollars.

The missing dollar debt from FX swaps/forwards and currency swaps is huge, adding to the vulnerabilities created by on-balance sheet dollar debts of non-US borrowers. It has reached $26 trillion for non-banks outside the United States, double their on-balance sheet debt. Moreover, it has grown smartly since 2016, despite the often significant premium demanded on dollar swap funding. For banks headquartered outside the United States, dollar debt from these instruments is estimated at $39 trillion, more than double their on-balance sheet dollar debt and more than 10 times their capital.

This off-balance sheet dollar debt poses particular policy challenges because standard debt statistics miss it. The lack of direct information makes it harder for policymakers to anticipate the scale and geography of dollar rollover needs. Thus, in times of crisis, policies to restore the smooth flow of short-term dollars in the financial system (eg central bank swap lines) are set in a fog.